Money isn’t just something we use, it’s becoming a service we can access anywhere, anytime.

From mobile wallets to embedded finance, Money as a Service MaaS platforms deliver seamless experiences, addressing traditional banking’s gaps.

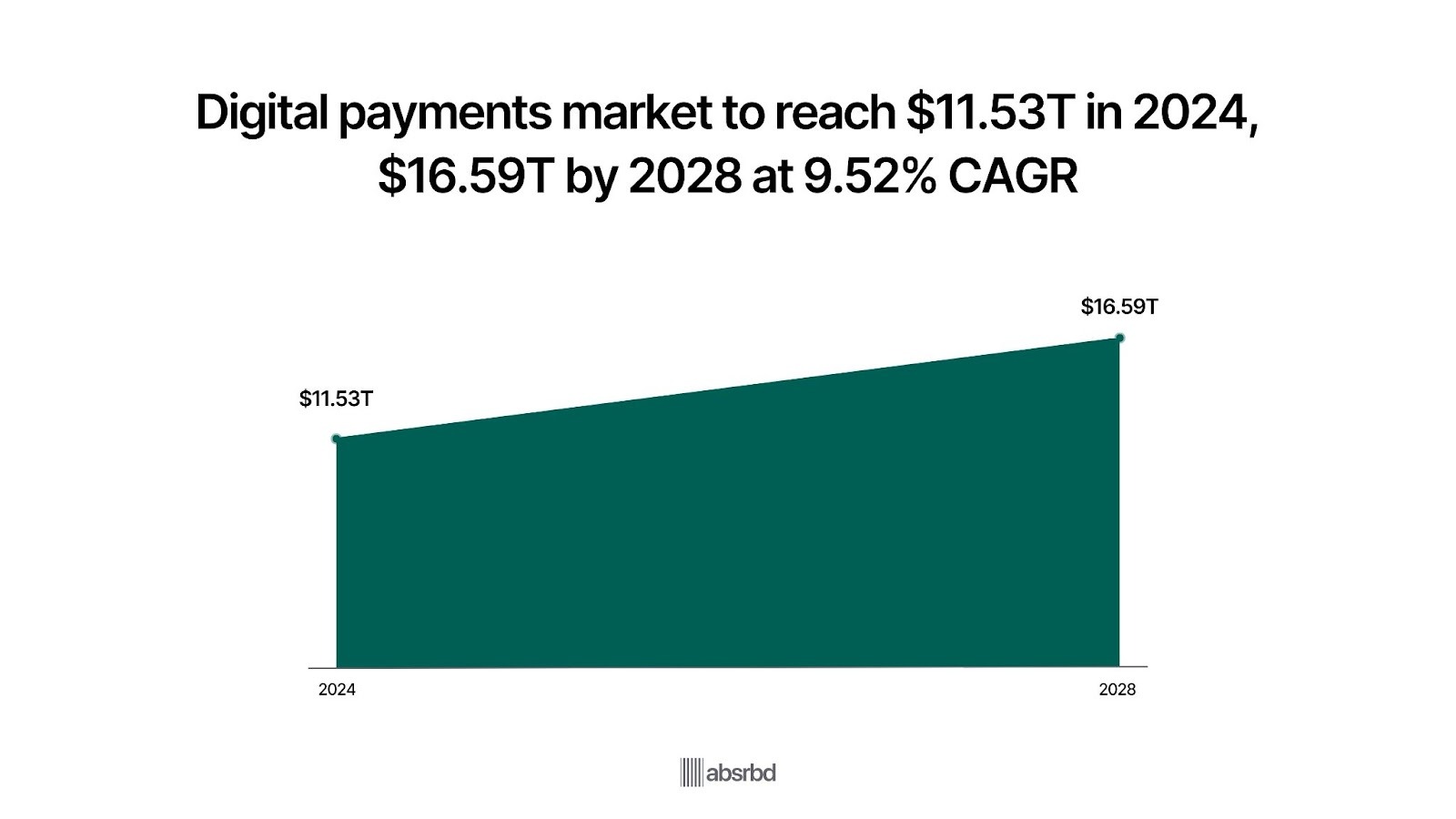

With the global digital payments market projected to hit $16.59 trillion by 2028, MaaS is gaining widespread adoption as it’s meeting growing demand for integrated solutions.

In this article, I’ll show you everything you need to know about the trends, challenges, emerging opportunities and the impact of MaaS on various stakeholders in this space.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and relevant developments in the Money Service Business.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, occurrences in the MaaS market are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaways

- The global payment as a service market was valued at $13.88 billion in 2022.

- 69% of consumers prefer personalized financial experiences.

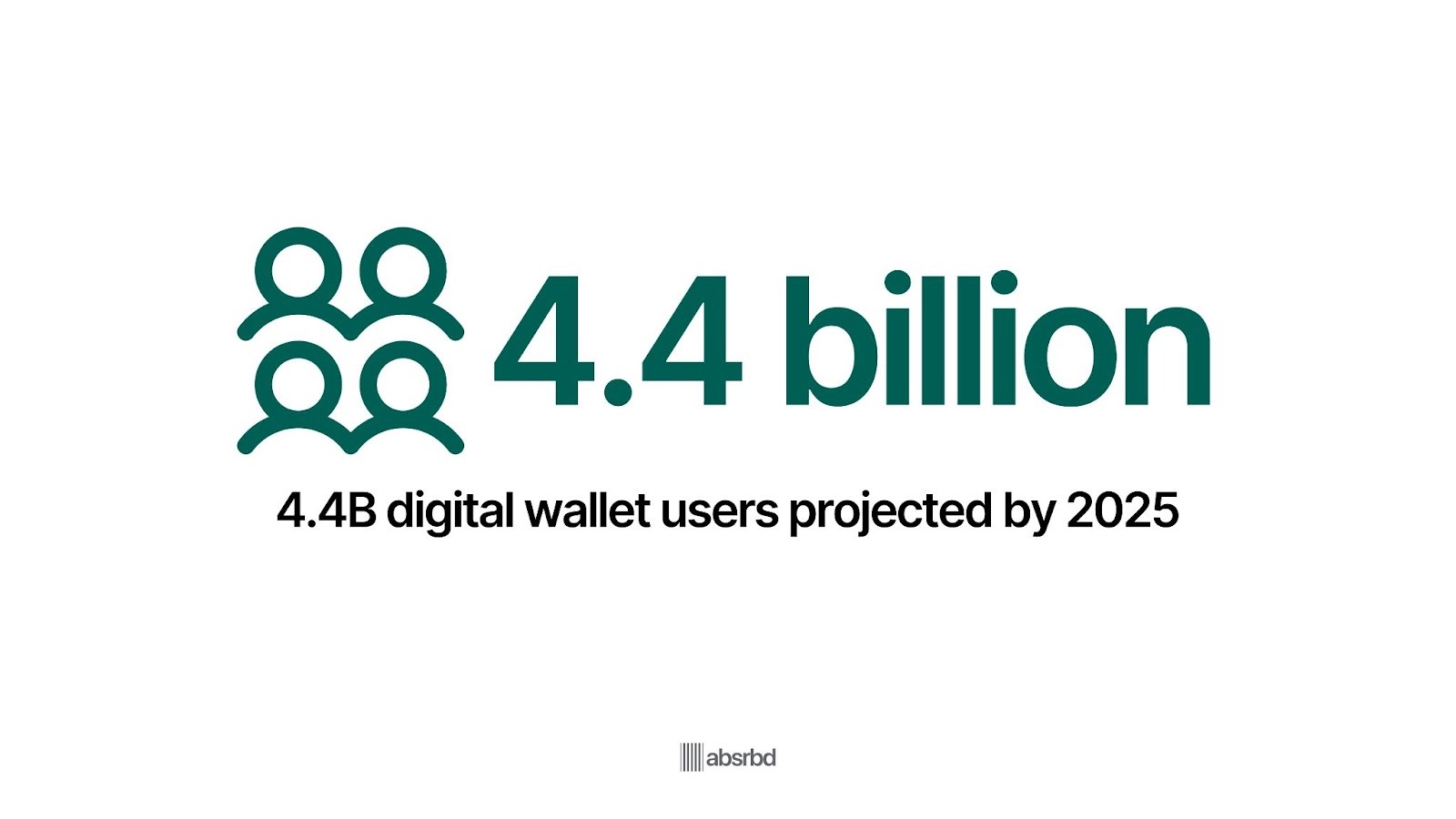

- Digital wallet users are expected to reach 4.4 billion globally by 2025, up from 2.6 billion in 2020, representing nearly 60% of the world's population.

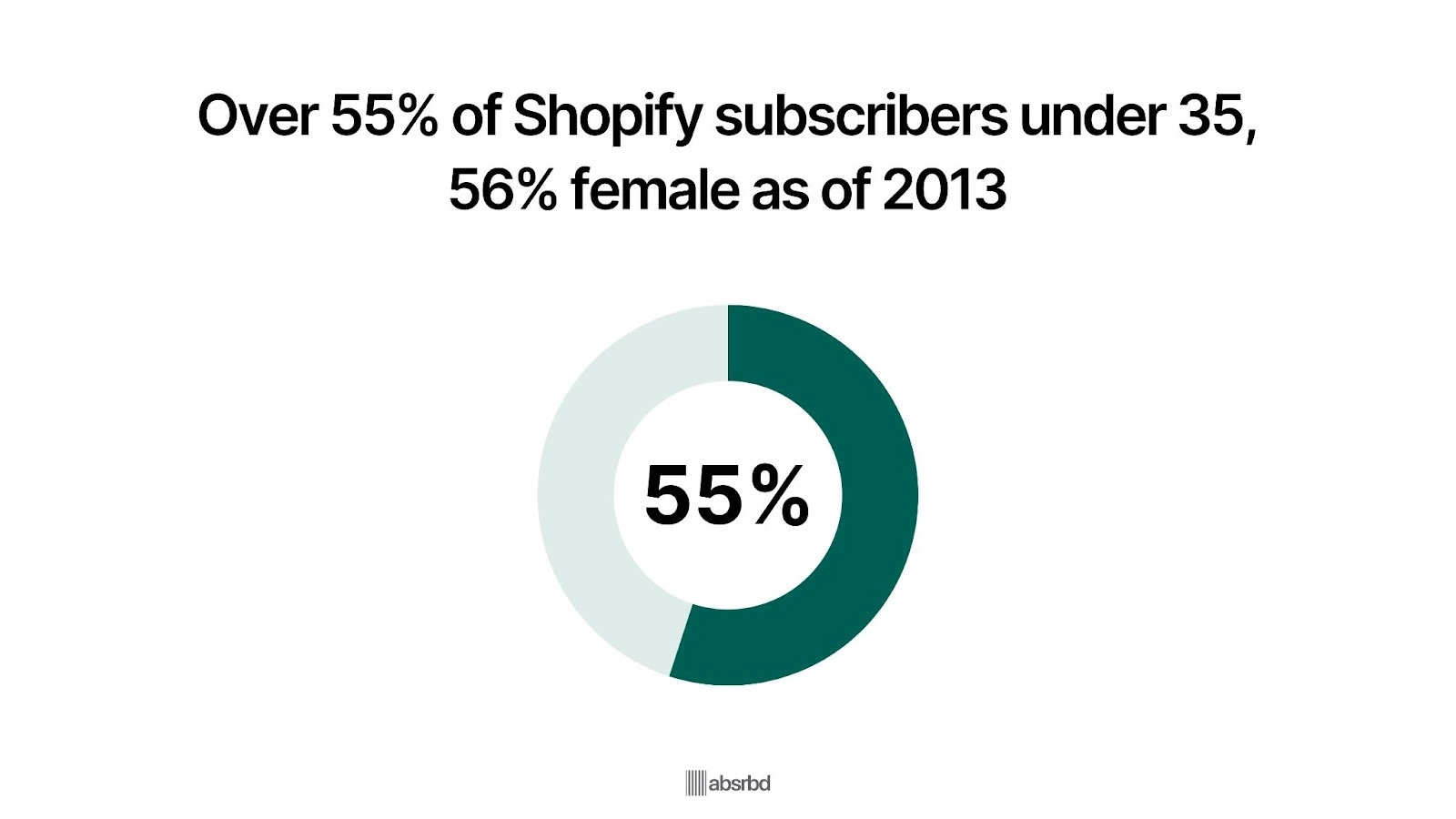

- As of 2013, more than half 55% of Shopify subscribers are under 35 years old, with women representing 56%.

- Over 130 countries are reported to be investigating the use or adoption of central bank digital currencies CBDCs.

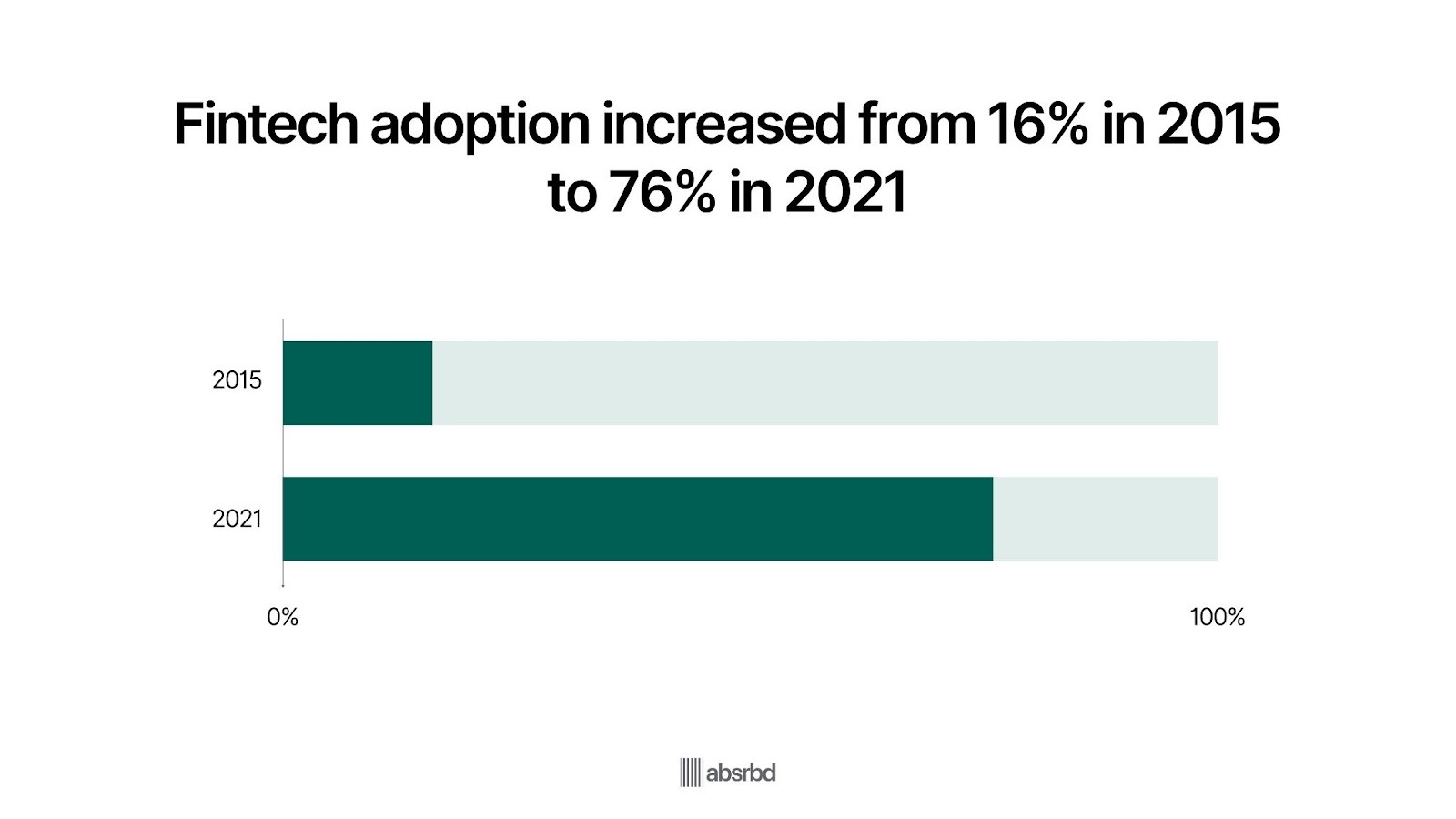

- Adoption of FinTech services has moved steadily upward, from 16% in 2015 to 33% in 2017, to 64% in 2019 EY to 76% account ownership among the global population in 202.

Overview of Money as a Service

Money as a Service MaaS emerged in the last decade, driven by the demand for more accessible and integrated financial solutions.

It refers to delivering financial services through digital platforms, allowing businesses and consumers to manage Money seamlessly.

Since its inception, MaaS has experienced rapid growth, with notable milestones such as the rise of embedded finance and the integration of payment solutions into non-financial platforms.

MaaS platforms incorporate essential elements that support each application. Typically, businesses connect to MaaS services via an API Application Programming Interface, enabling seamless integration with their current online systems or websites.

Companies can leverage MaaS offerings to deliver various financial functions, such as payment processing, international transfers, foreign exchange, and digital wallet solutions. Major players include fintech companies like Square, PayPal, and Stripe, while advancements in technology and changing consumer preferences continue to shape the industry's trajectory.

With the global digital payments market projected to reach $11.53tn in 2024, MaaS plays a crucial role in the evolution of financial services, making it a key area of focus for businesses, investors, and regulators alike. Statista

This innovative approach not only enhances convenience but also promotes financial inclusion, making it accessible to a broader audience.

Key Statistics

- The global payment as a service market was valued at $13.88 billion in 2022 and is expected to expand at a compound annual growth rate CAGR of 15.2% from 2023 to 2030. Grand View Research

- The global Money as a Service MaaS market is projected to reach around USD 39.8 billion by 2026. Research Nester

- Adoption of FinTech services has moved steadily upward, from 16% in 2015, to 33% in 2017, to 64% in 2019 EY to 76% account ownership among the global population in 2021World Bank

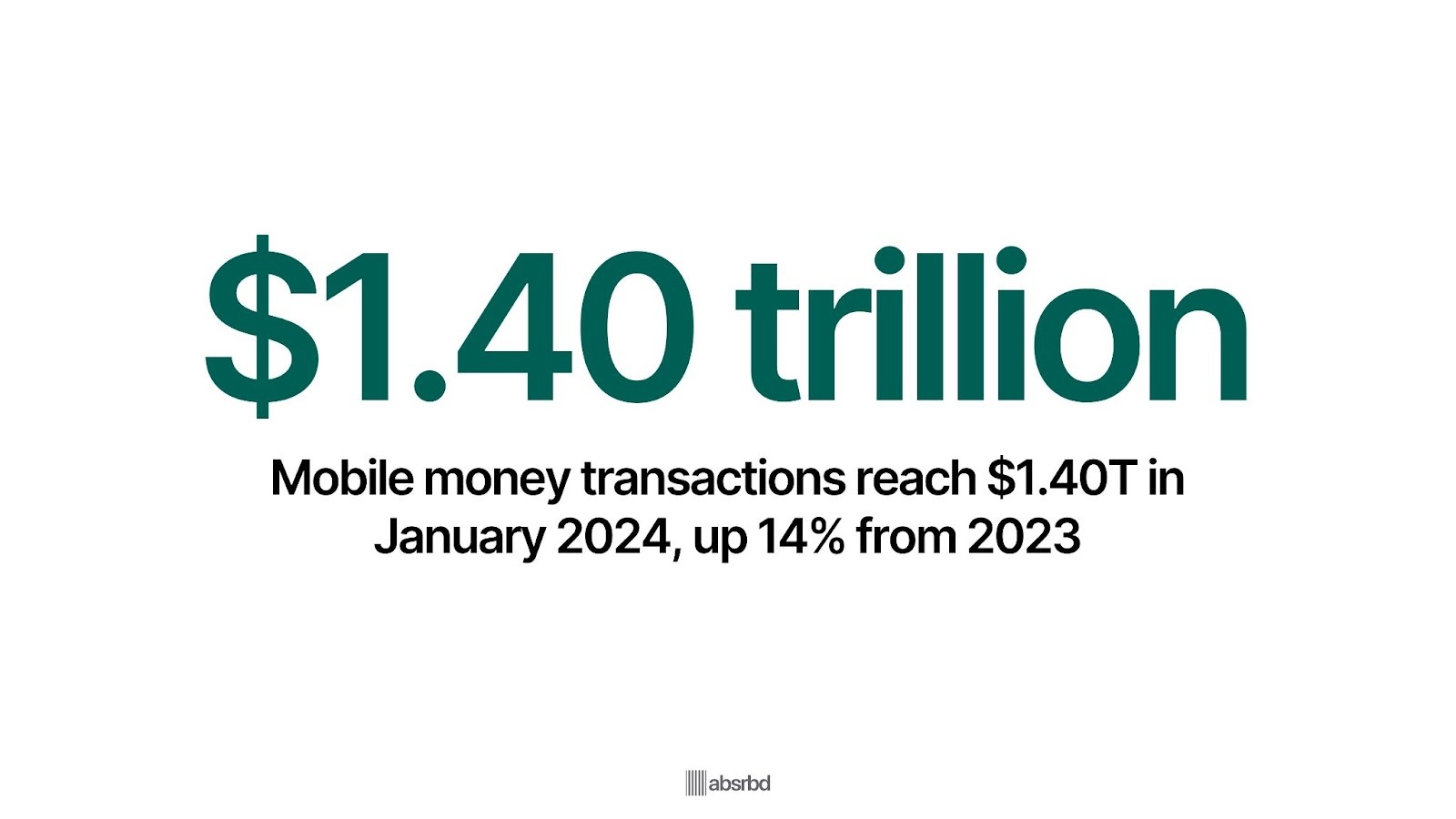

- Mobile money transactions worldwide reached $1.40 trillion by January 2024, showing a strong 14% growth from $1.26 trillion in January 2023. Digital Virgo

- Sub-Saharan Africa is leading the way in MaaS with 835 million registered accounts, followed by South Asia with 401 million, East Asia and Pacific with 374 million, Middle East and North Africa with 71 million, Latin America and the Caribbean with 48 million, and Europe and Central Asia with 26 million. GSMA

- As of 2013, more than half 55% of Shopify subscribers are under 35 years old, with women marking 56%. Business of Apps

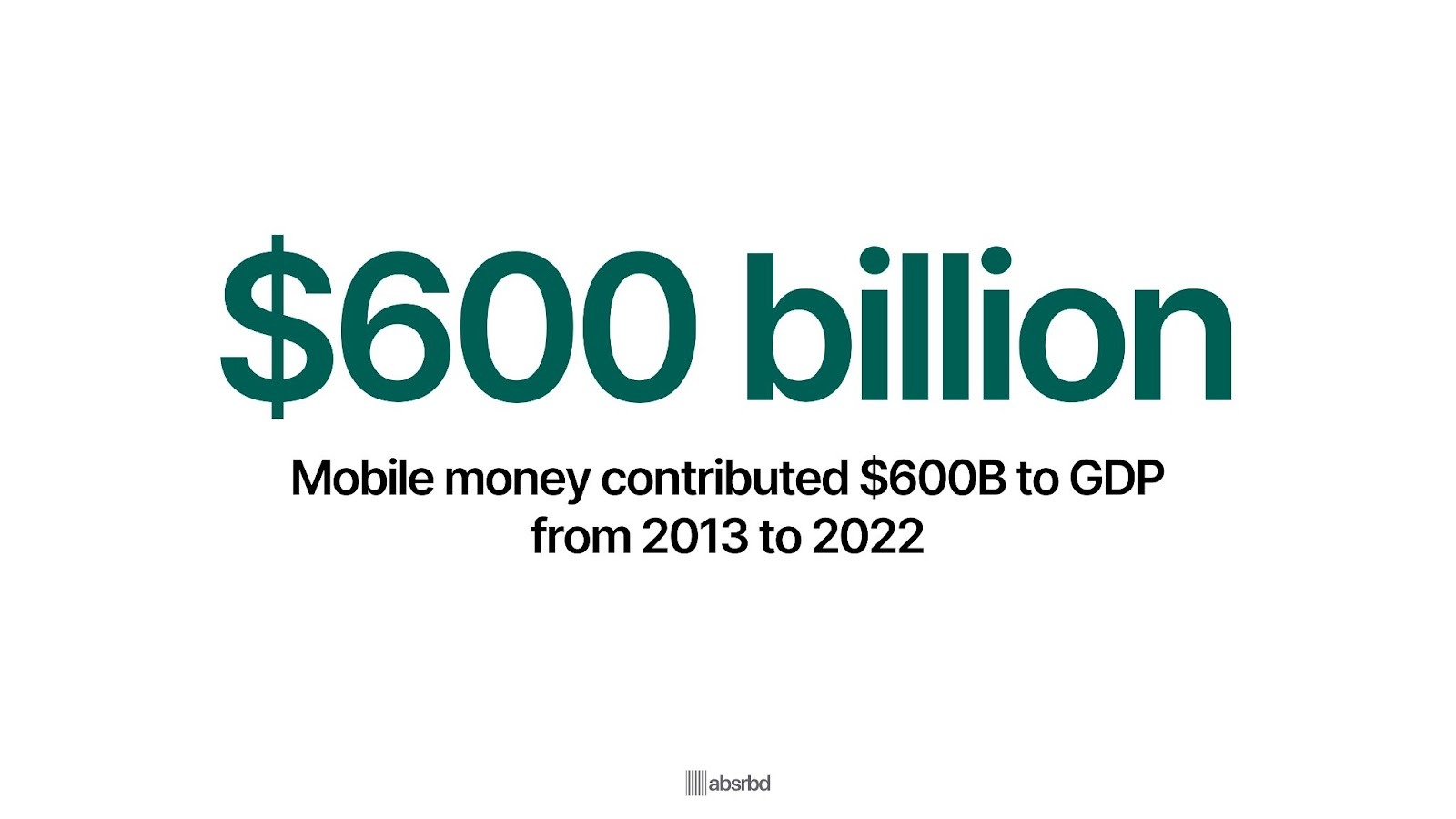

- In the 10 years to 2022, mobile money contributed $600 billion to the GDP of countries with a mobile money service. GSMA

- Payments revenues increased by 11% in 2022, marking a double-digit growth rate for the second consecutive year and reaching an all-time high of over $2.2 trillion. McKinsey

Key Trends Driving Money As a Service

The money-as-a-service MaaS market is changing rapidly, and several key trends are shaping its future.

Here are the most significant developments based on recent data and industry analysis:

Embedded Finance Driving Innovation

The embedded finance market is projected to reach $7.2 trillion by 2026, growing at a CAGR of 21.1%. FinTech Weekly

By integrating financial services directly into non-financial platforms, companies can enhance customer experiences and unlock new revenue streams.

For example, Shopify has successfully embedded payment processing, lending, and financial management tools into its e-commerce platform, enabling merchants to manage their finances seamlessly.

Surge in Digital Payments

The global digital payments market is expected to reach $11.53tn in 2024, growing at a CAGR of 9.52%, and projected to reach US$16.59tn by 2028 Statista.

The increasing adoption of mobile devices and the rise of e-commerce are driving this course, as consumers demand convenient and secure payment methods.

Companies like PayPal and Stripe are capitalizing on this growth by expanding their service offerings and enabling businesses to accept digital payments.

Personalization Through Data Analytics

As consumers increasingly seek personalized financial experiences, MaaS platforms are leveraging data analytics and A.I. to offer tailored recommendations and services.

According to the 2017 online survey of 1,000 consumers ages 18-64, the appeal for personalization is high, with 80% of respondents indicating they are more likely to do business with a company if it offers personalized experiences and 90% indicating that they find personalization appealing. Epsilon

While 90% of leading marketers say personalization primarily contributes to business profitability Think with Google

Companies that effectively harness this data-driven approach can differentiate themselves in a competitive market and enhance customer loyalty.

4.4 Billion Digital Wallets Users By 2025

Digital wallets are becoming increasingly popular as a convenient and secure method of payment.

This is remarkable because it's reshaping how consumers interact with Money and make purchases.

According to a report by Stripe, digital wallet users are expected to reach 4.4 billion globally by 2025, up from 2.6 billion in 2020, representing nearly 60% of the world's population.

From the Visa survey, 16% of customers are already exclusively using digital payment methods, and 25% say they anticipate making the transition over the next two years.

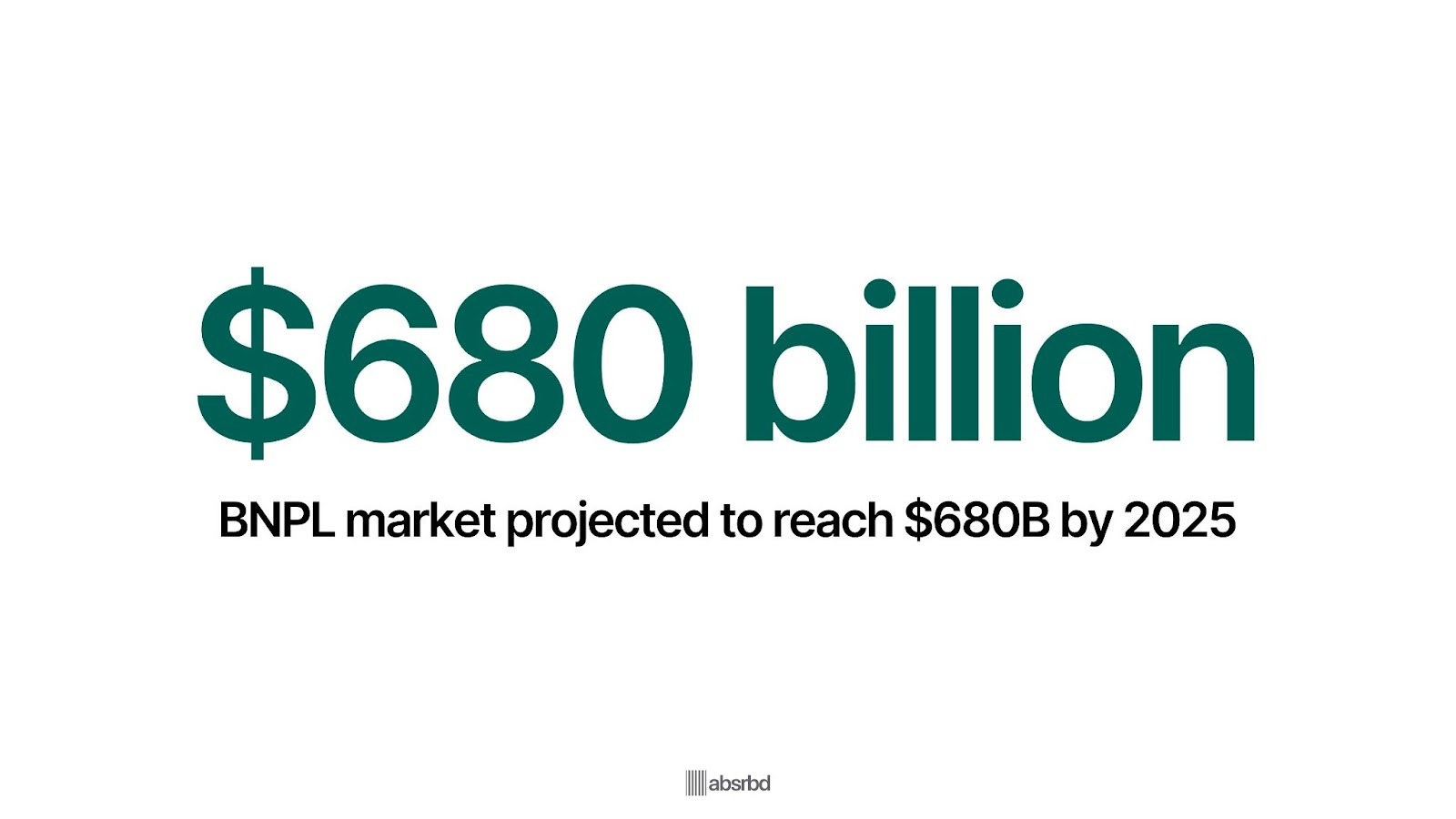

BNPL Market To Reach $680 billion By 2025

BNPL services are gaining traction as an alternative to traditional credit cards.

This shift is important because it's changing consumer credit behavior and attracting younger demographics.

The global Buy Now Pay Later market is projected to grow from $285 billion in 2018 to $680 billion by 2025, according to a report by Precedence Research.

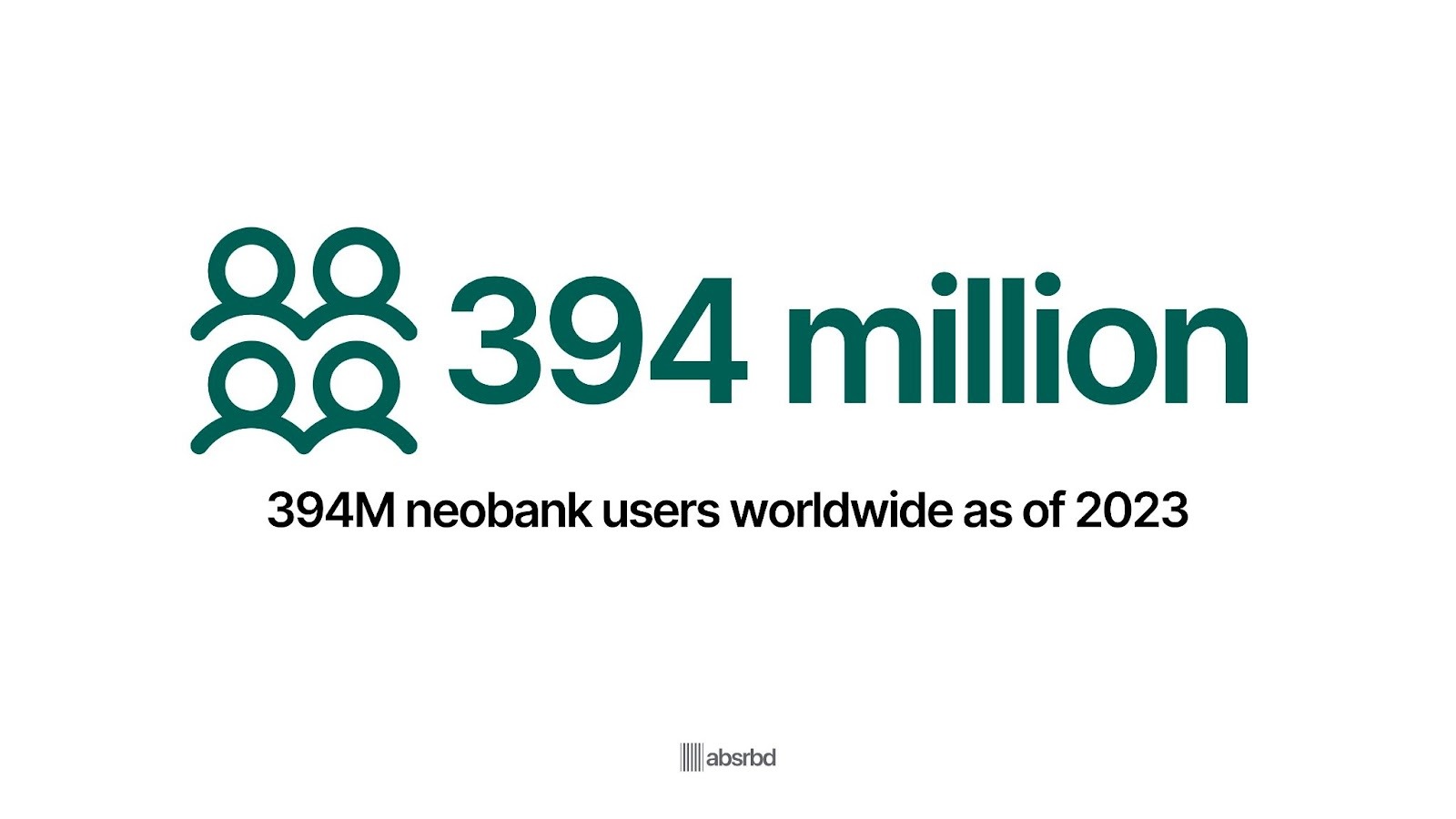

394 million Neobank Users Worldwide As Of 2023

Neobanks, or digital-only banks, are growing rapidly, offering lower fees and more user-friendly interfaces than traditional banks.

The rise of Neobanks is crucial because it's disrupting traditional banking models and improving financial inclusion.

According to Statista, neobanks are expected to reach $6.37tn in 2024 and 386.30 million users by 2028.

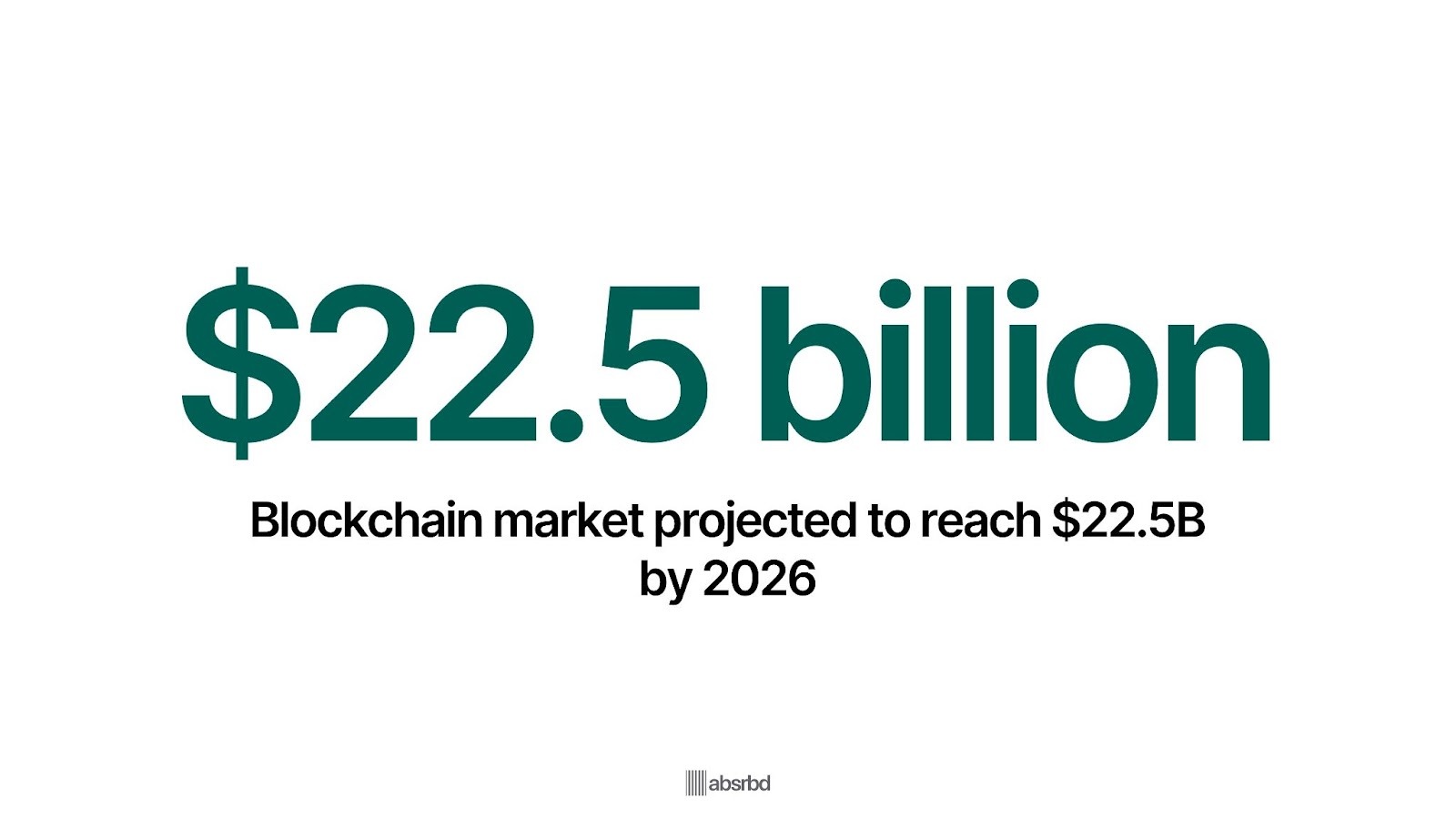

Blockchain Market to Reach $22.5 billion by 2026

Blockchain technology is being adopted for various financial applications, including cross-border payments and smart contracts.

This shift is important as it has the potential to increase transparency and reduce costs in financial transactions.

Market sand Markets forecasts that the global Blockchain market size is projected to grow from $20.1 billion in 2024 to $248.9 billion by 2029 at a Compound Annual Growth Rate CAGR of 65.5% during the period of the forecast. Yahoo Finance

Sustainable Finance Gaining Traction

The demand for sustainable financial products is growing as consumers and businesses seek to ensure their money is not being used to cause harm to the environment or society.

According to a report by the Global Sustainable Investment Alliance, 35.9% of global assets under management were invested in sustainable strategies in 2020

MaaS platforms that offer green financial products and services can tap into this growing market and contribute to a more sustainable financial ecosystem.

Digital and Crypto Currencies Back in the Spotlight

Digital currencies and cryptocurrencies are firmly back on the radar of financial services in 2024.

Over 130 countries are reported to be investigating the use or adoption of central bank digital currencies CBDCs Science Direct, while Bitcoin's recovery from its 2021 crash is attracting renewed interest from innovators and investors.

Outside of CBDCs, further movement towards governance and regulation of the crypto space is also anticipated.

Key Challenges Facing the Money as a Service Sector

The Money as a Service MaaS sector faces several key challenges that can hinder its growth and effectiveness.

Here are some of the major issues, supported by statistics and relatable examples:

Cybersecurity and Fraud Prevention

Cybercrime poses a serious risk to the MaaS sector, with financial services being prime targets due to the sensitive information they handle.

In 2023, the financial sector experienced a 233% increase in ransomware attacks, highlighting the urgent need for robust cybersecurity measures. U.K. Parliament

For instance, in 2021, a major cyberattack on a financial institution compromised the data of over 100 million customers, leading to substantial reputational damage and regulatory scrutiny. ACM Digital Library

The cost of cybercrime is expected to reach $10.5 trillion annually by 2025, up from $3 trillion in 2015. Business Standard

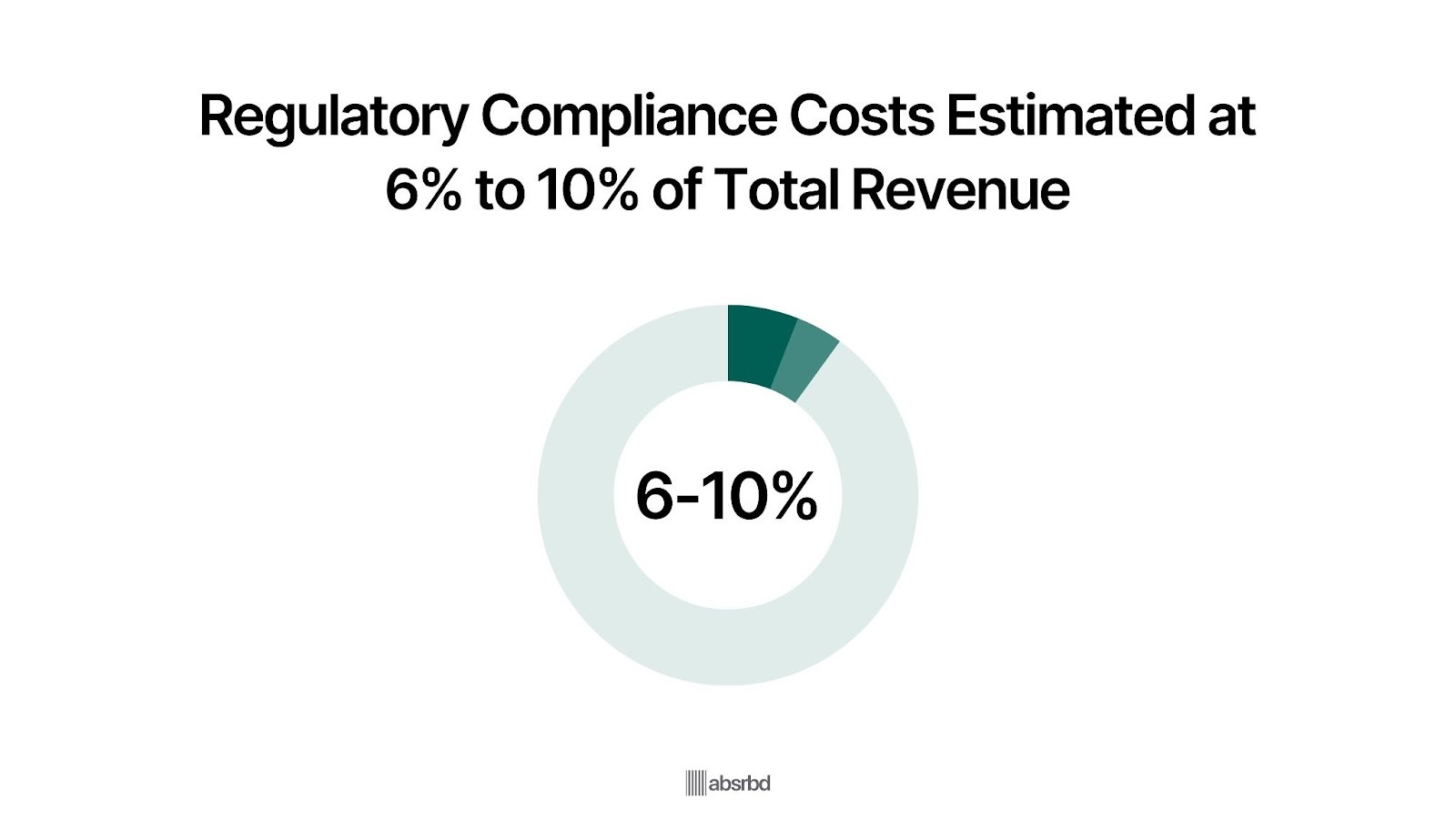

Regulatory Compliance

The constantly changing regulatory framework presents a challenge for MaaS providers.

Financial institutions must navigate complex regulations, including anti-money laundering AML and Know Your Customer KYC requirements.

The cost of regulatory compliance for financial institutions is estimated to be between 6% to 10% of their total revenue. Ascent

Failure to comply can lead to hefty fines and loss of customer trust.

Data Privacy Concerns

With the increasing use of personal data in financial services, ensuring data privacy has become crucial.

The Global Data Protection Regulation GDPR in Europe has set a new standard for data protection, with fines for non-compliance reaching up to €20 million or 4% of global turnover, whichever is higher. Intersoft Consulting

In 2021, financial services firms faced alarming GDPR fines, with Amazon paying €746 million $877 million. Tessian

Competition from Big Tech

Traditional financial service providers and fintech startups are facing increasing competition from big tech companies entering the financial services space.

A report by the Financial Stability Board estimates that fintech credit flows reached $223 billion in 2019, while big tech credit reached $572 billion globally in 2019. CEPR

Financial Literacy and Inclusion

Despite the growth of digital financial services, a large portion of the world population remains unbanked or underbanked.

The World Bank reports that approximately 1.7 billion adults globally remain unbanked as of 2017.

Low levels of financial literacy further exacerbate this issue, as many individuals do not understand how to utilize available financial tools effectively.

Bridging this gap requires overcoming infrastructure, education, and trust barriers.

Emerging Opportunities in Money as a Service Sector

The Money as a Service sector is witnessing a surge of emerging opportunities driven by technological advancements and changing consumer preferences.

Here are some key opportunities supported by statistics and relatable examples:

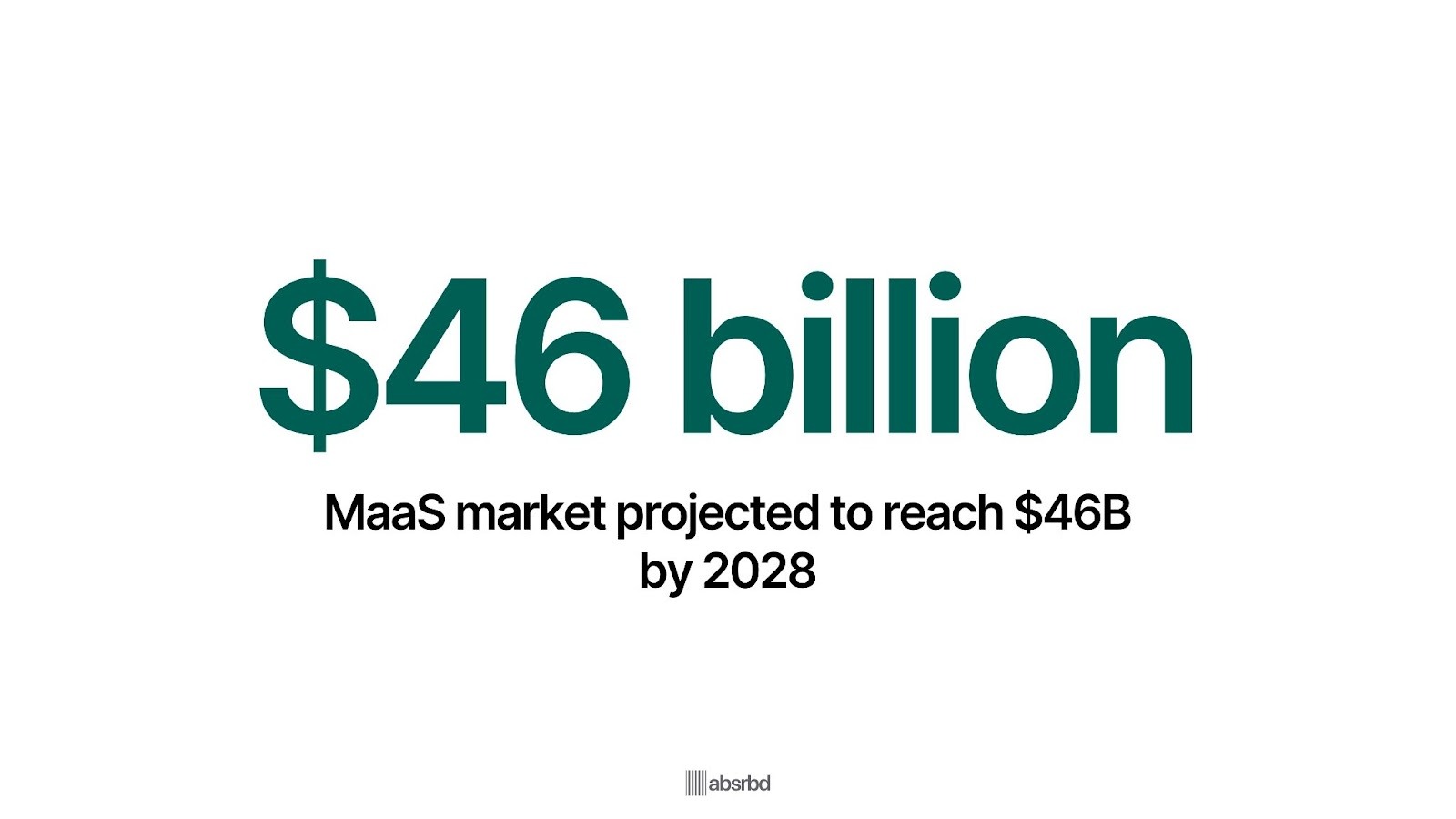

Seamless Integration of Financial Services

MaaS allows businesses to integrate financial services directly into their platforms through APIs.

This integration is expected to drive the sector's growth, with the MaaS market projected to reach $46 billion by 2028. Payset

Companies like Shopify, Uber, and Square are leveraging this opportunity by offering payment processing, lending, and financial management tools directly within their platforms, enhancing user experience and driving revenue growth.

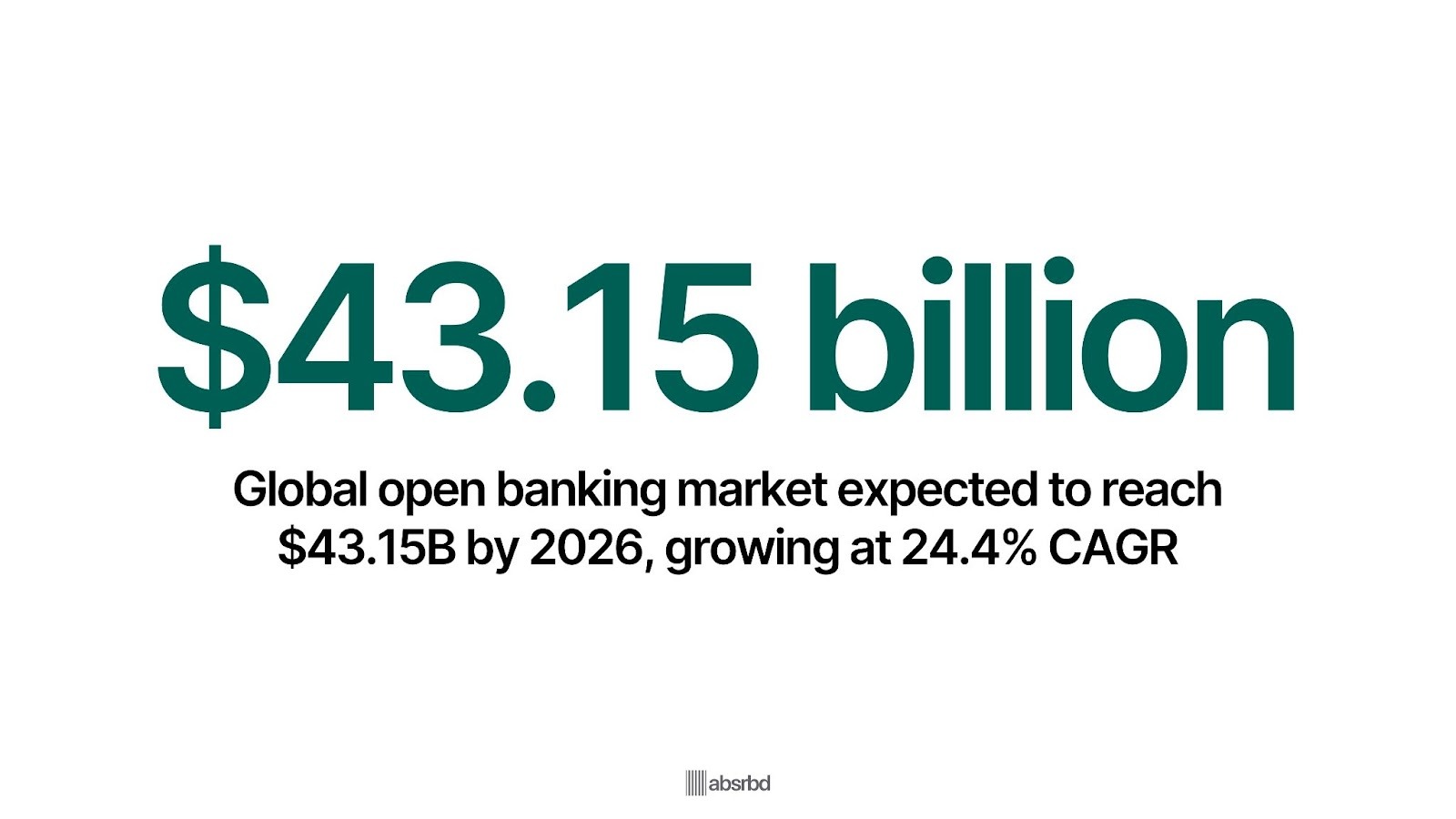

Open Banking and API Integration

Open banking is creating new opportunities for financial service providers to offer innovative products and services.

According to Allied Market Research, the global open banking market is expected to reach $43.15 billion by 2026, growing at a CAGR of 24.4% from 2019 to 2026. EIN Presswire

For example, Plaid, a fintech company that enables easy API integrations, was valued at $13.4 billion in 2021, demonstrating the high potential in this area. Forbes

Financial Services for the Gig Economy

The growing gig economy presents opportunities for tailored financial services.

A report by Mastercard estimates that the global gig economy transactions will grow by 17% annually to approximately $455 billion by 2023. H.R. Forecast

Companies like Payoneer are capitalizing on this shift by offering specialized payment solutions for freelancers and gig workers.

Blockchain and Decentralized Finance DeFi

Blockchain technology and DeFi are creating new opportunities in areas like cross-border payments and decentralized lending.

According to DeFi Pulse, the total value locked in DeFi protocols grew from about $1 billion in June 2020 to over $50 billion by April 2024. Exploding topics

For example, Compound, a DeFi lending protocol, has facilitated billions of dollars in loans without traditional intermediaries.

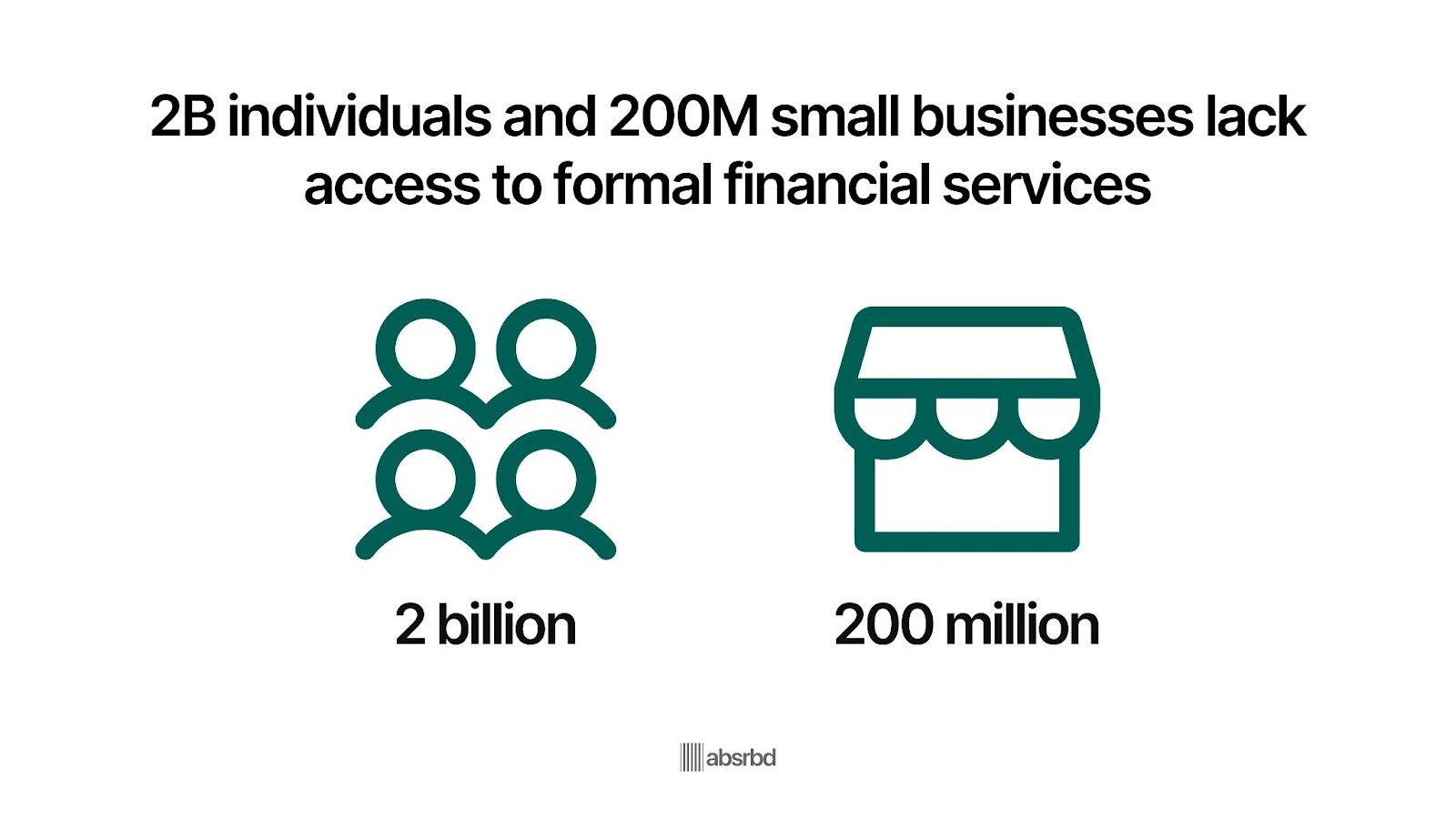

Financial Inclusion in Emerging Markets

MaaS is poised to tremendously improve financial inclusion, particularly in emerging markets where traditional banking services are limited.

Approximately 2 billion individuals and 200 million small businesses in these regions lack access to formal financial services. McKinsey

By providing mobile money solutions, companies can tap into this largely underserved market, which could increase the volume of loans extended by $2.1 trillion. McKinsey

Demand for Personalized Financial Solutions

As consumers increasingly seek personalized financial services, MaaS platforms are utilizing A.I. and data analytics to offer tailored recommendations and services.

This shift is remarkable as 69% of U.S. consumers prefer personalized financial experiences, which can enhance customer loyalty and retention. Forbes

Companies that effectively harness this data-driven approach can differentiate themselves in a competitive market.

Expansion of Digital Payment Solutions

The rapid growth of e-commerce is driving demand for digital payment solutions.

The global digital payments market is projected to reach $16.59tn by 2028, creating vast opportunities for MaaS providers to offer innovative payment solutions, such as contactless payments and mobile wallets. Statista

Companies like PayPal and Stripe are capitalizing on this movement by expanding their service offerings to include advanced payment processing capabilities.

Impact on Stakeholders

From consumers to financial institutions, to businesses and regulators, MaaS have several impacts on sta

Consumers

MaaS has greatly improved financial accessibility and convenience for consumers. According to a 2023 report by Plaid, 88% of Americans now use fintech apps to manage their finances. Plaid

This increased accessibility has led to:

- Improved financial inclusion: The World Bank reports that globally, 76% of adults now have a bank account, up from 68% in 2017, partly due to mobile money services.

- Enhanced user experience: The integration of data analytics in MaaS allows for personalized financial solutions tailored to individual needs.

- Enhanced Digital Transactions: The ability to transact digitally has been a game changer as it allows consumers to receive Money digitally with ease.

- Cost Savings on Banking Fees: MaaS platforms often provide lower fees compared to traditional banks, which is crucial for low-income consumers.

Traditional Banks

MaaS has forced traditional banks to innovate and adapt:

- Digital transformation, integrating technology.

- Partnerships with fintech, as banks enter into partnerships with fintech companies to enhance their digital offerings. PYMNTS

Fintech Companies

MaaS has created a booming fintech industry:

- Market growth: According to KPMG's Pulse of Fintech report, global fintech investment reached $210 billion in 2022.

- Increased valuations: As of 2023, there were over 200 fintech unicorns globally, with a combined valuation exceeding $900 billion and the U.S. having 166. Statista

For example, Stripe, a payment processing platform, was valued at $95 billion in 2021, making it one of the most valuable private companies in the world.

Small and Medium Enterprises SMEs

MaaS has provided SMEs with better access to financial services:

- Improved lending: The World Bank estimates that the global SME finance gap has decreased from $5.2 trillion in 2017 to $4.8 trillion in 2022, partly due to alternative lending platforms.

- Enhanced financial management: A 2023 survey by Intuit QuickBooks found that 83% of small businesses use at least one fintech app to manage their finances.

For example, Square Capital, a fintech lender, has provided over $9 billion in loans to small businesses since its inception.

Regulators

MaaS has presented new challenges and opportunities for regulators:

- Increased focus on fintech regulation: The Financial Stability Board reports that 65% of its member jurisdictions have made changes to their regulatory framework to address fintech developments as of 2023.

- Cross-border collaboration: The Global Financial Innovation Network GFIN, launched in 2019, now includes over 70 organizations working together on fintech regulation.

For instance, the European Union's revised Payment Services Directive PSD2 has set new standards for open banking and payment services, influencing global regulatory approaches.

Investors

MaaS has created new investment opportunities:

- Venture capital investment: According to C.B. Insights, global fintech funding reached $75.2 billion in 2022.

- Public market performance: The Global X FinTech ETF, which tracks the fintech sector, has outperformed the S&P 500 over the past five years.

Ant Group's IPO in 2020, although eventually suspended, was poised to be the largest in history at $34.5 billion, highlighting investor enthusiasm for fintech.

Conclusion

The Money as a Service sector faces both challenges and opportunities.

While cybersecurity threats and regulatory compliance pose major hurdles, the potential for innovation and financial inclusion remains key.

The rapid growth of digital wallets, projected to reach 4.4 billion users by 2025, illustrates this duality.

Industry players navigating this space must balance innovation with security and regulatory compliance.

Those who successfully leverage emerging technologies like A.I. and blockchain while maintaining robust security measures are likely to gain a competitive edge and capture larger market shares.

As we look to the future, the ability to adapt quickly to changing consumer needs and technological advancements will separate the leaders from the followers in the technology driven world of Money as a Service.

The sector's future hinges on creating seamless, secure, and inclusive financial experiences for a global user base.

Frequently Asked Questions

1. What is an MSB?

A money services business (MSB)is any business that transmits or converts Money for its customers or clients. MSBs are considered financial institutions under the Bank Secrecy Act BSA and are required to implement anti-money laundering measures.

2. What is a Unicorn Company?

A unicorn company is a privately held company that’s valued at $1 billion or more.

.jpg)