111 NE 1st ST

Miami, Florida 33132

USA

Embedded finance, or embedded banking, involves integrating financial services into non-financial platforms like retail, e-commerce, or social media apps.

This growing trend is set to transform the financial industry, with significant growth expected in the coming years.

Here are some key statistics and forecasts for the embedded finance industry in 2024.

Data Sources And Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and trends in Embedded Finance. Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include

While we strive for accuracy, trends in [topic] can shift rapidly. These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaway

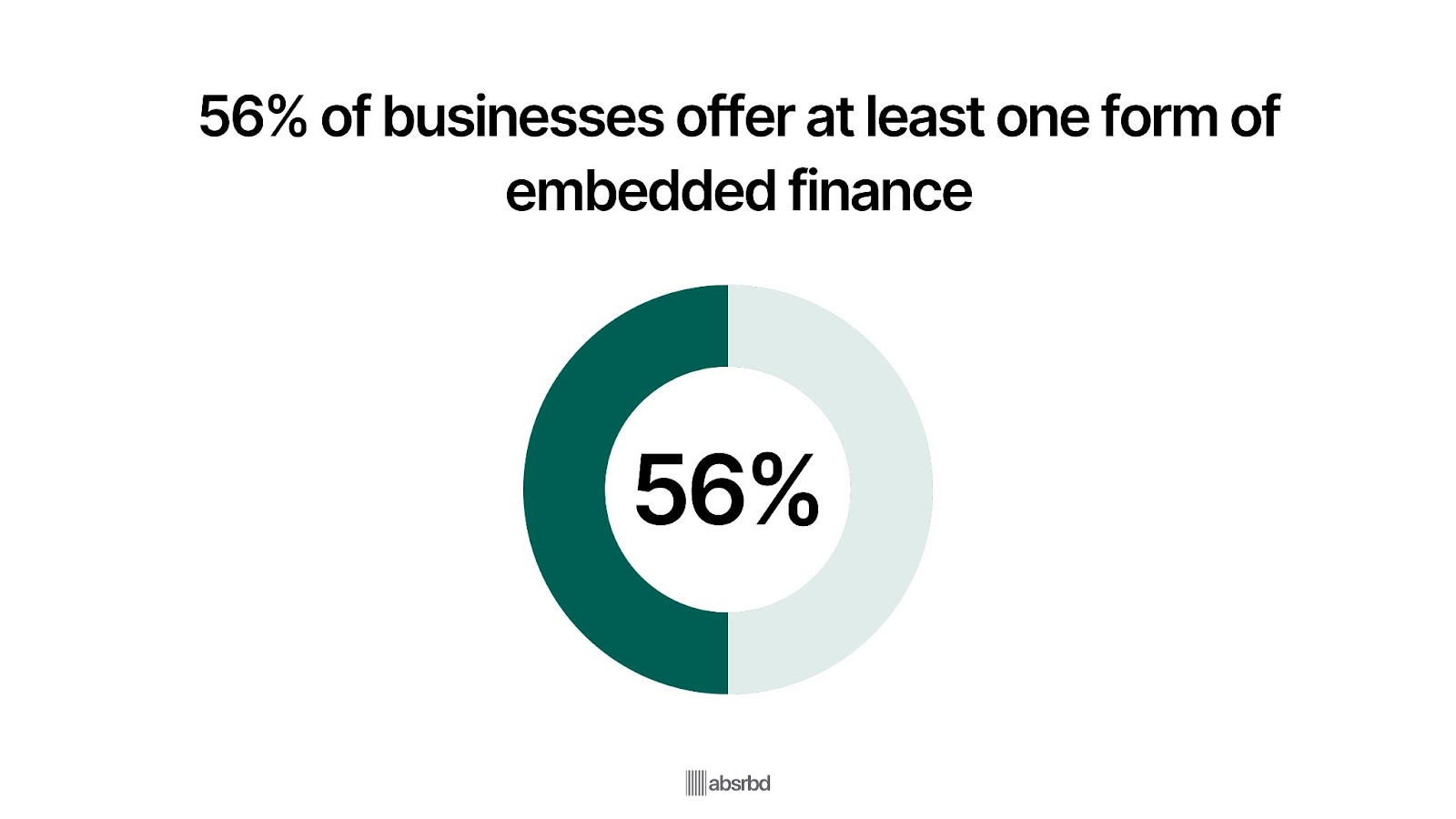

- 56% of businesses offer at least one form of embedded finance, and 55% of non-financial businesses plan to introduce these services within the next two years.

- The embedded finance market is projected to grow significantly, with its transaction volume in the U.S. expected to exceed $7 trillion by 2026, up from $2.6 trillion in 2021.

- AI-powered systems detect fraud by up to 50%.

- 45% of Gen Z and Millennials utilized BNPL services in the past year.

Overview of Embedded Finance

Embedded finance has its roots in the rise of fintech in the early 2010s when companies began integrating financial services directly into non-financial platforms.

Initially, it was about merging software and commerce models. Still, it has since expanded to include various financial services directly within non-financial applications, such as payments, lending, and insurance.

Embedded finance refers to the seamless integration of financial services into non-financial platforms, allowing users to access financial services as part of their regular digital interactions.

This includes services like payments, lending, and insurance embedded within platforms such as e-commerce sites and apps.

The embedded finance market is experiencing rapid growth, with its transaction volume in the U.S. alone reaching $2.6 trillion in 2021 and projected to exceed $7 trillion by 2026 (Bain & Company).

Major players in this sector include fintech startups like Walnut and Unit, which offer embedded insurance and financial services.

The widespread adoption of digital wallets and mobile payments also contributes to the expansion of embedded finance.

Embedded finance is crucial as it enhances user experience by providing seamless financial interactions, improves financial inclusion, and creates new revenue streams for businesses.

Its integration into everyday platforms reshapes the financial landscape, offering convenience and efficiency to consumers and businesses alike.

Key Statistics

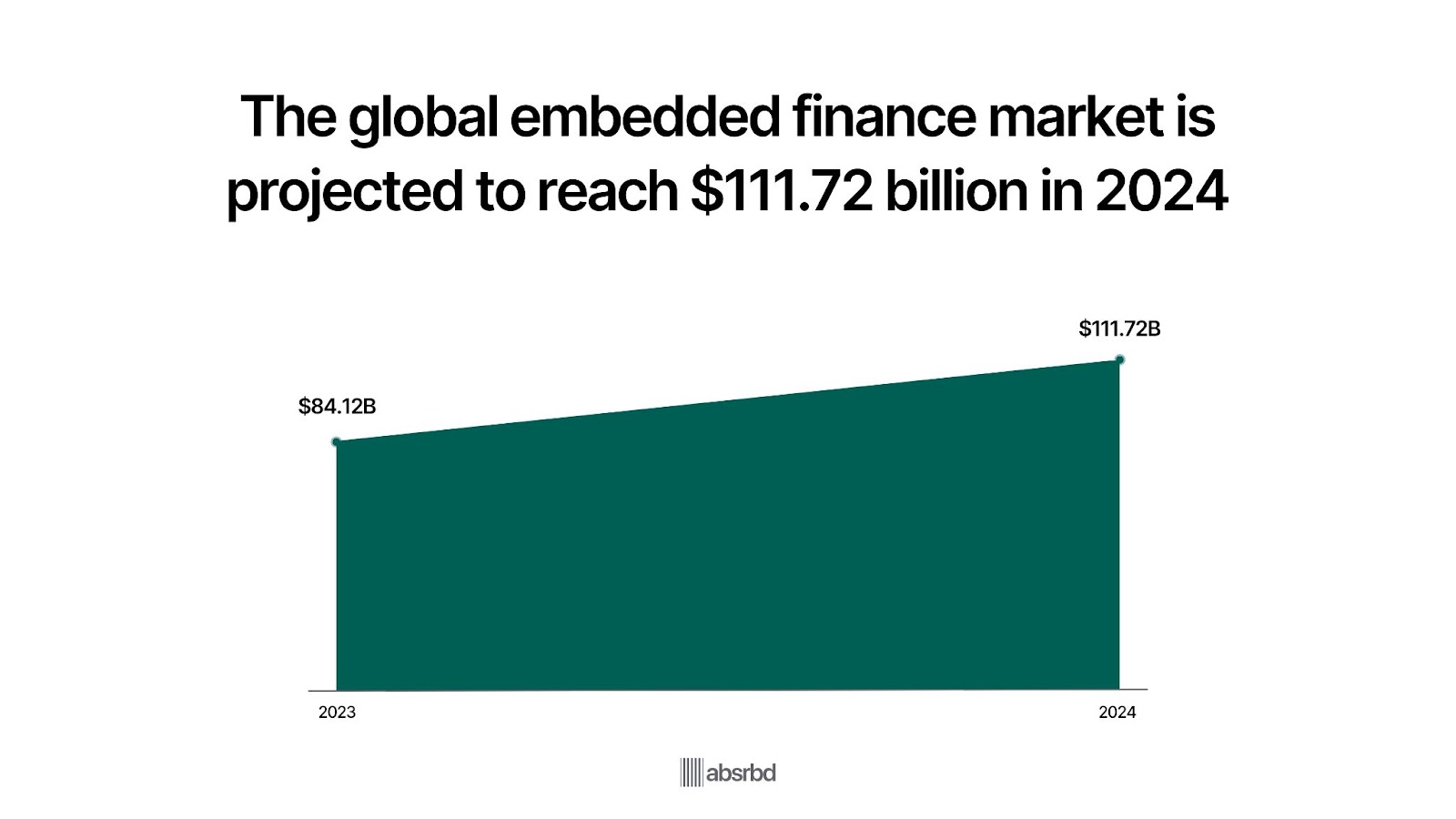

The global embedded finance market was estimated at $84.12 billion in 2023 and was projected to reach approximately $111.72 billion in 2024. (Precedence research)

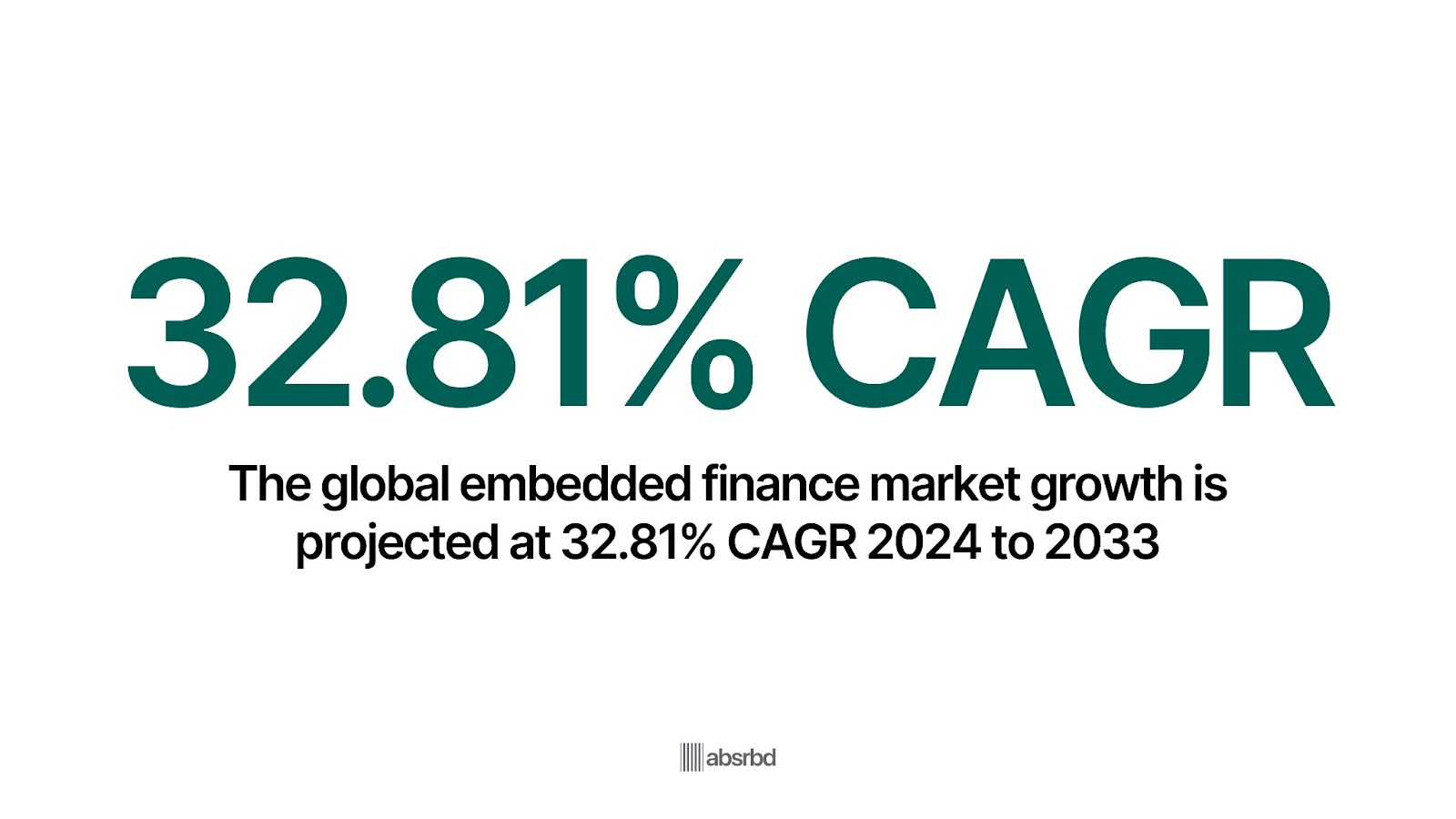

It is expected to grow at a compound annual growth rate (CAGR) of 32.81% from 2024 to 2033. (Precedence research)

It is expected to reach around $1.43 trillion by 2033. (Precedence research)

56% of businesses already offer at least one form of embedded finance, and only 14% do not plan to invest in it in the next year. (Capterra)

55% of non-financial businesses plan to offer embedded finance services within the next two years. (Statista)

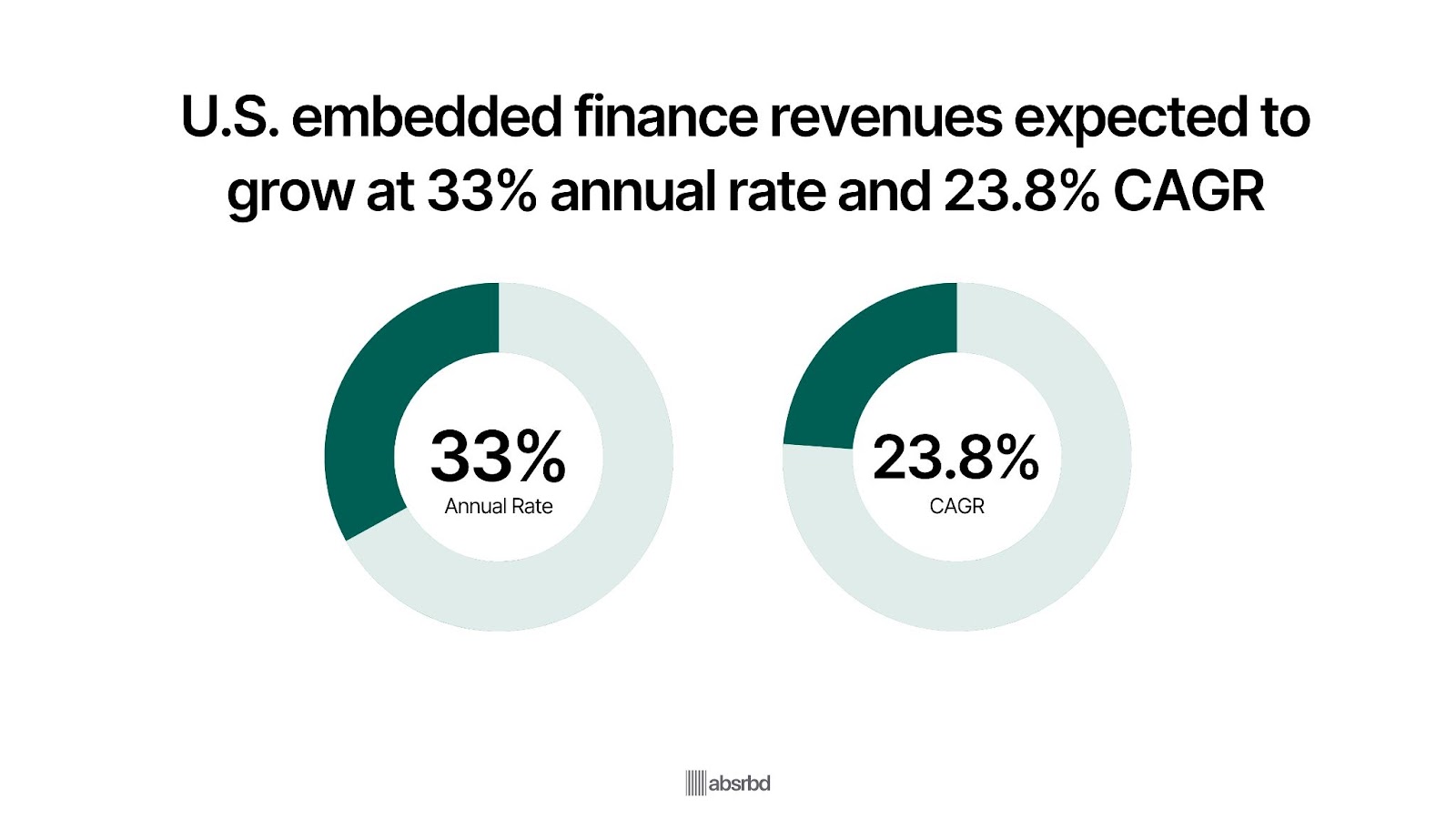

In the United States, embedded finance revenues are expected to grow from $36.99 billion in 2024 to $107.51 billion by 2029. (Yahoo Finance)

It is expected to grow at an annual growth rate of 33% and a compound annual growth rate (CAGR) of 23.8% during this period. (Yahoo Finance)

86% of U.S. mobile wallet users have purchased the retailer's embedded mobile app. (Marqeta)

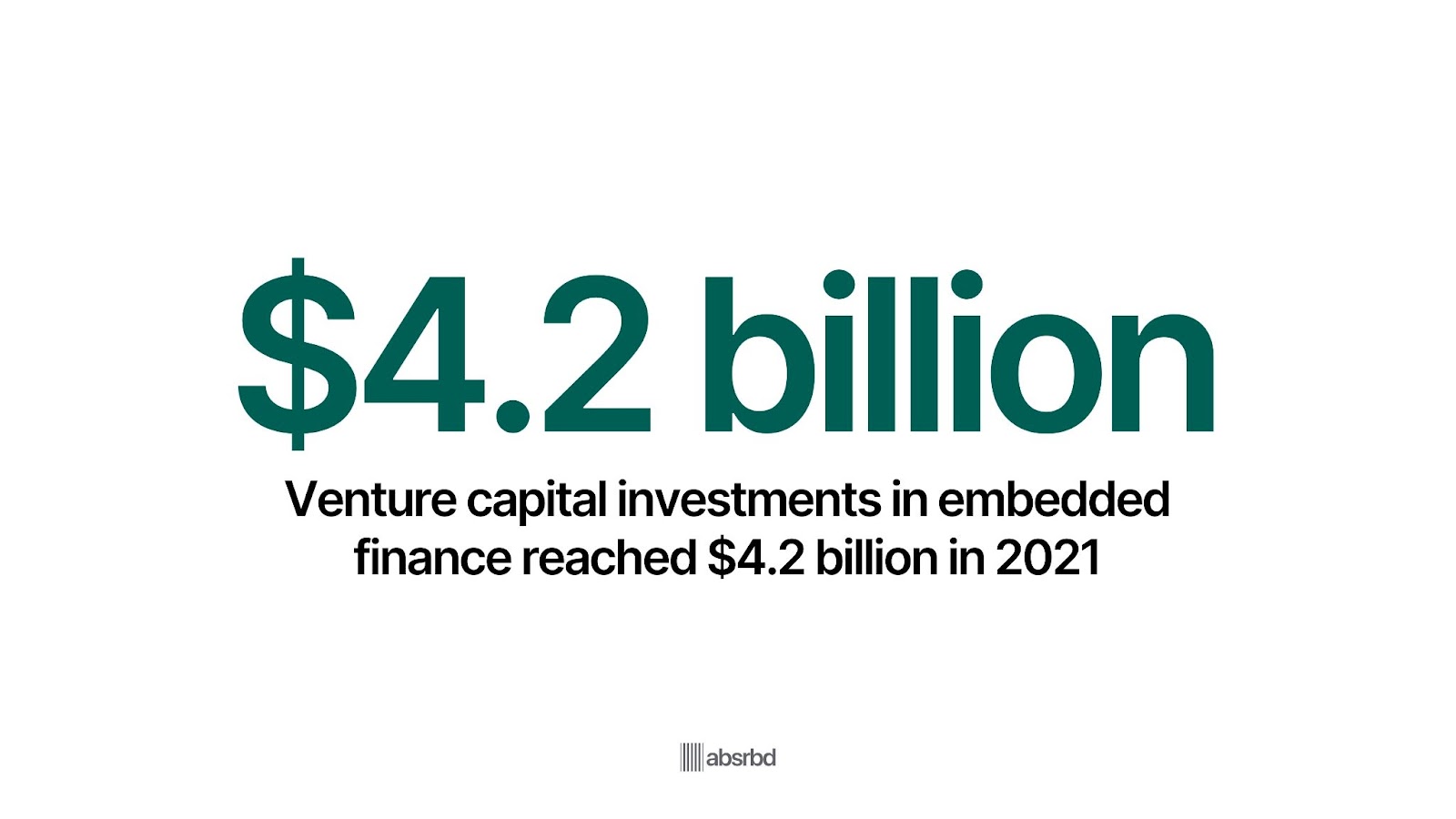

Venture capital investments in embedded finance reached $4.2 billion in 2021. (Statista)

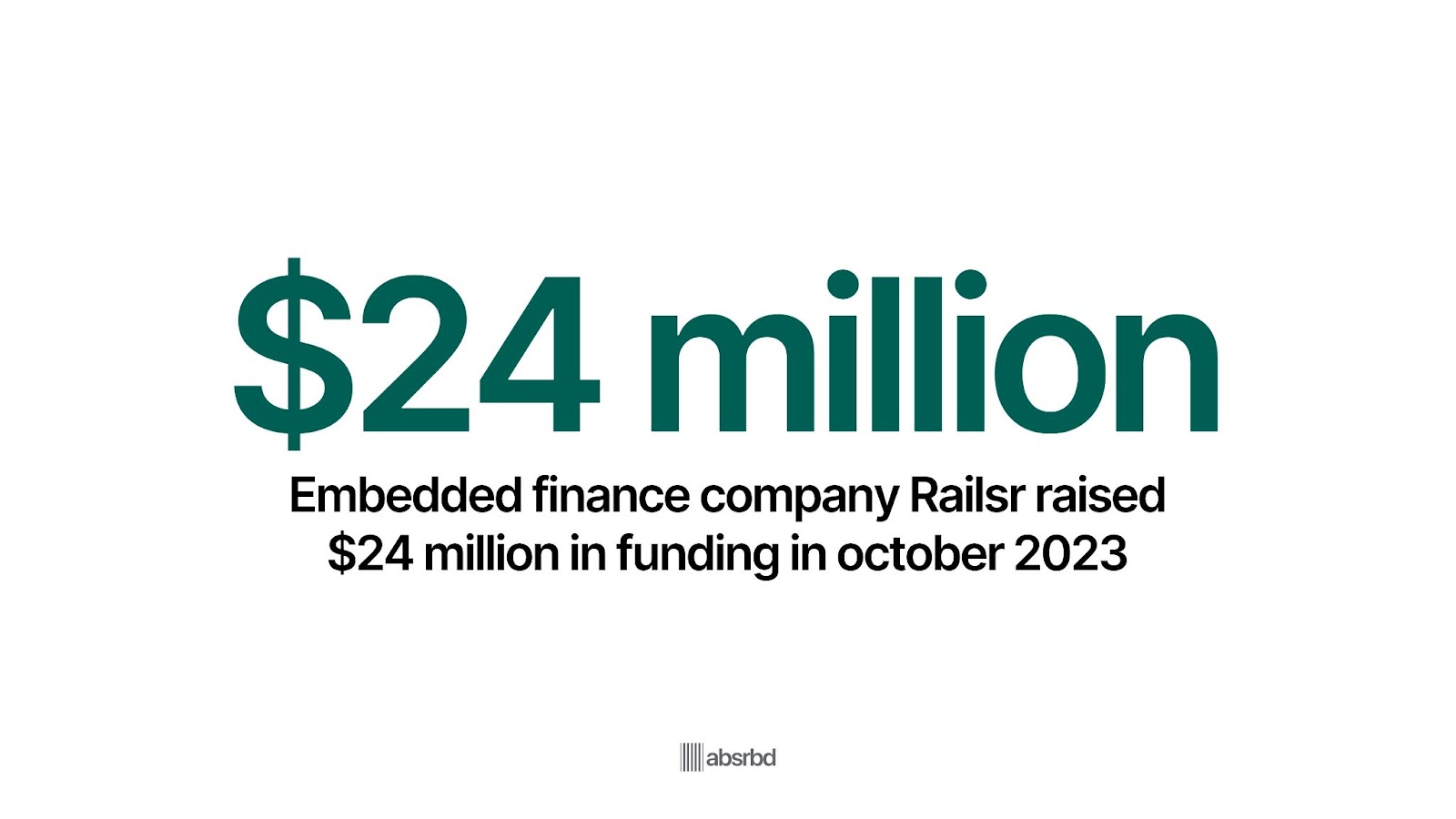

In October 2023, Railsr, a global embedded finance company, raised $24 million in funding from investors. (Grand View Research)

Major Trends in Embedded Finance

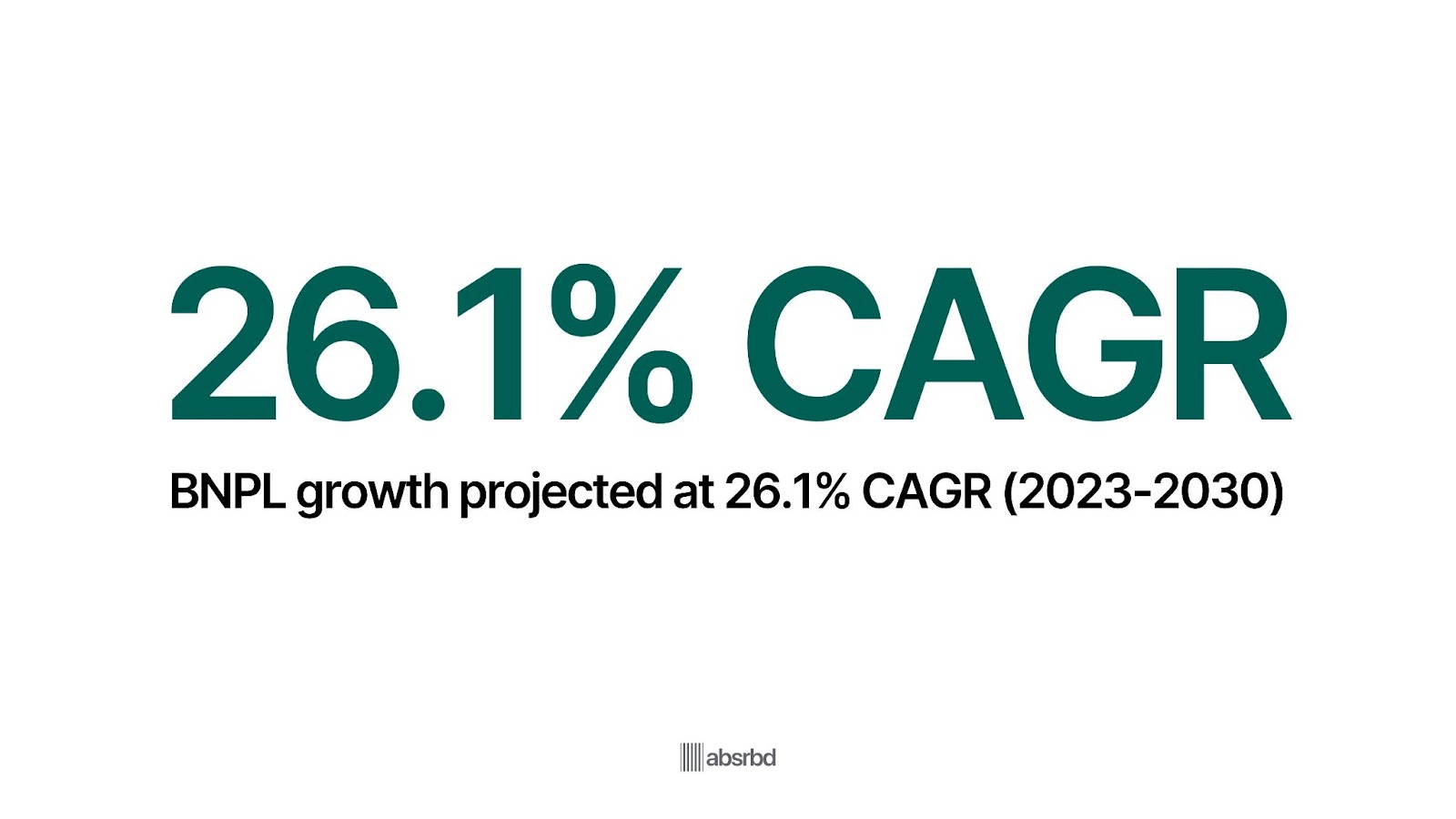

BNPL (Buy Now, Pay Later) is Expected to Grow at a CAGR of 26.1% from 2023 to 2030 (Grand View Research)

The Buy Now, Pay Later (BNPL) model is rapidly gaining popularity. The market is expected to grow at a compound annual growth rate of 26.1% between 2023 and 2030.

This trend is reshaping consumer credit, offering an alternative to traditional credit cards with more flexible payment options.

BNPL services appeal particularly to younger consumers, with 45% of Gen Z and Millennials using BNPL services in the past year (Pymnts).

This shift indicates a growing demand for more transparent and manageable payment methods.

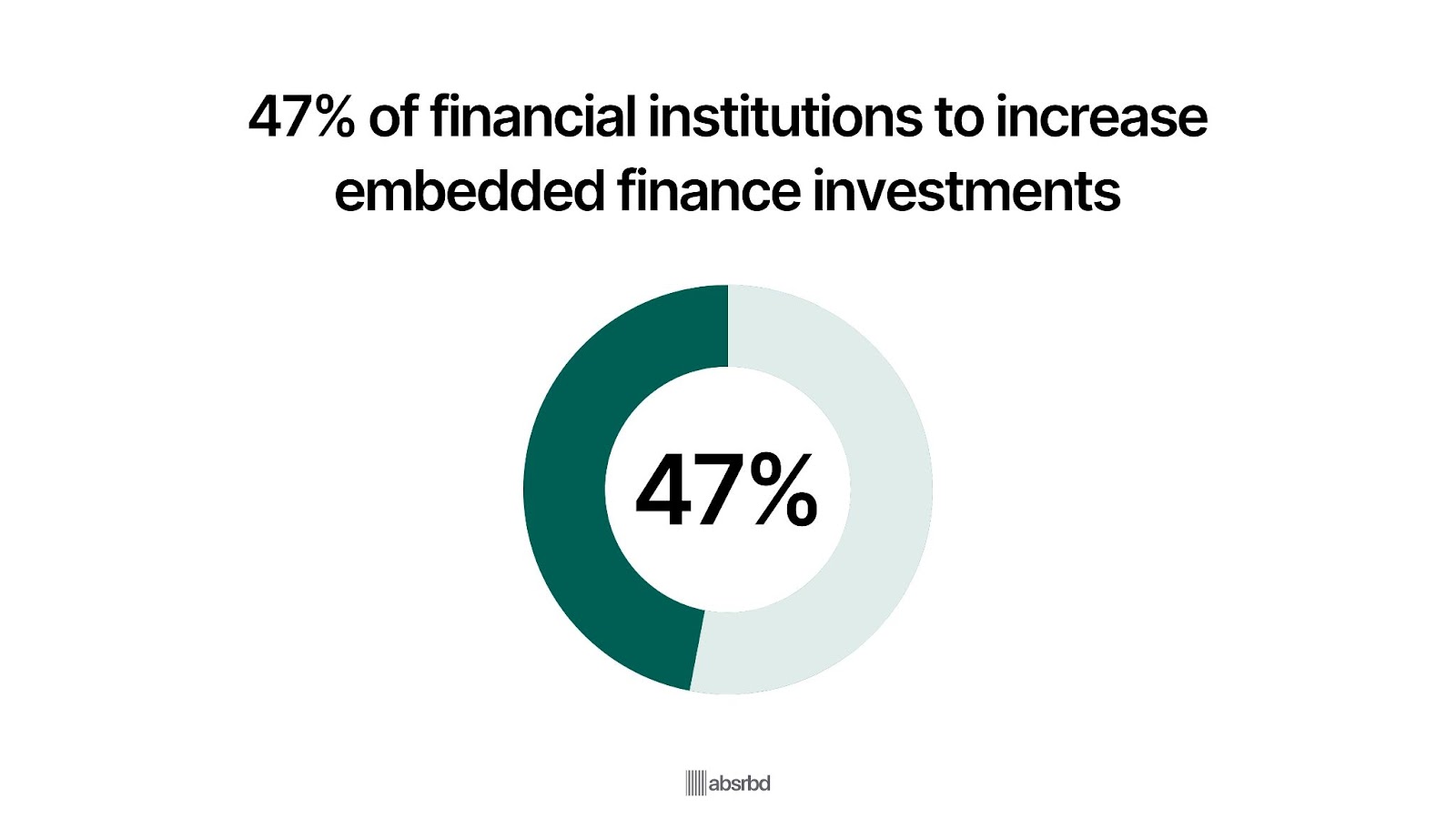

47% of Financial Institutions Plan to Increase Embedded Finance Investments (Accenture)

Most financial institutions are planning to increase their investments in embedded finance solutions.

This trend underscores the growing recognition of embedded finance's potential to create new revenue streams and enhance customer engagement by integrating financial services into non-financial platforms.

The strategic shift is driven by the desire to capture more of the customer journey and provide seamless financial services.

For example, in the retail sector, companies like Shopify and Amazon increasingly embed financial products into their platforms, simplifying access to credit and payments for their users.

Embedded Insurance Distribution Could Exceed $70 Billion in Premium in the U.S. by 2030 (Conning)

Embedded insurance is growing, with the market expected to reach $70 billion by 2025.

This trend is crucial as it offers consumers insurance coverage seamlessly integrated into their purchasing journey, such as travel insurance when booking a flight.

This not only simplifies the purchase process but also increases the penetration of insurance products.

Companies like Tesla have started embedding insurance products directly into their car sales, highlighting the potential of this trend.

AI-Powered Fraud Detection Reduces False Positives by 50% (McKinsey)

Artificial Intelligence is revolutionizing fraud detection in financial services, with AI-powered systems reducing false positives by up to 50%.

This trend is significant as it improves the accuracy and efficiency of detecting fraudulent transactions, saving financial institutions billions in losses annually.

For example, JPMorgan Chase has implemented AI algorithms that analyze transaction patterns to flag suspicious activities more precisely, reducing the burden on human analysts and enhancing overall security.

Cybersecurity Investments in Financial Services Reached $188.1 Billion in 2023 (Gartner)

The financial services sector is significantly ramping up its cybersecurity efforts, with investments projected to reach $215 billion by the end of 2024, an increase of 14.3% from 2023.

This trend is driven by the increasing sophistication of cyber threats targeting financial institutions, necessitating advanced security measures.

This is crucial because financial services are a primary target for cyberattacks, and robust cybersecurity is essential to maintaining trust and protecting sensitive data.

Banks like Bank of America invest heavily in AI-driven cybersecurity solutions to detect and respond to threats in real-time.

96% of Financial Services Pioneers Believe in Blockchain's Scalability (Deloitte)

According to Deloitte’s fourth annual Global Blockchain Survey, around 96% of financial services pioneers believe blockchain is a broadly scalable solution that has already achieved mainstream adoption.

This trend is significant because blockchain offers a decentralized and transparent way to conduct transactions, reducing the need for intermediaries and lowering transaction costs.

Major financial institutions like HSBC and Santander are exploring blockchain for cross-border payments, aiming to streamline processes and enhance security. This demonstrates the technology's transformative potential.

Decentralized Finance (DeFi) Market to Surpass $446.43 Billion by 2031 (Yahoo Finance)

Decentralized Finance (DeFi) is experiencing exponential growth, with the market projected to surpass $446.43 billion by 2031.

This trend is significant because DeFi platforms offer financial services such as lending, borrowing, and trading without traditional intermediaries like banks.

The rise of DeFi is democratizing access to financial services, particularly in regions with underdeveloped banking infrastructure.

Platforms like Aave and Uniswap lead this movement, allowing users to participate in financial markets through blockchain technology.

Embedded Finance Challenges

The adoption of blockchain in financial services faces several key challenges that need to be addressed for the technology to reach its full potential. Here are some of the main challenges

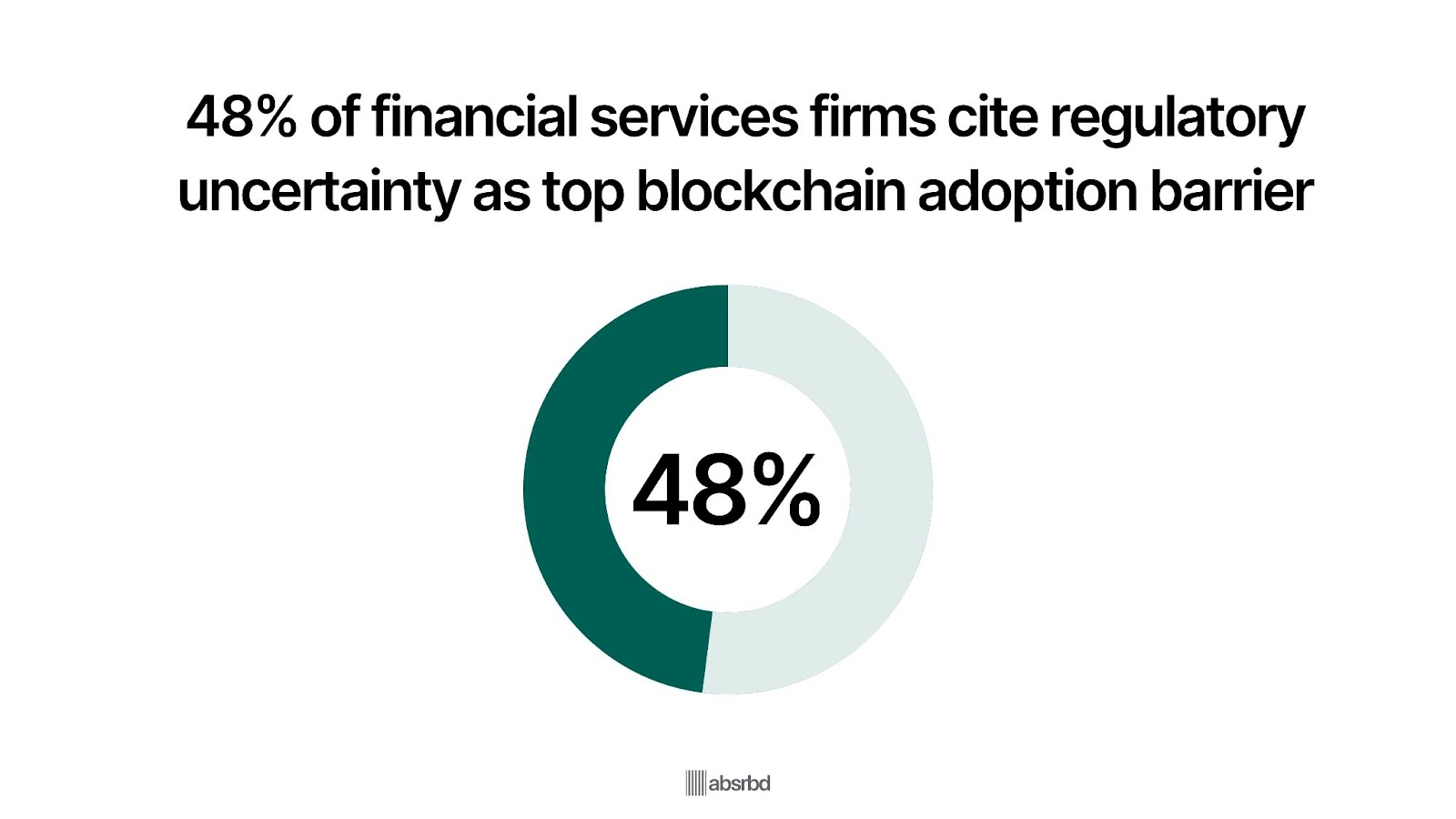

Regulatory Uncertainty

The lack of clear regulations around blockchain and cryptocurrencies is a major barrier to adoption.

A survey by PwC found that 48% of financial services firms cited regulatory uncertainty as the biggest obstacle to adopting blockchain. (PWC)

In China, the lack of regulation limits blockchain applications in financial services, as stability and trust are crucial in the industry.

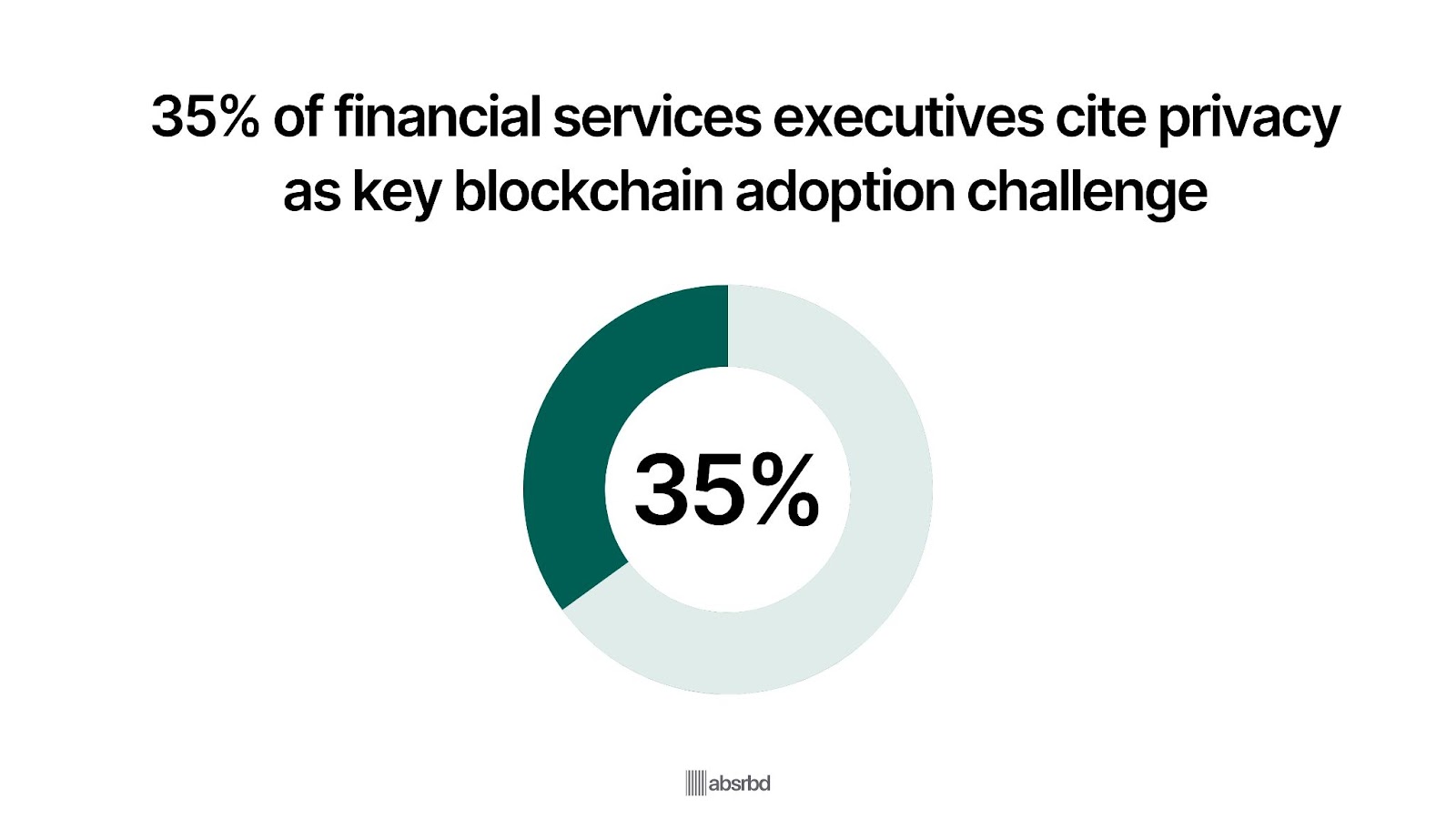

Privacy and Security Concerns

Financial institutions are hesitant to adopt blockchain due to concerns about privacy and security.

A study by the World Economic Forum found that 35% of financial services executives cited privacy as a key challenge in blockchain adoption. (PWC)

Example: Blockchain adoption in financial services can proliferate once the issue of privacy preservation is resolved.

Scalability and Performance

Current blockchain networks struggle with scalability and performance compared to traditional financial systems.

Visa can process over 24,000 transactions per second (Science Direct), while Bitcoin can only handle around 7 transactions per second. (Bitcoin)

Scalability is one of the key barriers to blockchain's widespread adoption in financial services.

Interoperability and Standards

The lack of interoperability between different blockchain platforms and the absence of industry standards hinders adoption.

Example: Ensuring standardization via smart financial contracts will enable legacy institutions to begin implementing blockchain-based innovations.

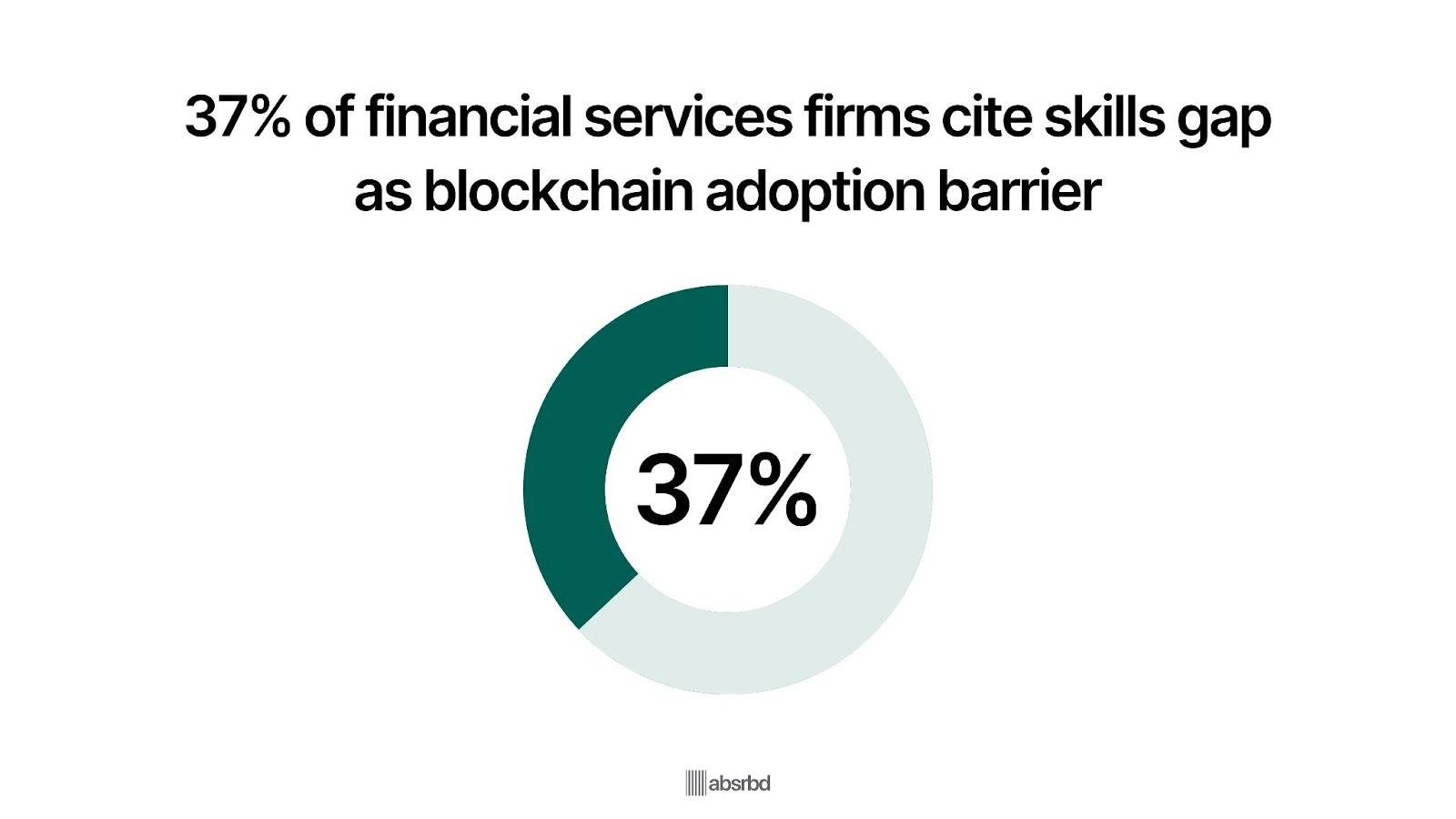

Talent and Expertise Shortage

There is a shortage of blockchain developers and experts in the financial services industry.

A survey by PwC found that 37% of financial services firms cited a lack of in-house skills as a barrier to blockchain adoption. (PWC)

Example: In the institutional landscape, regulatory uncertainty and questions regarding unproven tools and infrastructure have created barriers to blockchain adoption.

Embedded Finance opportunities

Emerging opportunities in embedded finance are expanding as technology and consumer expectations evolve.

Here are some key areas where embedded finance is likely to create new possibilities:

Embedded Financial Wellness Tools

Companies can embed financial wellness tools into their platforms to help users manage their finances more effectively.

These tools could include budgeting, savings automation, credit monitoring, and personalized financial advice.

Employers could integrate financial wellness platforms into employee benefits programs, providing tools like automated savings plans and real-time financial advice to enhance employee financial health.

Embedded Crypto Services

With the growing interest in cryptocurrencies, businesses can offer embedded crypto trading, savings, and payment services.

This would allow users to buy, sell, or pay with cryptocurrencies directly within non-financial platforms.

E-commerce sites could integrate crypto wallets, enabling users to pay seamlessly with Bitcoin or other cryptocurrencies, expanding payment options and catering to a broader audience.

SaaS Platforms Offering Embedded Financing

Software-as-a-service (SaaS) platforms can directly offer embedded financing options, such as lending or leasing, within their software.

This can help businesses finance the necessary tools to grow without leaving the platform.

Project management software can integrate financing options for additional features or upgrades, enabling businesses to scale their tools as they grow.

Payment plans can be seamlessly embedded within the SaaS platform, synchronizing the expansion of capabilities with the company's financial flexibility.

Embedded ESG (Environmental, Social, and Governance) Financing

Companies can offer embedded ESG financing options, such as green loans or sustainable investment products, within their platforms.

This caters to the increasing demand for socially responsible finance.

A real estate platform can seamlessly integrate green mortgage options for properties meeting specific sustainability criteria.

This approach creates a smooth flow from property discovery to financing, synchronizing the home-buying process with eco-friendly choices.

By embedding these sustainable financing options directly within the platform, consumers can more easily access and understand the benefits of investing in environmentally conscious homes.

Integrated Health and Insurance Services

Health and wellness platforms can integrate embedded insurance services, such as health insurance or life insurance, directly into their offerings, creating a one-stop shop for health-related financial services.

For example, a fitness app could partner with insurers to offer health insurance discounts or specialized policies based on the user’s activity data, encouraging healthy lifestyles while providing financial protection.

Gig Economy Financial Tools

Platforms that support gig economy workers can embed financial tools tailored to their unique needs, such as instant payouts, income smoothing, and access to credit.

For example, a ride-sharing app could offer embedded financial services like instant cash advances or savings accounts, helping gig workers manage irregular income streams more effectively.

Micro-Investments in E-commerce

E-commerce platforms can embed micro-investment opportunities, allowing consumers to invest small amounts of money in stocks or other assets as they shop, rounding up purchases or earning rewards through investments.

A real estate platform could seamlessly offer embedded green mortgage options for properties that meet specific sustainability criteria, simplifying the process for consumers to finance eco-friendly homes.

Digital Identity and Embedded KYC/AML

Digital identity verification and embedded Know Your Customer (KYC) and Anti-Money Laundering (AML) solutions can be integrated into various platforms, streamlining the onboarding process for financial services and improving security.

A social media platform could embed digital identity verification services, allowing users to easily sign up for financial services without needing separate KYC processes.

Embedded Loyalty Programs with Financial Rewards

Retailers can embed loyalty programs that offer financial rewards, such as cashback, interest-bearing accounts, or investment opportunities, directly into their purchasing ecosystems.

A supermarket chain could offer a loyalty program where points earned from shopping are automatically converted into savings or invested in a mutual fund, increasing customer engagement and financial literacy.

Supply Chain Financing and B2B Embedded Finance

B2B platforms can embed supply chain financing solutions, enabling businesses to access capital and manage cash flow more effectively, particularly in industries with complex supply chains.

A B2B marketplace could offer embedded invoice financing, allowing suppliers to get paid early for their goods, reducing financial strain and improving supply chain efficiency.

Automotive Embedded Finance

Automotive manufacturers and dealerships can offer embedded financing, insurance, and even leasing options directly within their sales platforms, simplifying the vehicle purchasing process.

For instance, an electric vehicle (EV) manufacturer could enhance the purchasing experience by offering embedded financing options alongside bundled insurance and maintenance plans, creating a comprehensive all-in-one solution for customers.

Embedded Real Estate Financing

Real estate platforms can offer embedded mortgage, insurance, and investment services, allowing users to handle all aspects of property buying and selling in one place.

A property listing website, for example, could provide a seamless user experience by integrating mortgage pre-approval and insurance services directly into their platform.

This would enable prospective buyers to browse, finance, and insure a property all within the same ecosystem, streamlining the entire process and reducing the need to navigate multiple external services.

Digital-Only Banking Embedded in Non-Banking Platforms

Non-banking platforms can offer digital-only banking services, such as checking and savings accounts, directly within their ecosystems, targeting specific user segments with tailored banking solutions.

A travel platform could offer embedded digital banking services catering to frequent travelers, such as a travel-focused bank account with no foreign transaction fees.

Embedded Finance Predictions for the Next 3-5 Years

1. Massive Expansion of Embedded Finance Across Industries

Embedded finance will become ubiquitous across multiple industries, with non-financial companies increasingly integrating financial services into their platforms.

This expansion will not be limited to retail and e-commerce but will extend to healthcare, real estate, education, and government services.

The demand for embedded financial solutions will grow as consumers and businesses seek more seamless, integrated experiences.

Companies will use embedded finance to increase customer engagement, drive new revenue streams, and differentiate themselves in competitive markets.

Healthcare providers, for instance, could enhance patient convenience by offering financing options directly through their patient portals.

This would allow users to pay for medical procedures in installments without ever needing to leave the platform, streamlining the payment process and improving overall patient experience.

2. Growth in Embedded Finance Infrastructure Providers

The market for embedded finance infrastructure providers (e.g., Banking-as-a-Service platforms) will grow significantly as more companies seek to offer financial services without obtaining banking licenses themselves.

These providers will offer the necessary APIs and compliance solutions to facilitate the integration of financial services.

As more non-financial companies look to integrate financial services, they will turn to specialized providers to handle the complex regulatory and technical aspects of banking.

This will lower the barrier to entry and speed up the adoption of embedded finance.

Companies like Stripe and Square could expand their offerings to include more comprehensive embedded finance solutions, enabling businesses to integrate everything from payments to lending with minimal effort.

3. Embedded Finance to Drive Financial Inclusion

Embedded finance will play a key role in driving financial inclusion, particularly in emerging markets. By integrating financial services into platforms that people already use, such as mobile apps or e-commerce sites, previously unbanked or underbanked populations will gain easier access to financial products.

The proliferation of smartphones and internet access in developing regions, combined with the flexibility of embedded finance, will enable more people to participate in the formal financial system, leading to greater economic empowerment and growth in these regions.

For example, telecom companies in Africa could embed micro-lending services into their mobile money platforms, providing small loans to individuals who would otherwise have no access to credit.

4. Regulatory Evolution and Standardization

As embedded finance grows, regulatory frameworks will evolve to address the unique challenges and risks associated with integrating financial services into non-financial platforms. There will likely be a push towards standardization and clearer guidelines to ensure consumer protection and market stability.

The rapid expansion of embedded finance will necessitate updated regulations to protect consumers and ensure the stability of financial systems.

Regulators will need to balance innovation with oversight, potentially leading to new laws and standards specific to embedded finance. A real estate platform can seamlessly integrate green mortgage options for properties meeting specific sustainability criteria.

This approach creates a smooth flow from property discovery to financing, synchronizing the home buying process with eco-friendly choices. By embedding these sustainable financing options directly within the platform, consumers can more easily access and understand the benefits of investing in environmentally conscious homes.

5. Proliferation of AI-Driven Personalization

AI and machine learning will play an increasingly important role in embedded finance, enabling more personalized financial services. Platforms will use AI to analyze user data and offer tailored financial products, such as customized insurance policies, investment portfolios, and credit offers.

As AI technology advances, it will become easier to use data-driven insights to offer hyper-personalized financial services that meet individual users' specific needs and preferences, enhancing customer satisfaction and loyalty. An e-commerce platform, for example, could use AI to offer personalized BNPL options based on a user’s purchase history and financial behavior, optimizing terms to match their specific circumstances.

6. Greater Integration of ESG Criteria in Embedded Finance

Environmental, Social, and Governance (ESG) considerations will increasingly integrate into embedded finance offerings. Financial products and services embedded within platforms will increasingly focus on sustainability and social impact.

As consumer awareness of ESG issues grows, businesses will respond by integrating ESG-friendly financial products into their offerings. This will meet consumer demand and align with global sustainability goals.

For example, Retail platforms could offer embedded financing options prioritizing green loans for purchasing eco-friendly products or services, incentivizing sustainable consumer behavior.

7. Rise of Embedded Finance Super Apps

The next few years will see the rise of “super apps” that integrate a wide array of embedded financial services within a single platform, offering users a one-stop shop for all their financial needs. Consumers increasingly value convenience and efficiency, and super apps will meet this demand by consolidating multiple services—such as payments, savings, insurance, and investments—into a single, cohesive experience.

A global player like PayPal or Google could evolve into a super app, offering everything from everyday payments and digital wallets to investment management and insurance, all within one platform.

8. Increased Collaboration Between Fintechs and Traditional Banks

Traditional banks and fintech companies will increasingly collaborate to deliver embedded finance solutions. Banks will leverage fintech innovation to reach new customer segments, while fintechs will benefit from the regulatory expertise and customer trust established banks provide.

The synergy between banks' regulatory know-how and fintechs' agility in innovation will create more robust and compliant embedded finance solutions, accelerating adoption. For example, a traditional bank could partner with a fintech company to offer embedded lending services directly through e-commerce platforms, combining the bank’s financial stability with the fintech’s technological prowess.

Potential Embedded Finance Disruptors

Embedded finance is rapidly growing, and several emerging players are disrupting traditional financial services. Here are some potential disruptors:

- Fintech Startups: Companies like Stripe and Plaid are integrating financial services into various platforms, making it easier for businesses to offer financial products and services directly to their customers.

- Big Tech Companies: Companies such as Apple, Google, and Amazon are leveraging their massive user bases and data to offer financial services, from payment solutions to lending and insurance.

- Neobanks: Digital-only banks like Chime, N26, and Revolut provide banking services without traditional physical branches, often with lower fees and innovative features.

- Blockchain and Cryptocurrencies: Technologies like blockchain and cryptocurrencies enable decentralized finance (DeFi), offering alternatives to traditional banking and financial services.

- Embedded Insurance: Companies like Cover Genius and Slice are embedding insurance products into non-insurance platforms, making it easier for users to access coverage tailored to their needs.

- Buy Now, Pay Later (BNPL) Providers: Firms like Klarna, Afterpay, and Affirm are reshaping how consumers finance their purchases, offering flexible payment options integrated into e-commerce platforms.

- Regtech Solutions: Companies offering regulatory technology, like ComplyAdvantage and Ayasdi, provide compliance and risk management tools that integrate seamlessly with financial services.

Impact of Embedded Finance Market Behaviour on Stakeholders

Embedded finance trends impact various groups in different ways:

Consumers

- Convenience: Consumers benefit from seamless financial services integrated into their favorite apps and platforms, such as easy payments at checkout or instant insurance coverage.

- Personalization: Embedded finance often provides tailored financial products and services based on user data and behavior, such as BNPL options or personalized investment advice.

- Cost Savings: Many fintech solutions and neobanks offer lower fees and more competitive rates than traditional financial institutions.

Businesses

- Enhanced Customer Experience: By integrating financial services into their platforms, businesses can offer a more streamlined experience, increasing customer satisfaction and loyalty.

- New Revenue Streams: Companies can create additional revenue streams by partnering with fintechs or offering financial products like payment processing or insurance.

- Operational Efficiency: Embedded finance can simplify financial operations, reduce administrative overhead, and improve cash flow management through integrated payment solutions and automated processes.

Investors

- Growth Opportunities: Investors have the opportunity to capitalize on the growth of fintech and embedded finance sectors, with many startups and emerging companies offering high returns on investment.

- Diversification: The rise of embedded finance allows investors to diversify their portfolios by including financial technology companies and platforms in their investments.

- Risk Management: Investors need to carefully assess the risks associated with new technologies and regulatory changes in the financial sector to make informed investment decisions.

Financial Institutions

- Competition: Traditional banks and financial institutions face increased competition from fintechs and big tech companies entering the financial space, which may pressure them to innovate and lower fees.

- Collaboration Opportunities: Traditional institutions have opportunities to partner with fintech companies to enhance their offerings and reach new customer segments.

- Regulatory Challenges: Financial institutions must navigate evolving regulations as new financial products and services become embedded in various platforms.

Conclusion

The trends in embedded finance have far-reaching implications for various stakeholders. For consumers, the integration of financial services into everyday platforms provides unparalleled convenience and personalization, often resulting in cost savings and a more seamless experience.

Meanwhile, businesses must contend with increased competition as they integrate financial services into their offerings, which not only enhances customer engagement but also opens up new revenue streams.

This shift requires them to stay agile and innovative to maintain a competitive edge. On the other hand, investors face both exciting growth opportunities in the burgeoning fintech sector and the need to navigate new risks associated with evolving technologies and regulatory landscapes.

Overall, embedded finance is transforming how financial services are delivered and consumed, prompting significant adjustments and strategic planning across all involved parties.

Frequently Asked Question

Who are the Key Players in Embedded Finance?

Stripe, Inc.

Stripe is a leading global fintech company that provides payment processing solutions for businesses, enabling them to accept payments online and through mobile applications.

Its comprehensive suite of products includes payment links, invoicing, and financial connections, making it a key player in the embedded finance ecosystem.

Stripe's ability to facilitate seamless transactions positions it as a crucial partner for businesses looking to integrate financial services into their platforms.

PayPal Holdings, Inc.

PayPal is a well-known online financial platform simplifying payments and commerce for consumers and merchants worldwide.

By offering embedded payment solutions, PayPal allows businesses to provide a smooth checkout experience, enhancing customer convenience.

Its widespread recognition and trust among users make PayPal a significant player in the embedded finance market.

Plaid, Inc.

Plaid specializes in connecting applications to users' bank accounts, enabling seamless access to financial data.

Plaid plays a vital role in the embedded finance ecosystem by providing APIs that facilitate integrating financial services into apps. Its technology allows developers to build applications that offer personalized financial experiences, making it a key enabler of embedded finance.

Klarna Bank AB

Klarna is a prominent player in the embedded finance market, particularly known for its buy now, pay later (BNPL) solutions.

By integrating its payment options directly into e-commerce platforms, Klarna enhances the shopping experience for consumers while driving higher conversion rates for merchants. This innovative approach positions Klarna as a leader in the embedded finance space.

FIS

FIS is a major financial technology solution provider that integrates banking, payments, and financial management services into various business platforms. By enabling companies to enhance their customer experiences through embedded finance, FIS supports businesses in delivering customized financial solutions that meet the evolving demands of the digital economy.

Marqeta

Marqeta is a card-issuing platform that provides businesses with the tools to create and manage their payment cards. By offering embedded card solutions, Marqeta enables companies to streamline payment processes and enhance customer loyalty.

Its focus on providing flexible payment solutions makes it a key player in the embedded finance landscape.

Alloy

Alloy offers an omnichannel identity risk solution that helps banks and fintechs manage compliance and fraud prevention in the embedded finance ecosystem. By providing transparency and oversight across partner portfolios, Alloy empowers embedded finance providers to launch new financial products efficiently and safely, making it an essential player in the market.

What is the Prediction for Embedded Finance?

The prediction for embedded finance indicates significant growth and expansion in the coming years.

The global embedded finance market is estimated to reach $112.6 billion in 2024 and is projected to grow to $237.4 billion by 2029, reflecting a compound annual growth rate (CAGR) of 16.1%. (Globe New Wire)

Additionally, another forecast suggests that the market could grow from $83.32 billion in 2023 to approximately $588.49 billion by 2030, with a CAGR of 32.8%. (Grand View Research)

This growth is driven by increasing consumer demand for convenience, digitalizing financial services, and integrating financial products into non-financial platforms.

Furthermore, embedded payments are expected to dominate the market because they streamline transactions and enhance user experiences. In contrast, embedded lending is anticipated to experience the highest growth rate as it provides easier access to credit for consumers and businesses alike.

What Companies Use Embedded Finance?

Many companies across various industries leverage embedded finance to enhance their offerings and provide integrated financial services. Here are some examples:

E-Commerce Platforms

- Amazon: Integrates financial services through Amazon Pay and credit card offerings, allowing seamless payments and financial transactions within its ecosystem.

- Shopify: Offers embedded payment solutions, including Shopify Payments, and integrates with various financial services for merchants.

Travel and Hospitality

- Expedia: Embeds payment solutions and travel insurance into its booking platform, providing a seamless financial experience for travelers.

- Airbnb: Integrates payment processing and financial transactions directly into its platform for bookings, host payouts, and more.

Ride-Sharing and Mobility

- Uber: Embeds payment solutions into its app, allowing riders to pay for rides and drivers to receive payments directly through the platform.

- Lyft: Similar to Uber, Lyft incorporates financial services for transactions, driver payouts, and more within its app.

Retail

- Walmart: Uses embedded financial services for payment processing, and financial management and even offers its financial products like credit cards and money transfers.

- Target: Integrates payment solutions and financial services into its mobile app and checkout process, enhancing the customer shopping experience.

Financial Technology

- Stripe: Provides embedded payment solutions and financial infrastructure for businesses across various sectors, enabling seamless transactions and financial management.

- Plaid: Offers APIs for embedding financial data and account connectivity into apps and services, enabling functionalities like account verification and personal finance management.

Insurance

- Cover Genius: Embeds insurance products into various non-insurance platforms, offering coverage seamlessly integrated into partner apps and websites.

- Slice: Provides on-demand insurance products that can be embedded into various digital platforms, catering to specific needs like travel or rental coverage.

Digital Banks and Neobanks

- Chime: Operates as a digital bank with integrated financial services, offering banking, payments, and financial management through its app.

- Revolut: Its mobile app embeds various financial services, including banking, trading, and insurance.