.jpg)

111 NE 1st ST

Miami, Florida 33132

USA

The rise of mobile-first finance, embedded services, and AI-driven personalization is transforming how people and businesses manage money, while new regulations and shifting consumer expectations are reshaping the business environment.

With so much change underway, it can be hard to keep track of the numbers that really matter.

That’s why this neobanking statistics 2026 report pulls together the latest figures, forecasts, and trends to give you a clear view of where digital banking stands today, and where it’s heading next.

Highlights from this year’s data include:

- The global neobanking market surpassing USD 550 billion in 2026

- Transaction values on track to hit €10 trillion by 2028

- Nearly 400 million people worldwide expected to be using neobanks by 2028

- SME and business banking already generating two-thirds of sector revenues

- Emerging markets in Asia, Latin America, and Africa set to lead the next growth wave

And that’s just the beginning. The following pages unpack the strongest data, trends, opportunities, and predictions shaping the future of neobanking in 2026 and beyond.

Data Sources and Methodology

This article combines open-access resources and proprietary data to present accurate, up-to-date statistics and trends on Neobanking.

Our methodology involves:

- Aggregating data from government databases, industry reports, and academic publications

- Incorporating exclusive insights from leading industry providers

- Regular updates to reflect the latest information

Key data providers include:

While we strive for accuracy, trends in neobanking are shifting rapidly.

These statistics reflect current patterns and should not be considered permanent facts.

Key Takeaways

- The global neobanking market is projected to hit USD 552 billion in 2026.

- Global neobank users are approaching 400 million by 2028.

- Transaction values are forecast to top €9.76 trillion by 2028.

- User penetration will climb from 3.9% in 2024 to 4.8% in 2028.

- 1.4 billion adults remain unbanked, offering vast inclusion opportunities.

- Embedded finance revenues could reach USD 228.6 billion by 2028.

- The BaaS sector will surpass USD 24.6 billion by 2025.

- The UK crossed 13.3 million open banking users in early 2025.

- Biometric fraud peaked at 16% in 2024, underscoring security challenges.

Overview of Neobanking

Neobanks emerged in the early 2010s as a response to the growing demand for digital-first banking solutions.They are financial technology companies that provide banking services exclusively through digital channels, such as mobile apps and websites, without physical branch networks.

Neobanks gained momentum following the 2008 financial crisis, which eroded trust in traditional banking institutions. Designed for mobile-first users, they emphasize speed, low fees, and seamless user experience via apps and web interfaces.

Since 2023, the neobanking industry has entered a steep growth phase. In 2022, the U.S. had about 23.7 million neobank account holders; that number is forecast to reach 34.7 million by 2026, reflecting strong adoption. Statrys

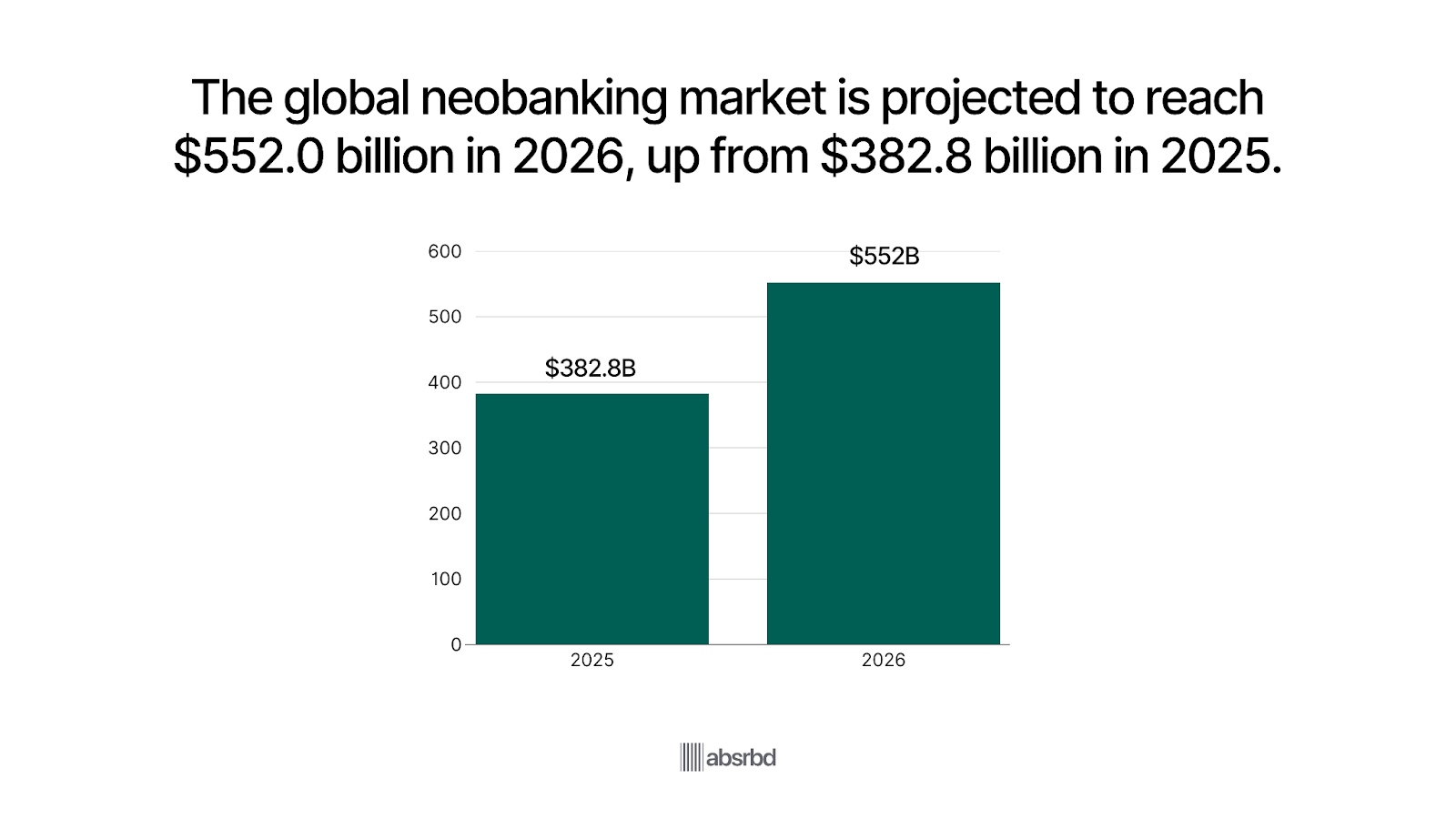

Globally, the number of active neobank users grew from 301.7 million in 2024 to an estimated 350 million by 2025, with projections pointing toward even more by 2026. Market value is expanding rapidly. Estimates place the global neobanking market at about USD 382.8 billion in 2025, rising to approximately USD 552.0 billion in 2026.

This growth is driven by rising fintech adoption, increasing smartphone penetration, and shifting consumer preferences toward digital banking solutions. Regionally, Brazil leads in penetration, with about 43% of the population already using digital-only banking services. North America is also seeing steep growth: the U.S. neobanking market is rising at an estimated CAGR of 34.6% through 2026.

The demographic profile of neobank users remains consistent with earlier trends but strengthened. Users skew young, primarily Millennials and Gen Z, and are comfortable with technology. They use digital banking for more than basic transactions, including budgeting tools, online payments, and cross-border remittances.

Neobanks are increasingly not just challengers to traditional banks, but catalysts for financial inclusion, serving urban and rural populations alike, especially where traditional banking infrastructure is sparse. Features like real-time payments, open banking APIs, mobile wallets, and even embedded finance are now standard expectations.

Key Statistics

- The Global Neobanking market size in 2026 is projected at USD 552.0 billion, up from USD 382.8 billion in 2025. P&S Intelligence

- The global neobanking market was valued at USD 195.11 billion in 2024. IMARC Group

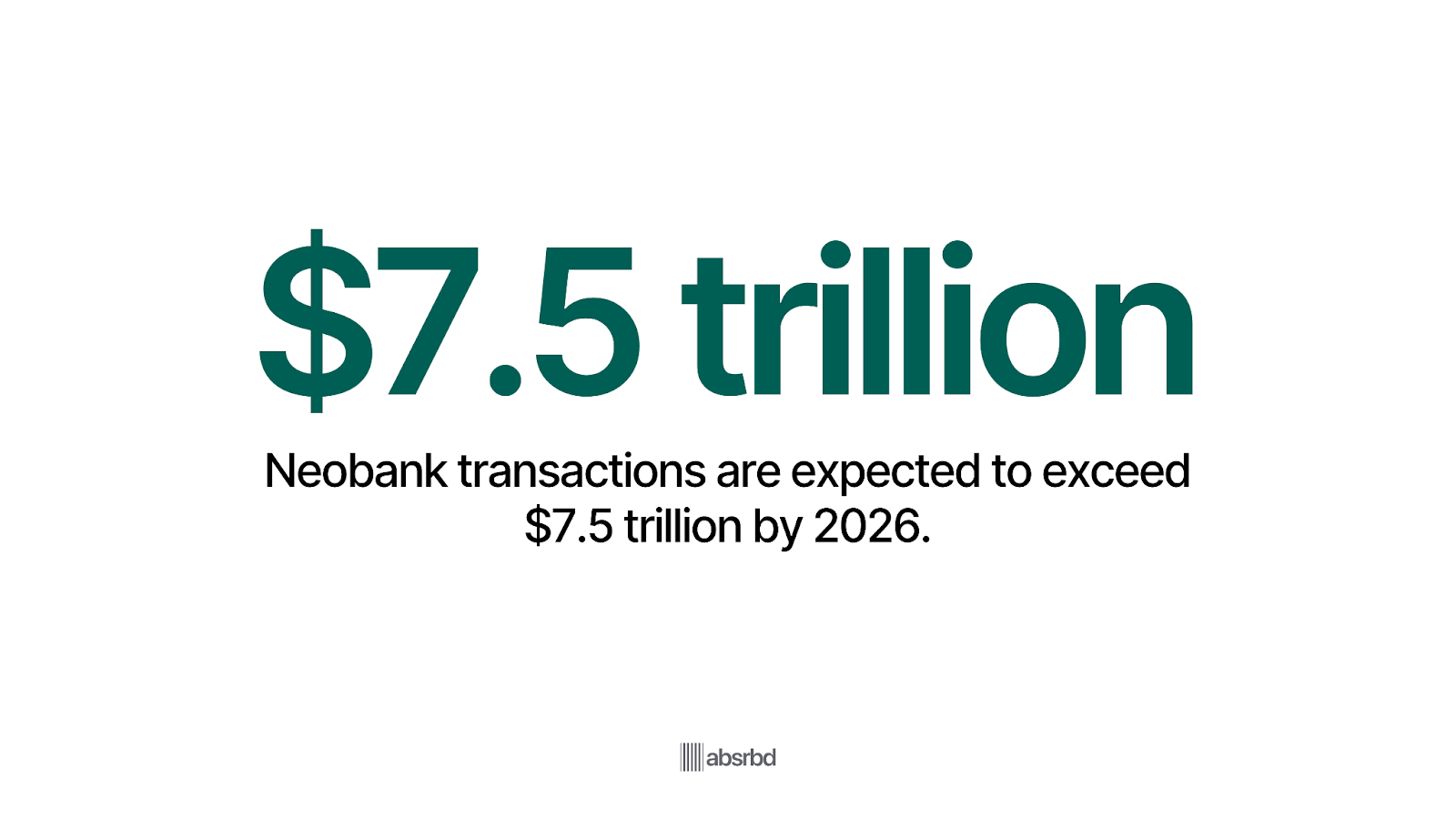

- By 2026, the total transaction value conducted through neobanks is projected to exceed 7.5 trillion USD. SDK Finance

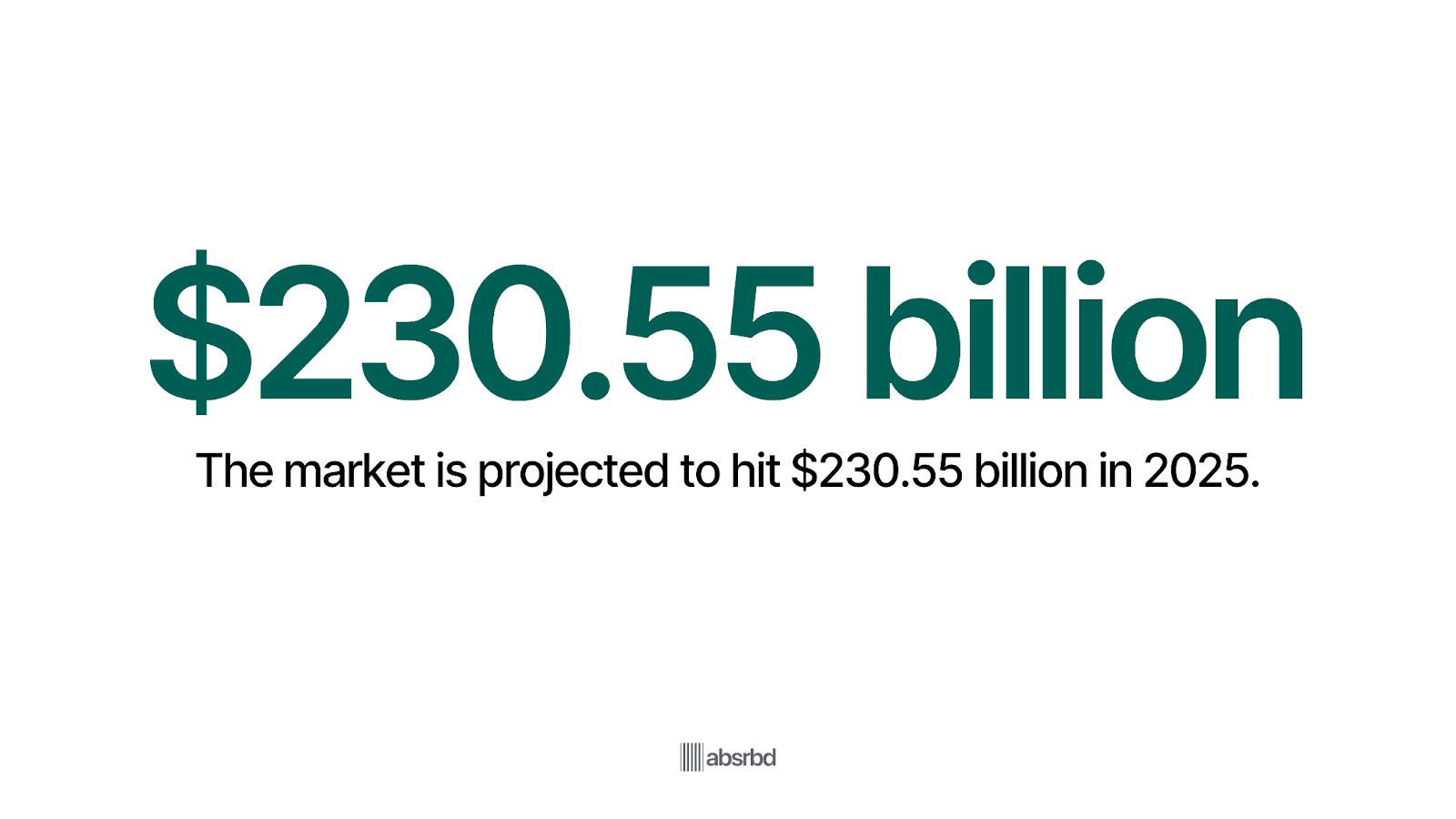

- It is projected to reach USD 230.55 billion in 2025. Precedence Research

- Between 2025 and 2034, the neobanking market is expected to grow at a CAGR of approximately 40.29%. Precedence Research

- By 2034, the global neobanking market size is forecast to reach USD 4,396.58 billion. Precedence Research

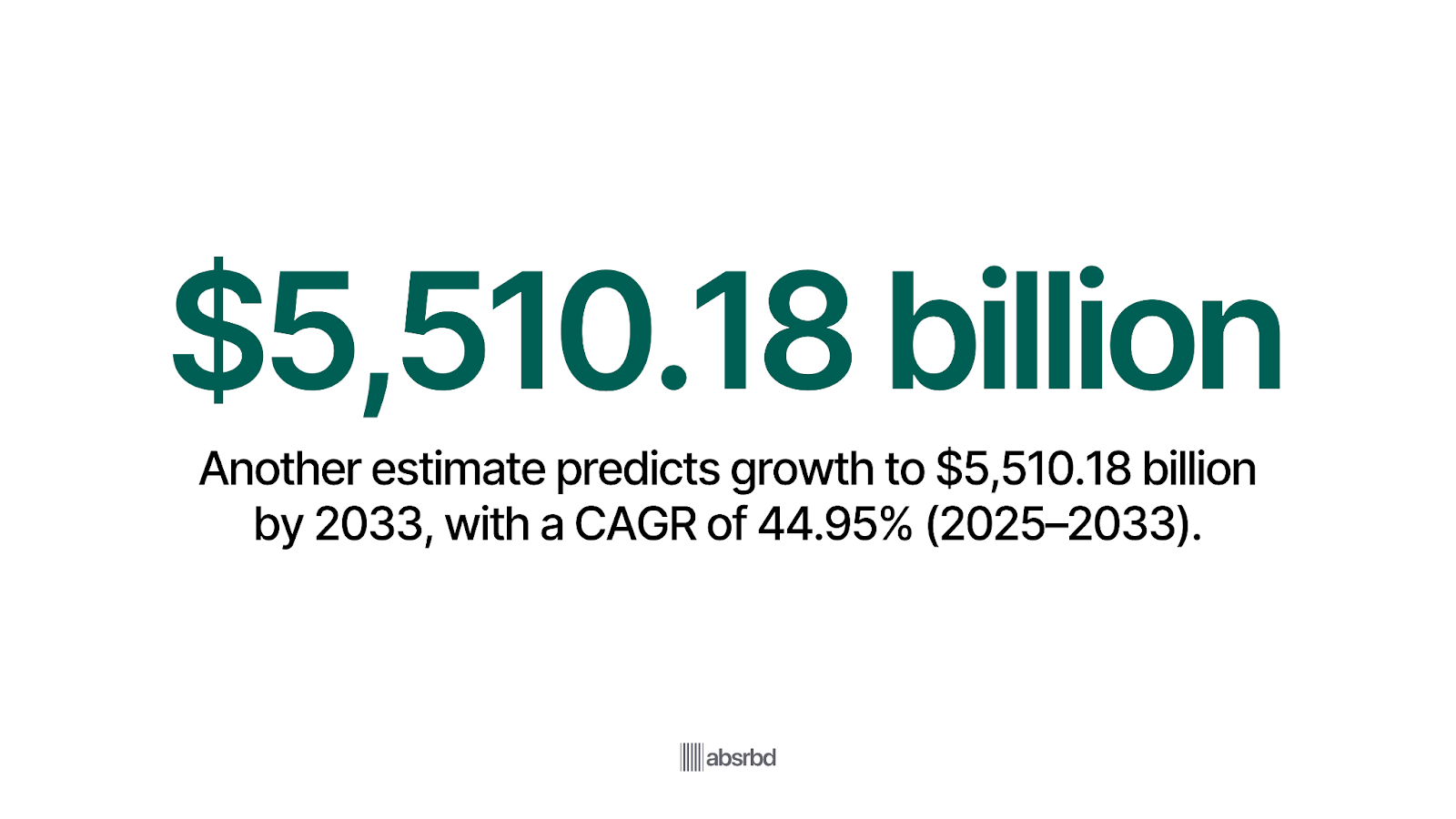

- Another projection estimates the global market will grow to about USD 5,510.18 billion by 2033, with a CAGR of 44.95% from 2025-2033. IMARC Group

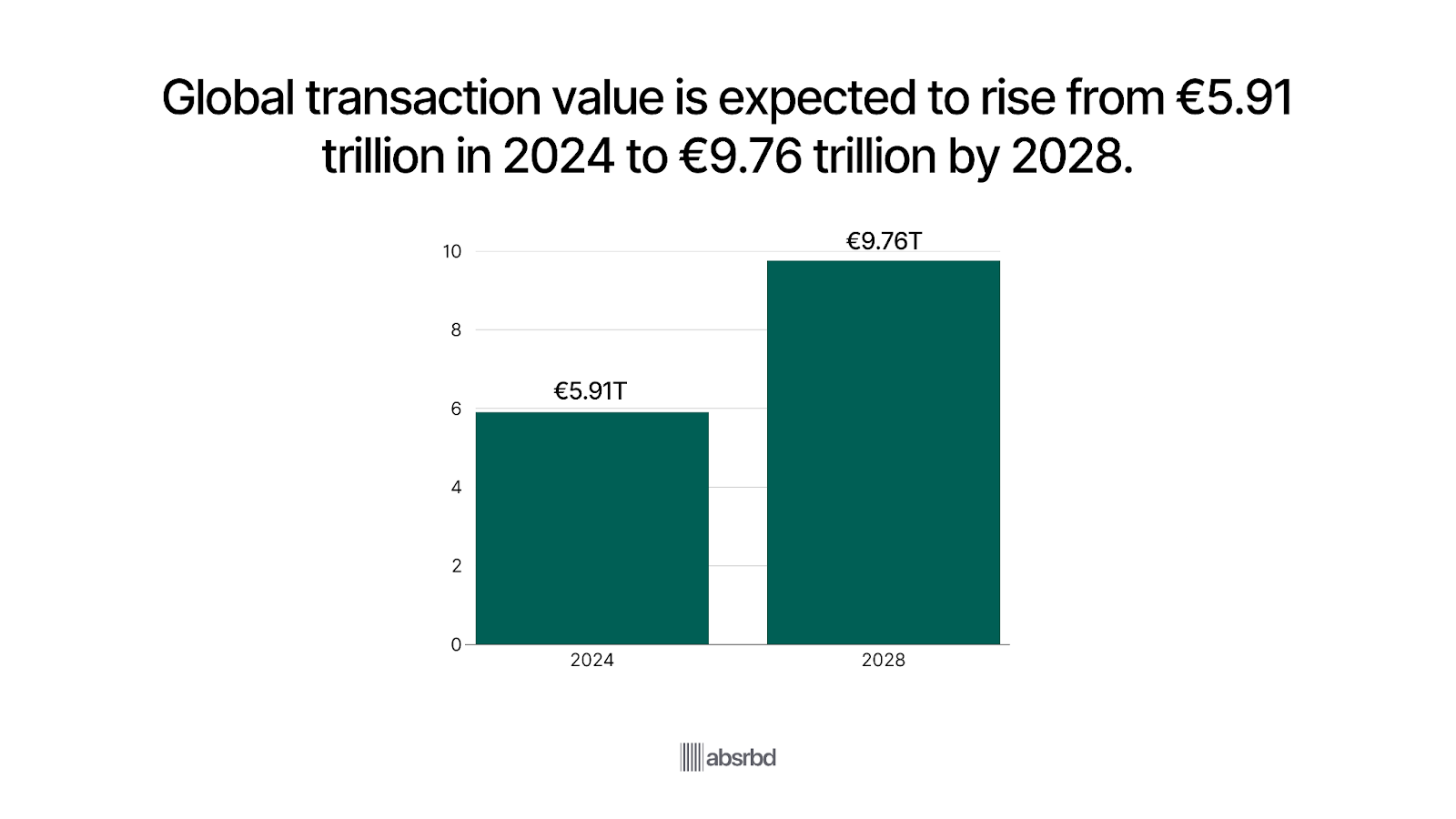

- The worldwide transaction value in the neobanking market was forecast at €5.91 trillion in 2024, with growth to about €9.76 trillion by 2028. Statista

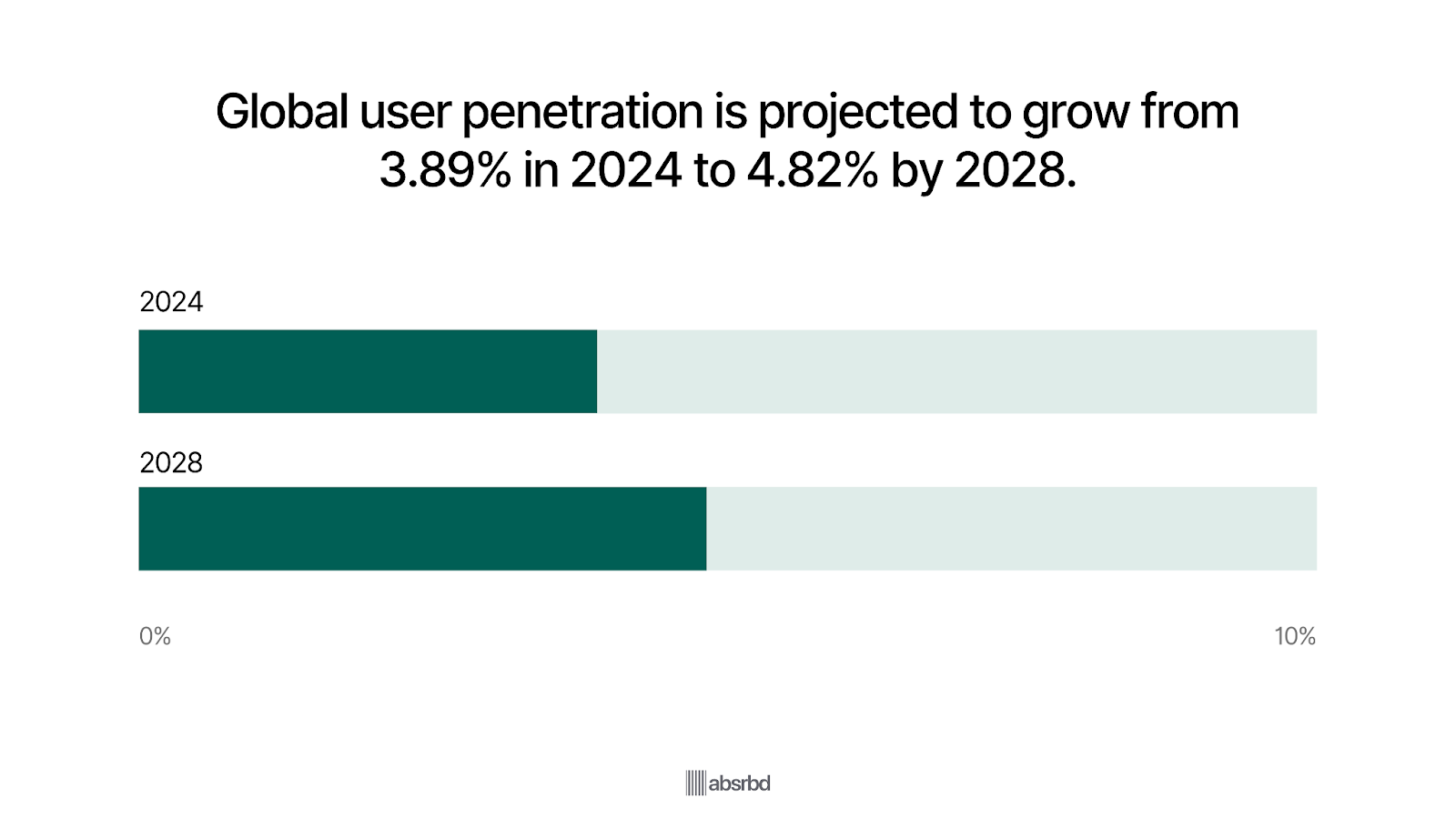

- Global user penetration of neobanking was about 3.89% in 2024, and is expected to rise to 4.82% by 2028. Statista

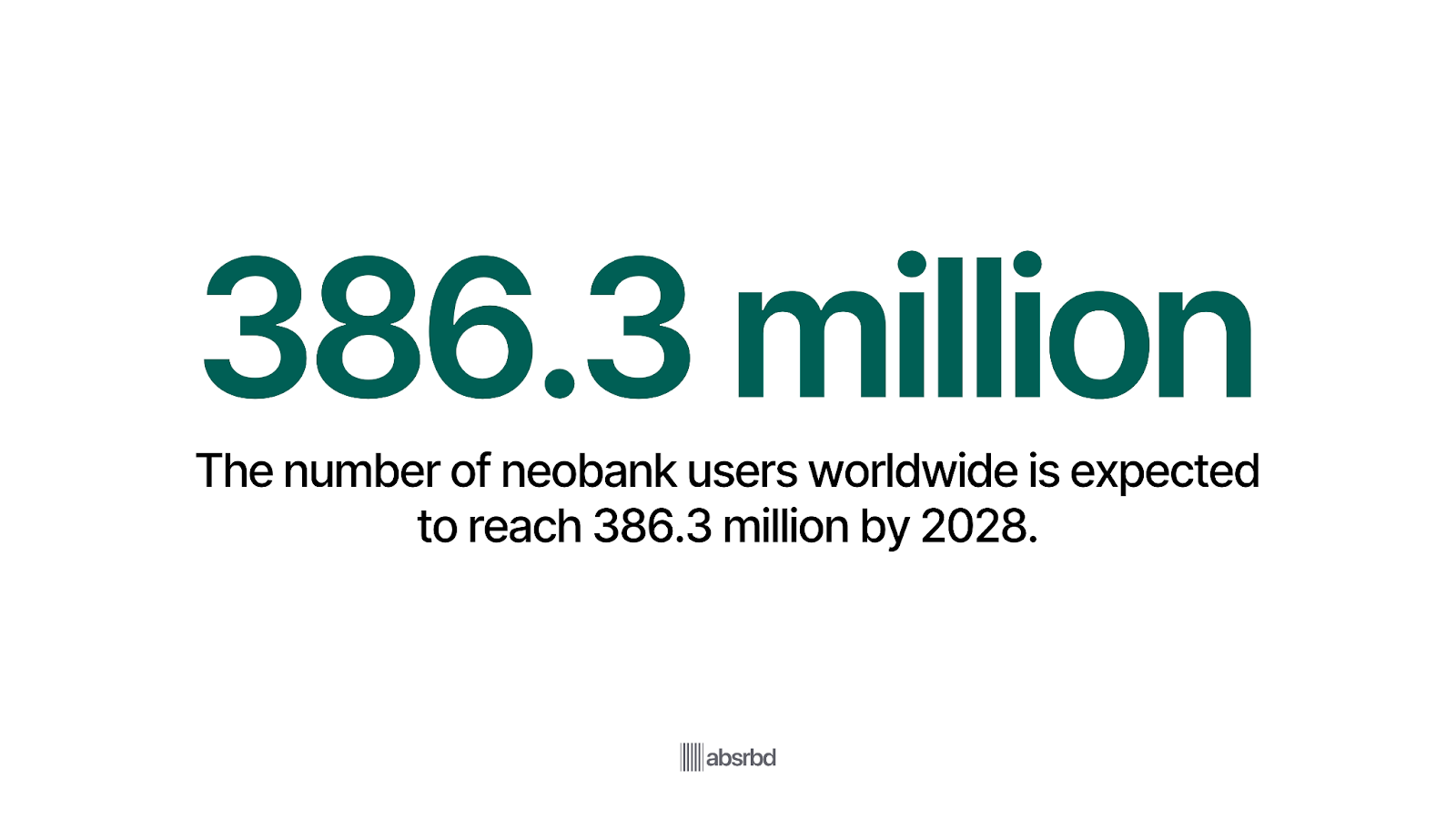

- The number of neobank users globally is projected to reach 386.30 million by 2028. Statista

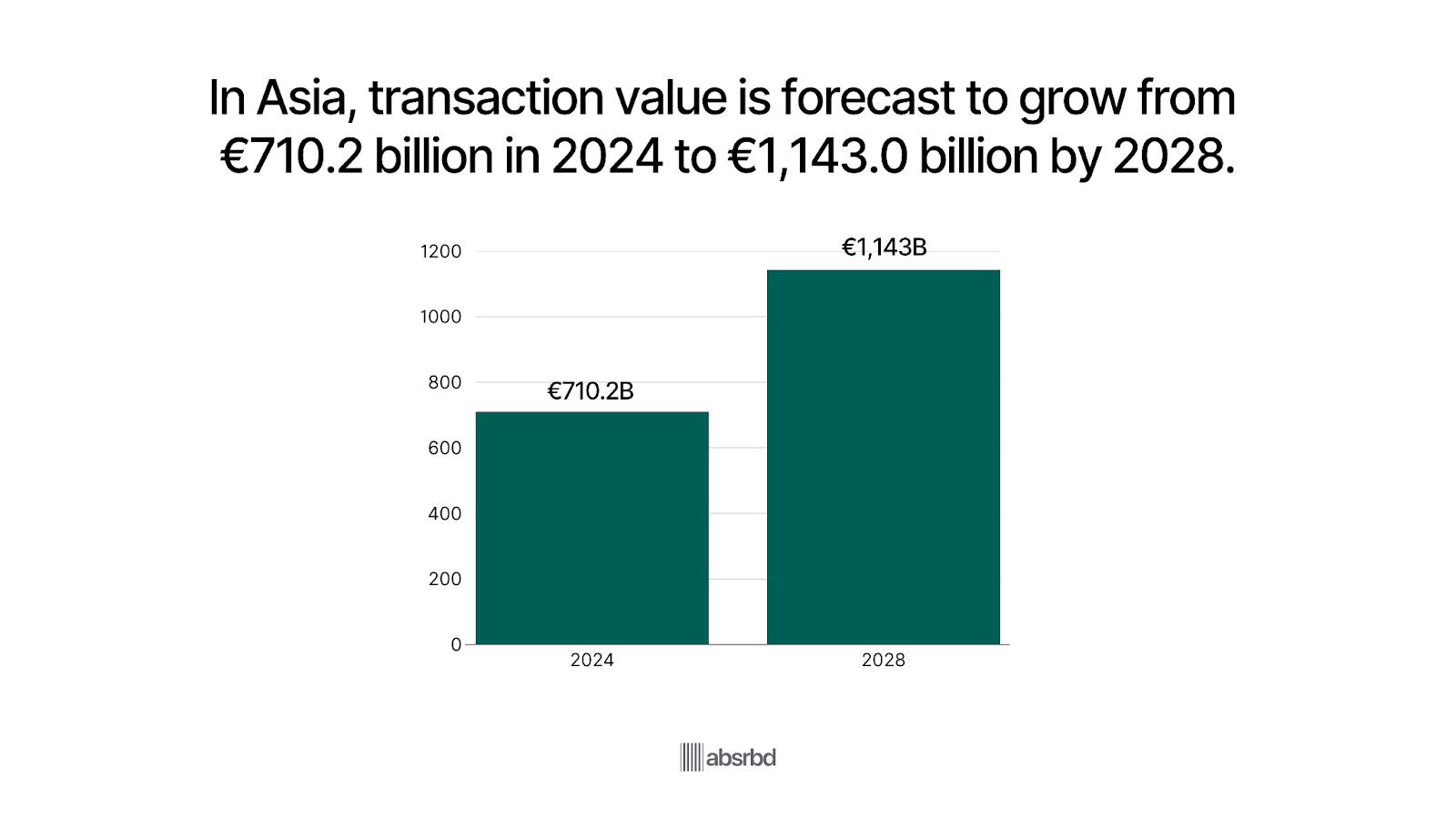

- The Asia region’s neobanking transaction value was approximately €710.20 billion in 2024, with expectations to reach €1,143.00 billion by 2028. Statista

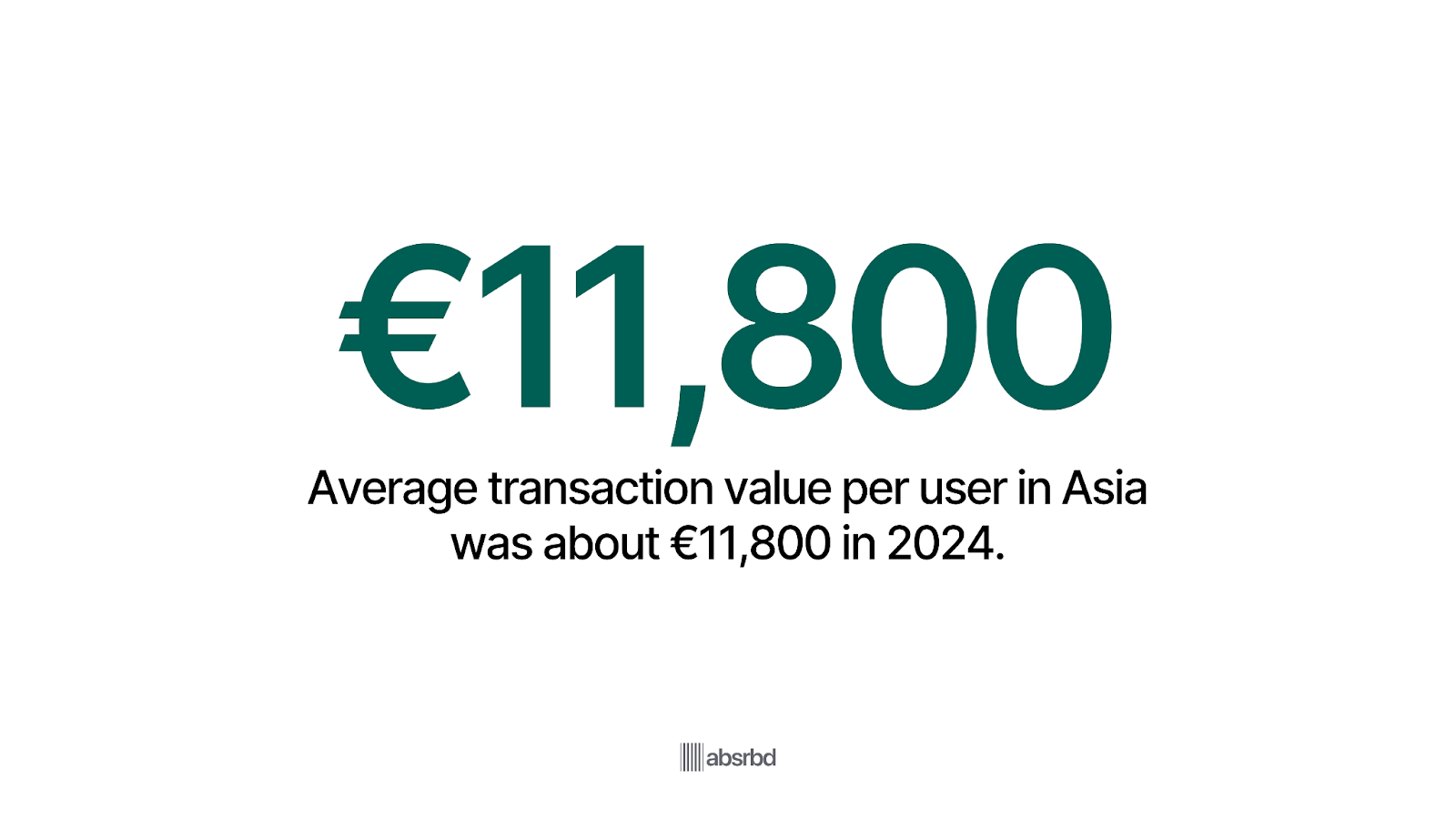

- In Asia, average transaction value per user was about €11,800 in 2024. Statista

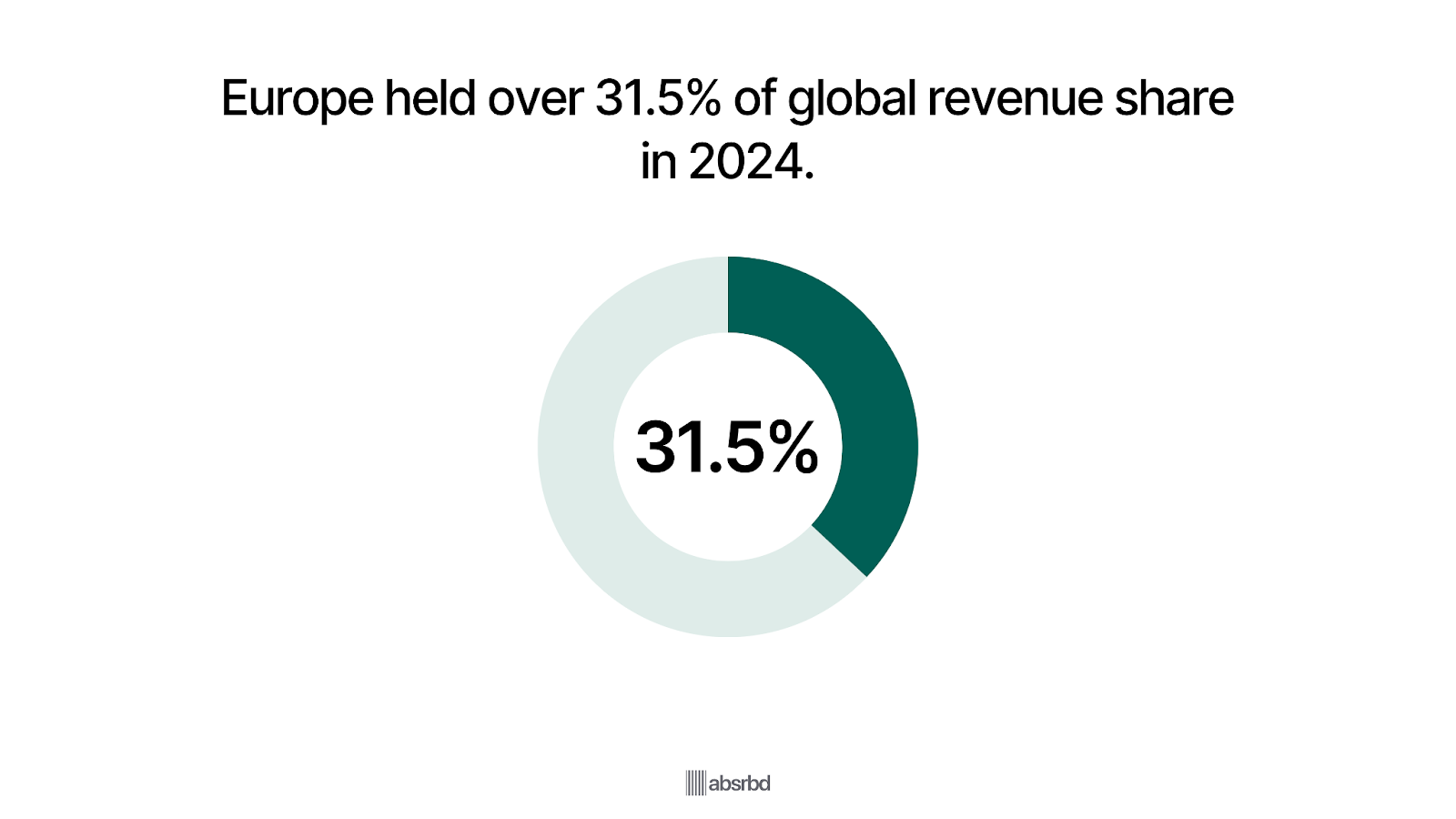

- Europe accounted for over 31.5% of global neobanking market share by revenue in 2024. IMARC Group

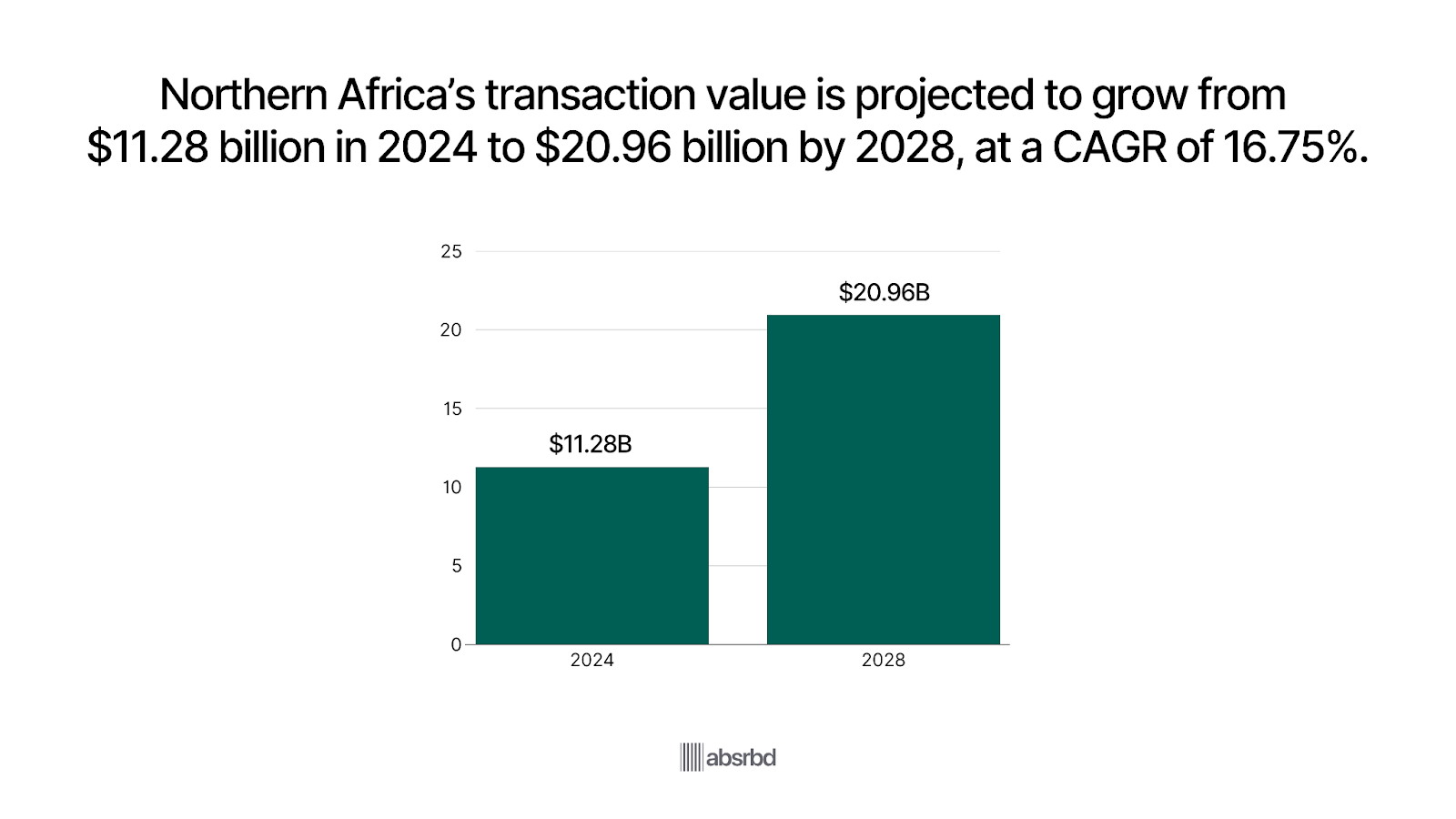

- Northern Africa’s neobanking transaction value is projected to be USD 11.28 billion in 2024, growing at a CAGR of 16.75% to USD 20.96 billion by 2028. Statista

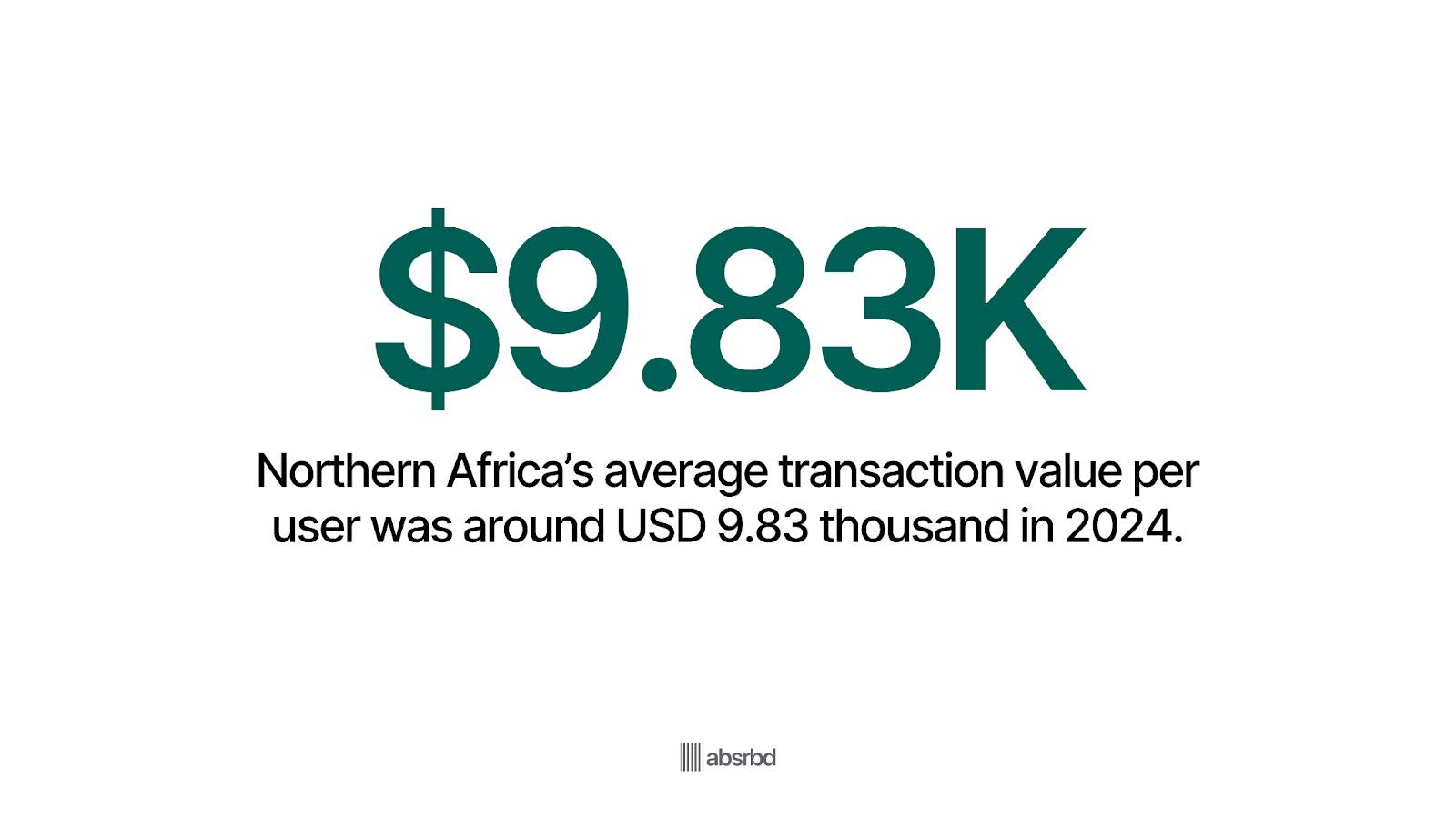

- Northern Africa’s average transaction value per user was about USD 9.83 thousand in 2024. StatistThe business account segment held about 67% of revenue share globally in 2024. Precedence Research

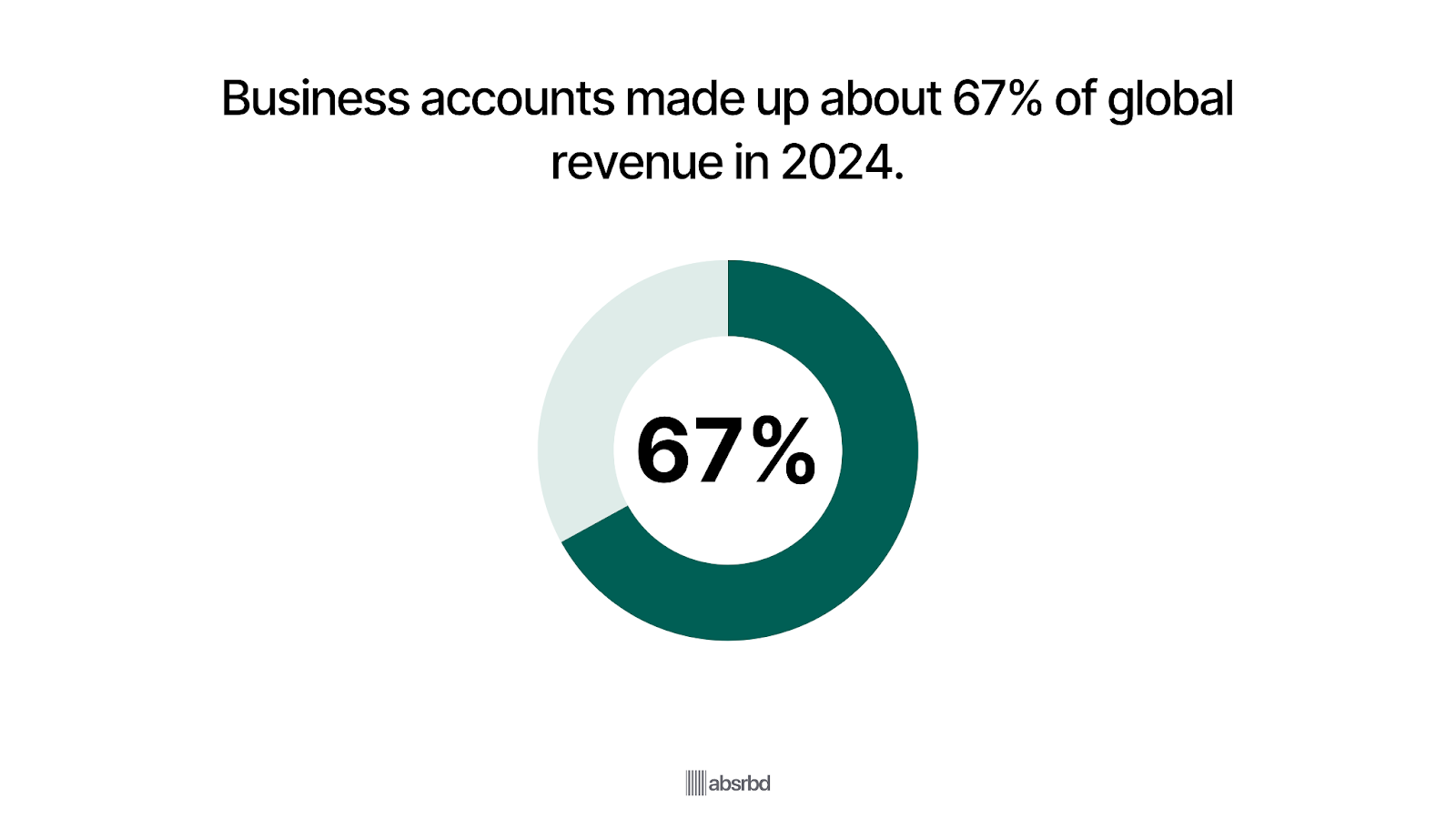

- The business account segment held about 67% of revenue share globally in 2024. Precedence Research

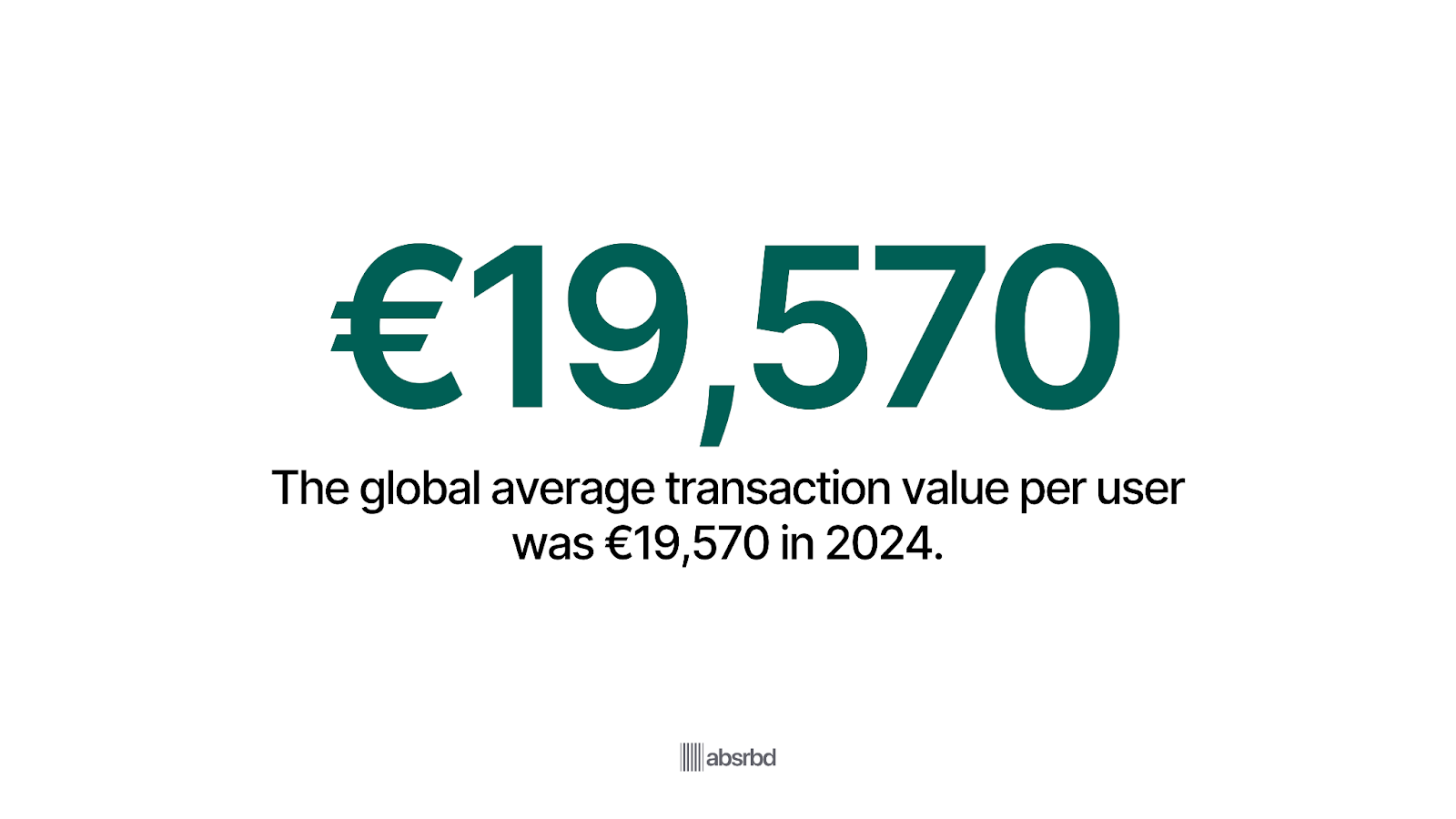

- In 2024, the average transaction value per user globally was €19,570. Statista

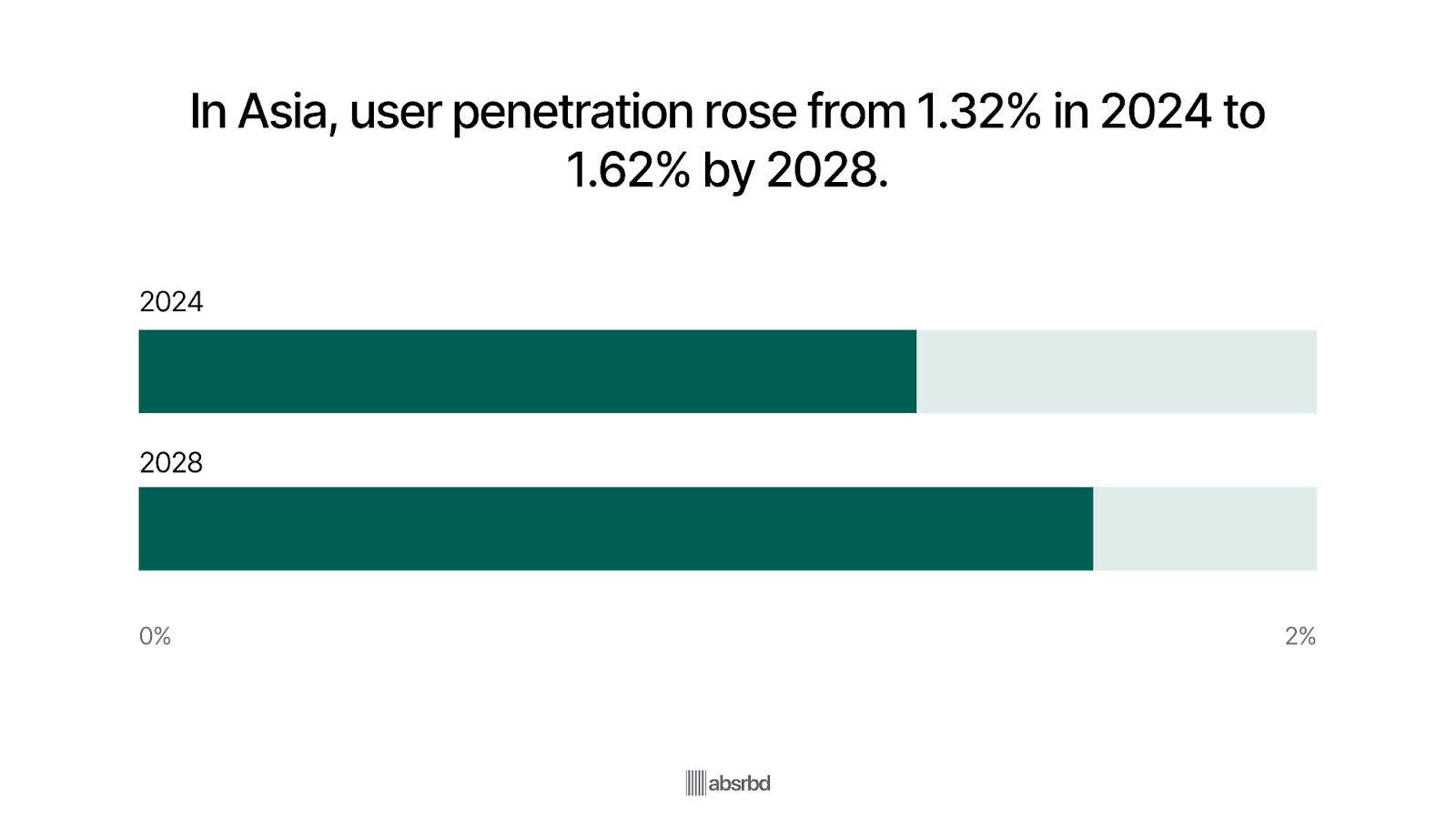

- In Asia, user penetration of neobanking was 1.32% in 2024, rising to 1.62% by 2028. Statista

- Global neobanking transaction value CAGR (2024-2028) is about 13.36%. Statista

Major Trends in Neobanking

Below are the key trends defining this next wave: AI personalization, embedded finance, niche focus, regulatory clarity, and much more.

Neobanking to Reach USD 552.0 Billion in 2026 with 45% CAGR

The global neobanking market is expected to grow from USD 382.8 billion in 2025 to about USD 552.0 billion in 2026, reflecting a robust 45% year-on-year increase. P&S Intelligence

This surge is driven by widespread smartphone adoption, rising demand from Gen Z & Millennials for mobile-first banking, and growing regulatory support for digital banking infrastructure.

Europe holds the largest regional revenue share in 2024, while Asia-Pacific is forecast to be the fastest growing region through 2030. P&S Intelligence

34% of Gen Zers say traditional banks don’t understand their needs (Emarketer)

Younger generations are in charge of adopting neo-banking services, with nearly half of Gen Z and Millennials using digital-only banks.

This trend is crucial as it indicates a shift in consumer preferences towards more technologically advanced and user-friendly financial services.

Furthermore, 80% of Gen Z and 81% of millennials report that digital banking is at the core of their banking preferences, and 53% of Gen Z and 51% of millennials identify it as a top need for choosing a new institution. (Apiture)

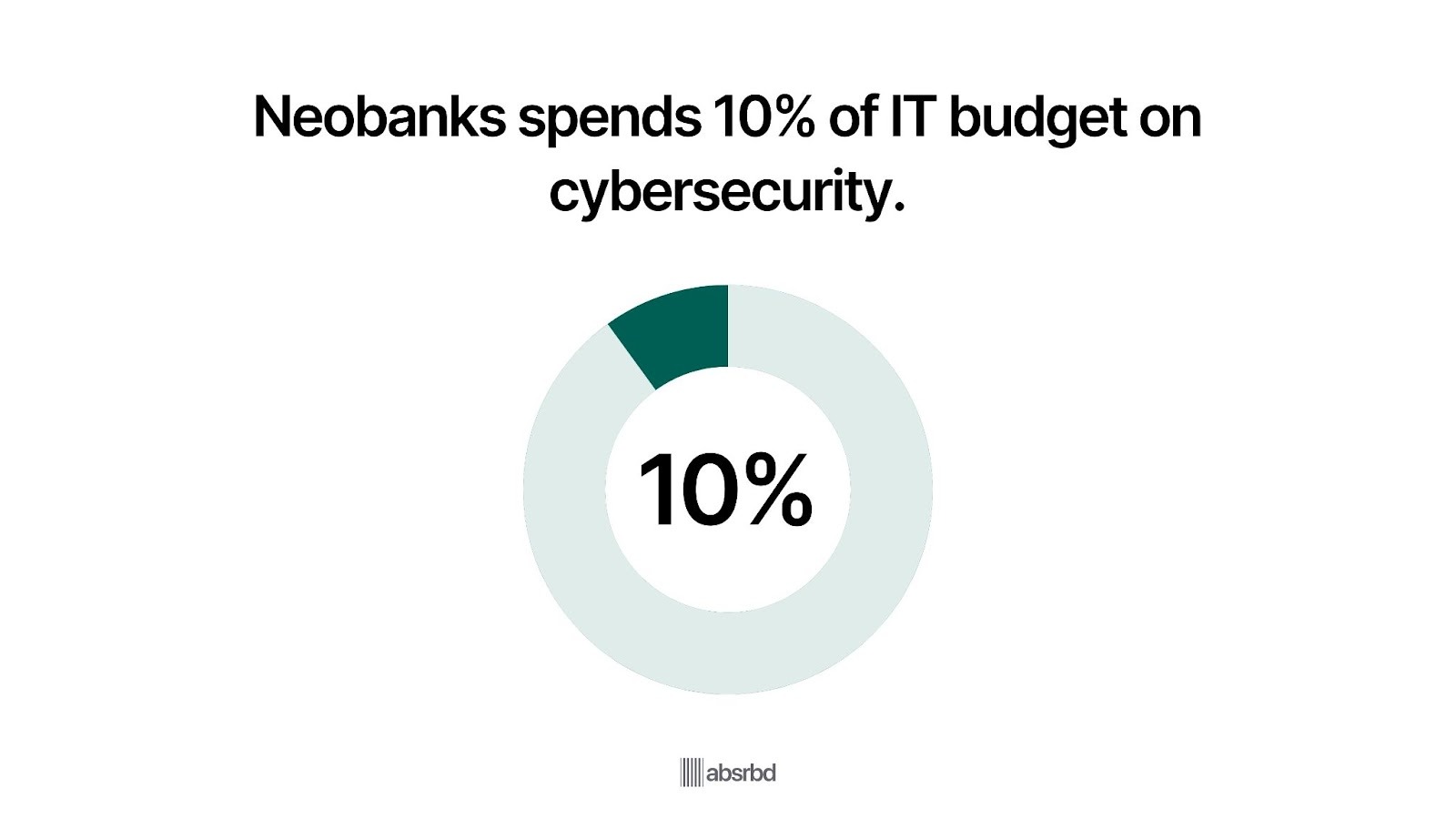

Cybersecurity Spending in Neobanks Projected to Reach 10% of IT Budgets (Fintechna)

Neobanks are significantly increasing their cybersecurity spending to protect against growing threats in the digital banking landscape.

This trend is crucial as it demonstrates the industry's commitment to safeguarding customer data and maintaining trust in digital-only banking platforms.

On average, large financial services companies, including neobanks, are allocating 10% of their IT budgets to cybersecurity.(Fintechna)

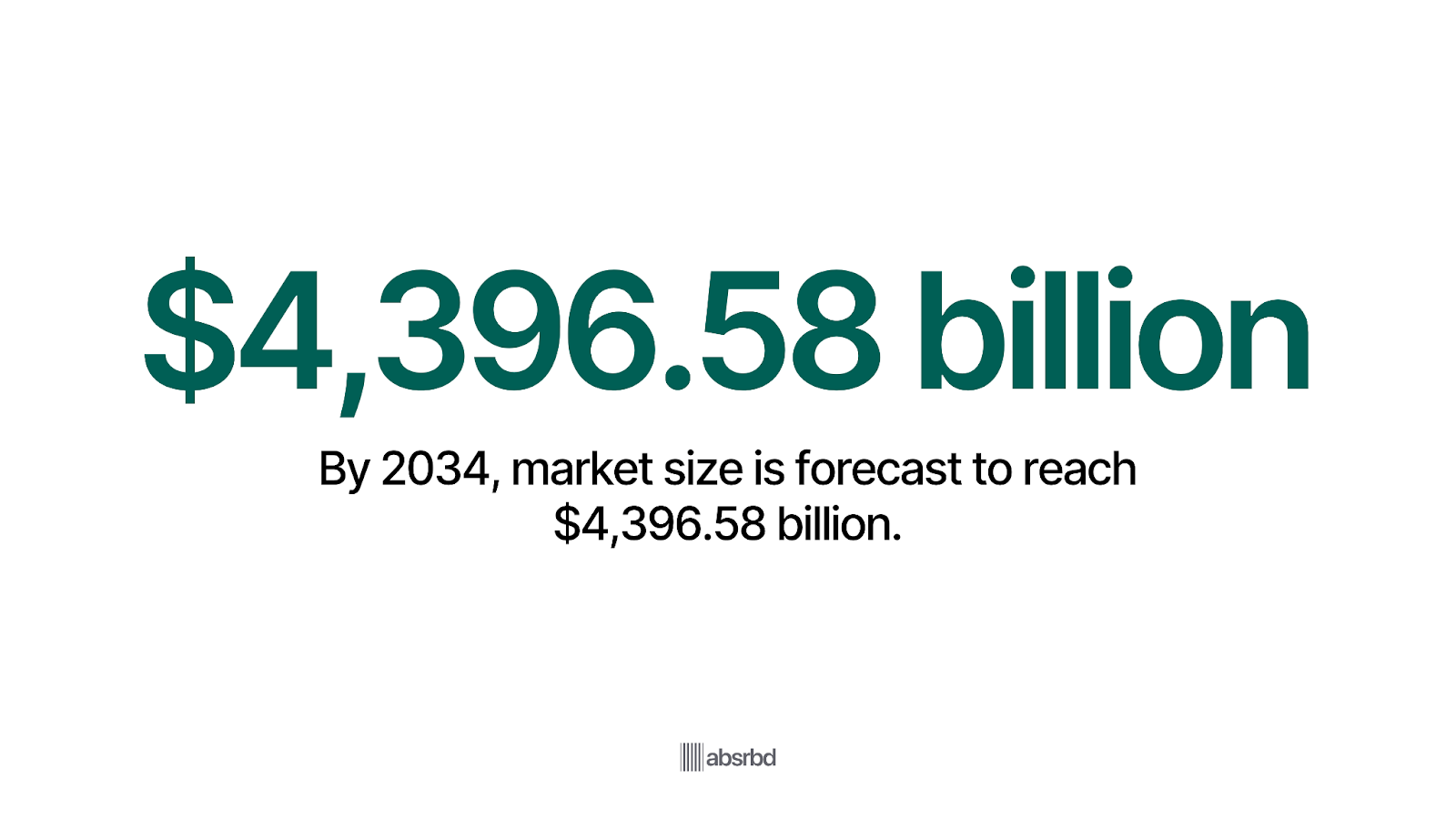

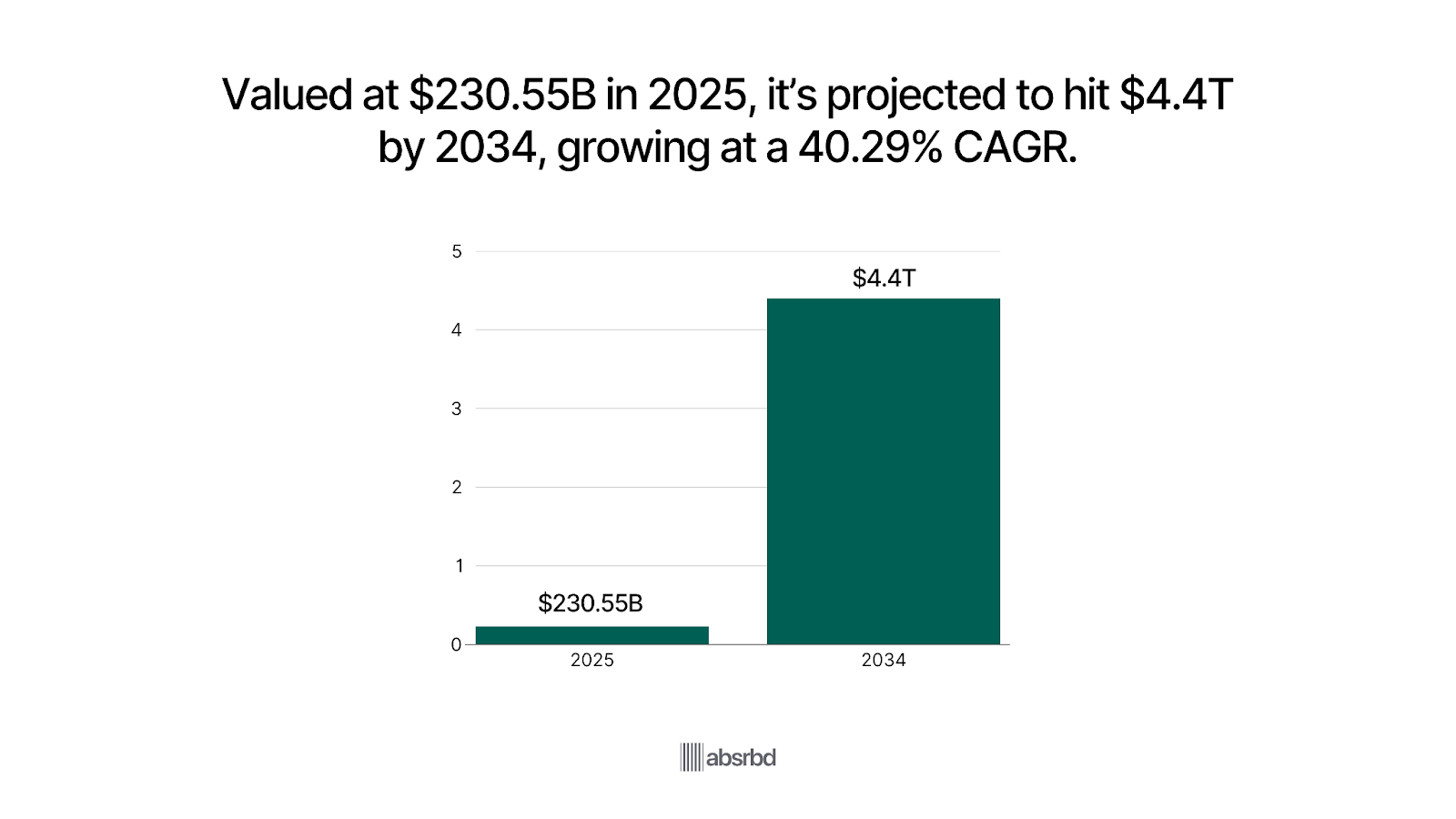

Neobanking Market Expected to Hit USD 4,396.6 Billion by 2034

Following an estimated USD 230.55 billion valuation in 2025, the global neobanking market is predicted to reach USD 4,396.58 billion by 2034, with a CAGR of 40.29% over 2025-2034. Precedence Research

This reflects huge growth in both user base and service complexity—neobanks increasingly offering savings, loans, business banking, investment, and cross-border services.

Europe was the dominant market in 2024 (34% share), while Asia-Pacific is expected to lead growth in coming years. Precedence Research

Rapid Growth in User Adoption; 43% of Brazilians Use Neobanks (SEON)

Brazil has seen a remarkable surge in neobank adoption, with 43% of its population now using digital-only banks.

This rapid adoption is largely attributed to the accelerated digitization during the COVID-19 pandemic, which pushed many to seek more convenient banking solutions.

This trend is significant because it highlights the growing preference for digital banking over traditional banking methods, especially in emerging markets.

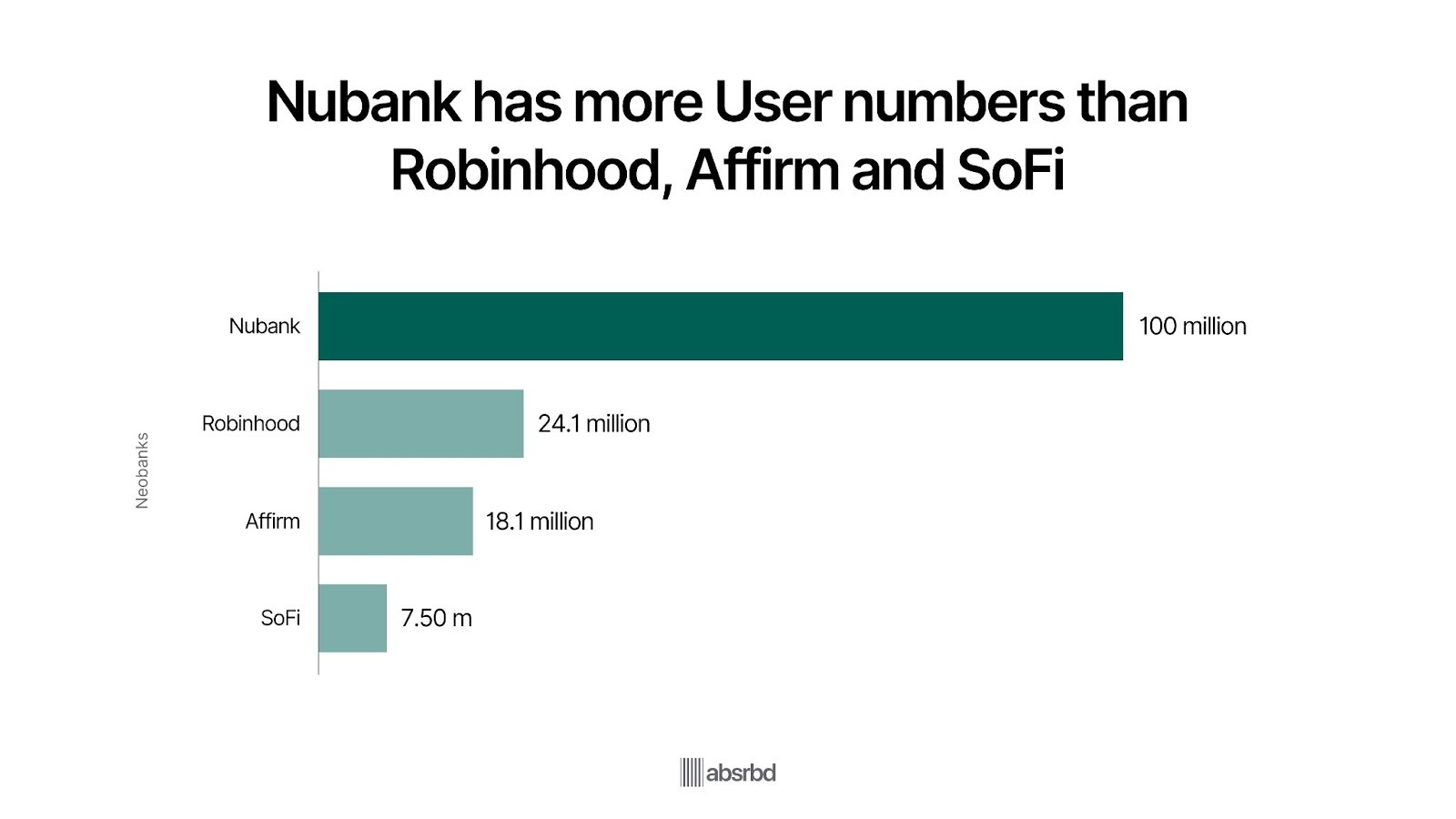

For instance, Nubank, one of Brazil's leading neobanks, has over 100 million users, demonstrating the high demand for digital financial services. (PYMNTS)

Founded on May 6, 2013, Nubank operates in just three Latin American countries yet boasts more customers than JP Morgan and Bank of America, the second-largest bank in the US.

This makes it larger than Robinhood, Affirm, and SoFi.

Nubank's rapid growth, driven 80% by word of mouth, showcases how neobanks can outpace traditional banking giants like Bank of America, Wells Fargo, and JPMorgan Chase in key metrics such as customer base and market impact. Nubank

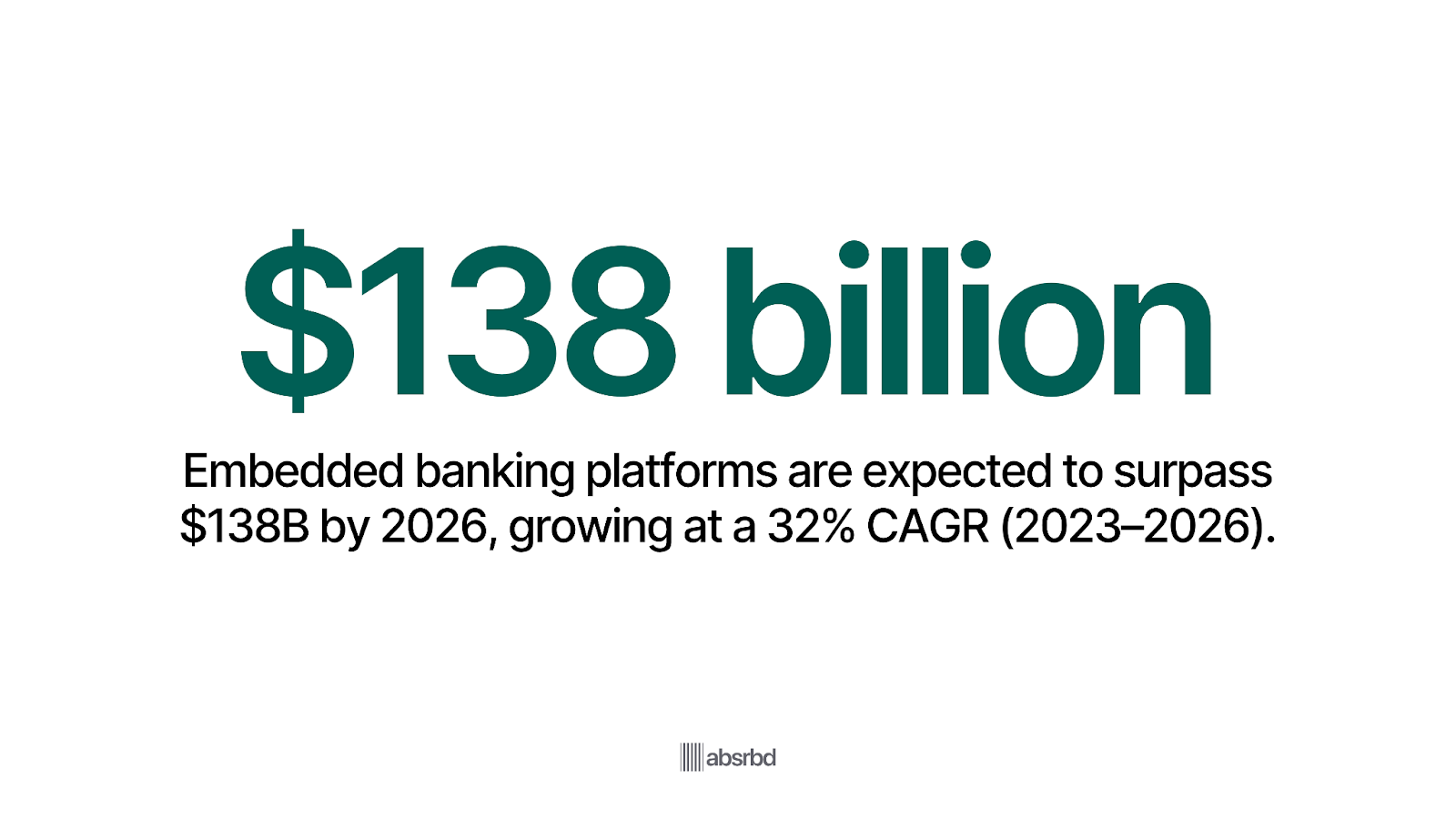

Revenue Set to Hit USD 138 Billion by 2026; 32% CAGR

Embedded banking platforms are forecast to exceed USD 138 billion by 2026, expanding at 32% CAGR (2023-2026) as more businesses embed financial services in non-bank platforms. Quick Market Pitch

Growth is driven by API commoditization, which lowers barriers for small and medium-sized businesses to launch financial products without building full banking infrastructure.

B2B use cases like invoice financing and embedded BNPL are major contributors to this growth, with strong demand from sectors with frequent cash-flow needs.

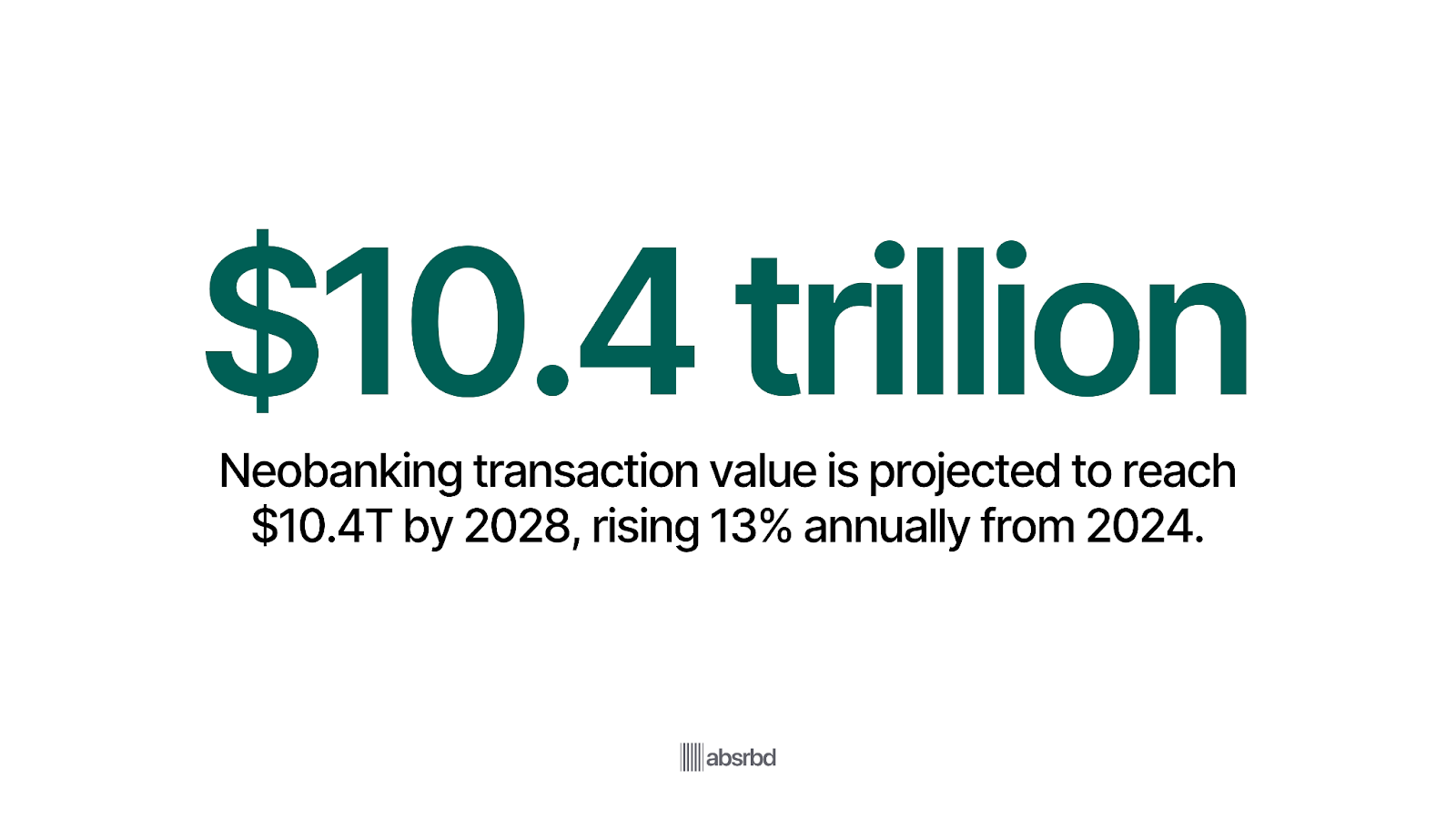

Global Transaction Volume to Top $10.4 Trillion by 2028; 13% CAGR

Neobanking’s global transaction value is projected to reach USD 10.4 trillion by 2028, growing 13% annually from 2024 levels. altindex.com

This trend demonstrates that as user numbers grow, transaction frequency and size are also scaling.

It underscores neobanks’ transition from novelty to core financial infrastructure.

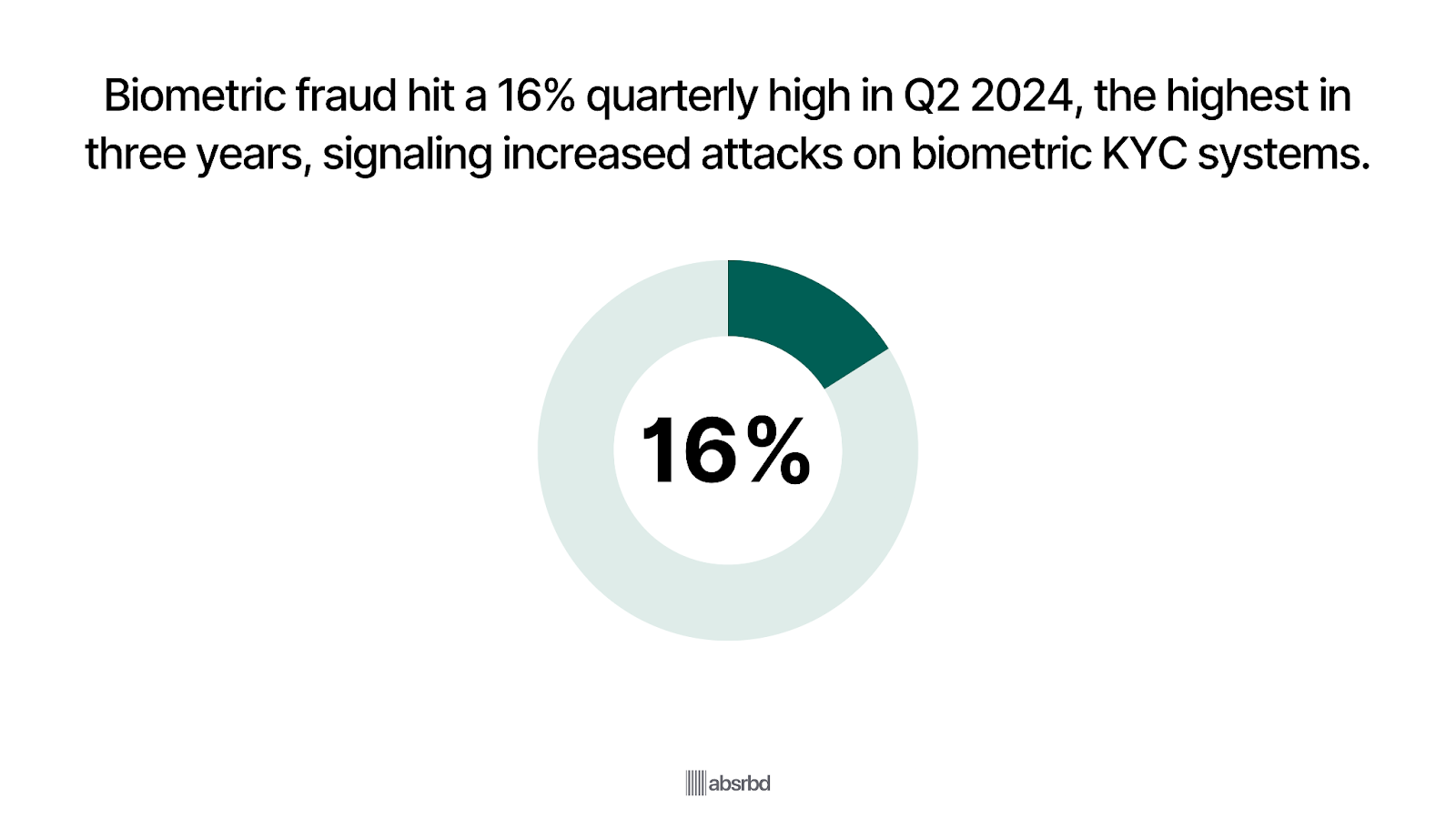

Biometric Fraud Peaked at 16% in 2024, Q2 High

Biometric fraud (e.g., spoofing, deepfake) reached a quarterly high of 16% in Q2 2024—the highest in three years, showing attackers are increasingly targeting biometric-based KYC systems. Smile ID

Document fraud also rose sharply, climbing from 4% in early quarters to 9% by Q4, indicating that fraud is no longer only targeting biometric systems. Smile ID

This trend underscores the urgent need for dynamic liveness detection, multi-factor identity verification, and advanced fraud prevention tools in neobank onboarding.

Neobanking Challenges

Neobanks scale fast but face structural limits, low ARPU, high CAC, regulatory friction, and increasing cyber threats that can stall momentum.

1. Few percent of neobanks are profitable: Multiple analyses show most neobanks remain unprofitable, while industry summaries into 2024–25 suggest a small improvement. This wide range reflects different sample sets and timing, but the message is consistent: low ARPU, high marketing spend and subsidized pricing keep margins thin. Investing.com

2. Customer acquisition costs (CAC) are a major drag on unit economics: Neobanks typically face meaningful marketing and incentive costs to sign new users; reported CACs vary but are frequently cited in the single- to double-digit dollars range per acquisition and are a key metric for profitability. Because many digital banks subsidize onboarding (bonuses, fee waivers), reliance on low-cost organic acquisition or high LTV/CAC ratios is critical to reach break-even.

3. Low revenue per user (ARPU) constrains margins; many neobanks earn under $30/year per customer: Public and industry analyses show that several neobanks generate modest annual revenue per customer from fees, interchange and subscriptions, making scale, and higher-margin products, essential to improve unit economics. Until neobanks cross-sell lending, business services, or premium subscriptions at scale, ARPU pressures continue to limit profitability.

4. Regulatory & compliance complexity imposes heavy costs and operational risk: Neobanks must comply with multi-jurisdictional KYC/AML, data-privacy, and licensing rules; failures or gaps can trigger fines, remediation costs, and supervisory action. High-profile regulatory enforcement (and large fines) against digital banks in recent years shows how quickly compliance lapses can damage finances and reputation.

5. Cybersecurity, identity fraud and synthetic identity attacks are rising threats: Fraud trends show biometric and document-based attacks are growing: biometric fraud peaked at 16% in Q2 2024 and remained materially elevated through 2024, underlining attackers’ focus on onboarding channels. Neobanks must invest in layered identity, liveness detection and real-time monitoring to keep fraud losses manageable. cms.med

6. Operational dependence on third-party providers creates systemic risks: Many challengers outsource core rails (BaaS providers, card processors, cloud vendors, KYC vendors). When partners suffer outages, security incidents, or regulatory problems, the neobank’s service, and brand trust, can be instantly impacted. This vendor concentration forces heavy vendor governance, contractual protections, and contingency planning.

7. Scaling customer support and operations without exploding costs is difficult: Rapid user growth increases demand for 24/7 support, dispute handling, fraud investigations, and credit operations; building those teams is expensive and often lags product growth. Poorly scaled operations produce outages and slow response times, which quickly erodes trust in a digital-only relationship.

8. Product and regulatory uncertainty for new offerings (crypto, cross-border, DeFi) slows monetization: Innovations such as crypto custody, cross-border settlement or DeFi integrations offer upside, but inconsistent regulation and unclear licensing mean slower rollout and higher compliance costs. Neobanks must balance first-mover advantage with legal risk and increased regulatory scrutiny.

Neobanking Opportunities

Key opportunities include AI-driven hyper-personalization, SME banking solutions, expanding into emerging markets, embedded finance models, digital ID verification, and B2B banking-as-a-service offerings.

AI and Machine Learning for Personalization

Neobanks leverage AI and ML algorithms to offer hyper-personalized services based on deep data insights.

This includes personalized budgeting, automatic savings roundups, fraud detection with over 90% accuracy, and real-time customer service through natural language processing (NLP). SuperAGI

These technologies significantly enhance customer engagement, reduce costs through automation, and differentiate neobanks in competitive markets.

Partnerships with Traditional Banks

An increasing trend is collaboration between neobanks and traditional banks.

Neobanks benefit from the incumbents' regulatory compliance, trust, and capital, while traditional banks gain agility and digital innovation.

This results in models like white-label digital banking and banking-as-a-service (BaaS), enabling faster product launches and expanded customer bases.

Shared Banking and Personal Finance Management

Neobanks are focusing on shared banking features such as shared accounts, peer-to-peer payments, expense splitting, and integrated personal finance management (PFM) tools.

These allow users to manage finances collaboratively and holistically, especially appealing to millennials and Gen Z who prefer transparent, social money management.

Cryptocurrency and Blockchain Integration

Digital banks are adopting cryptocurrency services, allowing customers to buy, sell, and store digital assets inside banking apps.

This includes crypto staking, lending, decentralized finance (DeFi) protocols, yield farming, and blockchain-powered cross-border payments.

Such integrations open new revenue streams and address the growing interest in digital assets.

Open Banking and API Ecosystems

Open banking APIs enable neobanks to integrate with third-party financial services such as investment platforms, insurance, accounting software, and payment solutions.

This integration creates seamless money management experiences for customers, enabling account aggregation, payment initiation, and robo-advisory services.

Instant Loans and Credit

Neobanks cater to the rising demand for instant microloans and short-term credit through algorithms that assess creditworthiness in real-time.

Customers enjoy quick approvals and fund disbursement without traditional paperwork, enhancing financial inclusion and convenience.

Hyper-Niche and SME Banking

Neobanks are targeting specific market segments like gig workers, youth, immigrants, and small businesses with tailored products and onboarding.

SME banking services include easy account setup, digital invoicing, payment acceptance, and automated accounting integration.

This segment is underserved by traditional banks and offers steady deposits and fee income for neobanks.

Embedded Finance

Neobanks integrate their services into non-financial platforms, allowing users to access payments, lending, subscriptions, insurance, investments, bill payments, and digital identity verification within everyday apps.

Examples include paying for rides via a neobank or instant microloans at checkout, driving growth through contextual banking.

Cross-Border Banking and Multi-Currency Wallets

Globalization and remote work boost demand for multi-currency wallets, real-time foreign exchange, and global bill payment tools.

Neobanks providing seamless, low-fee international transactions enable financial inclusion for diaspora, freelancers, and SMEs with international operations.

Social and Environmental Responsibility

Neobanks are incorporating social impact initiatives—like eco-friendly cards that track carbon footprints, charity donations via app rounding, and partnerships with environmental causes—to attract socially conscious consumers and enhance brand loyalty.

Potential Neobanking Disruptors

Potential disruptors in the neobanking market over the next several years include a number of key technological, business model, and market innovation trends that could radically reshape neobanking:

Decentralized Finance (DeFi)

DeFi could significantly disrupt neo-banking by offering decentralized financial services that operate on blockchain technology.

DeFi platforms provide lending, borrowing, and trading services without intermediaries like traditional banks or neobanks.

This technology can offer more transparent, efficient, and accessible financial services globally.

As DeFi platforms mature, they could attract users away from neobanks by offering higher yields and more innovative financial products.

Central Bank Digital Currencies (CBDCs)

CBDCs are digital versions of national currencies issued by central banks.

The introduction and widespread adoption of CBDCs could change the digital banking landscape.

If central banks start issuing digital currencies directly to consumers, this could reduce the reliance on neobanks and traditional banks for certain types of transactions.

Countries like China are already piloting their digital yuan, and other nations are exploring similar initiatives.

Big Tech Entry into Banking

Major technology companies like Google, Apple, and Amazon are interested in entering the financial services sector.

These companies have extensive user bases, advanced technological infrastructure, and significant financial resources.

If these tech giants decide to fully enter the neo-banking space, they could leverage their ecosystems to offer integrated financial services, potentially disrupting existing neobanks.

For instance, Apple Pay and Google Pay are widely used for transactions, and expanding into full banking services would be a natural progression.

Enhanced Artificial Intelligence (AI)

Advanced AI applications in banking could be a major game-changer.

AI can improve customer service through better chatbots, provide personalized financial advice, enhance fraud detection, and streamline various banking operations.

Neobanks that integrate advanced AI capabilities will have a significant competitive advantage.

For example, AI-driven neobanks could offer more accurate credit scoring, personalized financial products, and predictive financial planning tools.

Regulatory Changes

Significant changes in financial regulations could either hinder or help neobanks.

Stricter regulations could pose challenges in terms of compliance costs and operational hurdles.

However, regulatory support for innovation and competition in the financial sector could provide new opportunities for neobanks.

For example, the European Union's PSD2 regulation, which mandates open banking, has already facilitated more competition and innovation in digital banking.

Biometric Security

Implementing advanced biometric security measures, such as facial recognition and fingerprint scanning, could revolutionize how users interact with their banks.

Enhanced security features can significantly reduce fraud and identity theft, increasing user trust and adoption.

Neobanks that adopt these technologies can offer more secure and seamless banking experiences.

Integration with the Internet of Things (IoT)

Integrating neobanking services with IoT devices can offer more convenience and innovative solutions.

For instance, smart home devices could facilitate automated bill payments, and wearable devices could enable seamless transactions.

The growth of the IoT ecosystem will open new avenues for neobanks to provide services that integrate deeply into consumers' daily lives.

Impact of Neobanking Market Behaviour on Stakeholders

The behavior of the neobanking market from 2026 onward impacts multiple stakeholders, including customers, traditional banks, fintech companies, regulators, and investors, in various ways:

Impact on Customers

- Customers experience enhanced convenience due to mobile-first, digital-only banking solutions that offer instant account setup, payments, loans, and personalized financial management powered by AI.

- The rise of neobanks drives increased financial inclusion, especially among underserved populations, gig workers, SMEs, and digitally native younger generations, democratizing access to affordable, transparent banking.

- User-centric features like instant credit scoring, lower or zero fees, and 24/7 virtual support improve customer satisfaction and engagement.

Impact on Traditional Banks

- Traditional banks face stronger competition, pushing them to accelerate their digital transformation and partner with neobanks or fintech platforms to retain customers and innovate.

- Many incumbents adopt Banking-as-a-Service (BaaS) and white-label models, leveraging neobank infrastructure to offer digital products without legacy overhead.

- Neobanking disrupts revenue streams for traditional banks by cutting fees and automating services, pressuring incumbents to redesign cost structures and business models.

Impact on Fintech Companies and Ecosystems

- Fintech firms benefit by partnering with neobanks for open banking API integrations, embedded finance opportunities, and joint product innovation.

- Neobank growth fosters fintech ecosystem scaling, increasing collaborations in payments, lending, crypto, and data analytics.

- The market’s rapid expansion drives investments and technological advancement within related industries.

Impact on Regulators and Policy Makers

- Regulators must balance fostering innovation with ensuring security, privacy, and financial stability amidst the rise of digital-only banks.

- Open banking regulations, data protection laws, and digital operational resilience frameworks continue to evolve to accommodate neobanking.

- Regulatory clarity and support help build trust for neobanks and protect consumer interests.

Impact on Investors and Market Players

- The neobanking sector attracts significant venture capital, private equity, and strategic investments driven by rapid user growth and technology adoption.

- Investors benefit from emerging revenue models like subscription fees, premium services, and BaaS platforms.

- Market players must focus on innovation, customer experience, and sustainable growth to maintain competitiveness.

Conclusion

The data shows that neobanking continues its rapid ascent in 2026, with the global market surpassing USD 550 billion and user numbers approaching 400 million worldwide.

Transaction values are set to climb toward €10 trillion by 2028, confirming that digital-only banks are becoming a mainstream financial channel.

Looking ahead, forecasts suggest the market could exceed USD 1.2 trillion by 2029, with strong growth across Asia, Latin America, and Africa.

While challenges around profitability, compliance, and cyber risk remain, the long-term outlook points to sustained expansion and deeper integration of neobanks into global financial systems.

Key takeaway: Neobanking is no longer a challenger, it is on track to become a core pillar of the global banking industry.